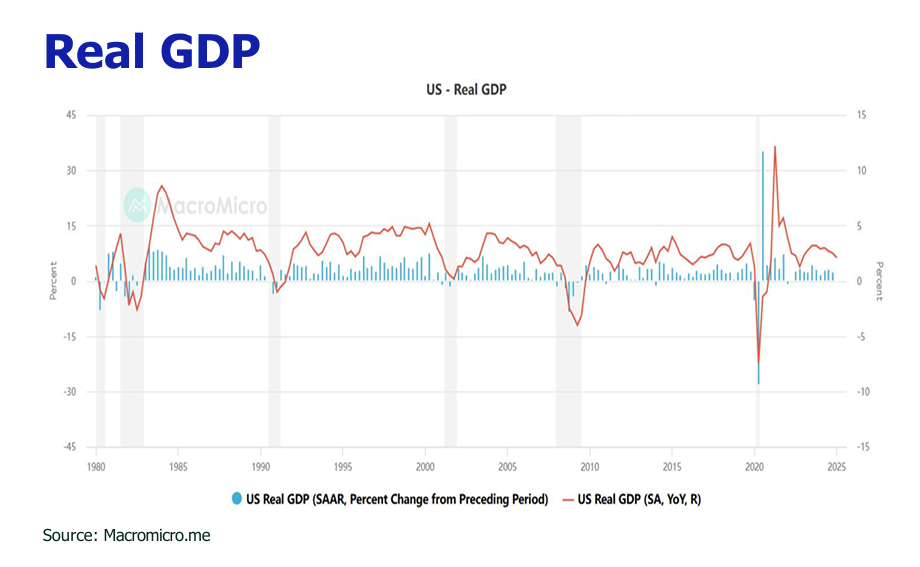

Highlights

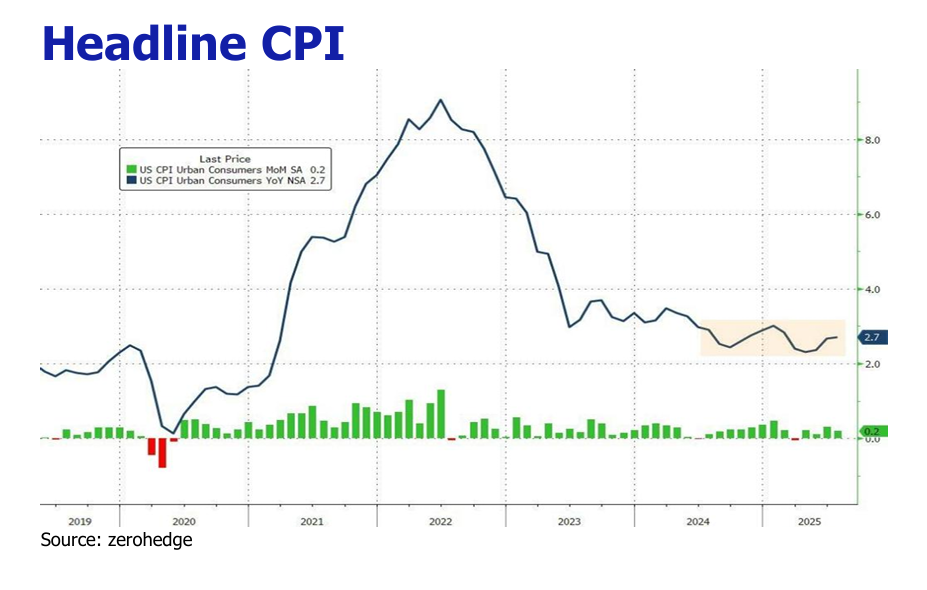

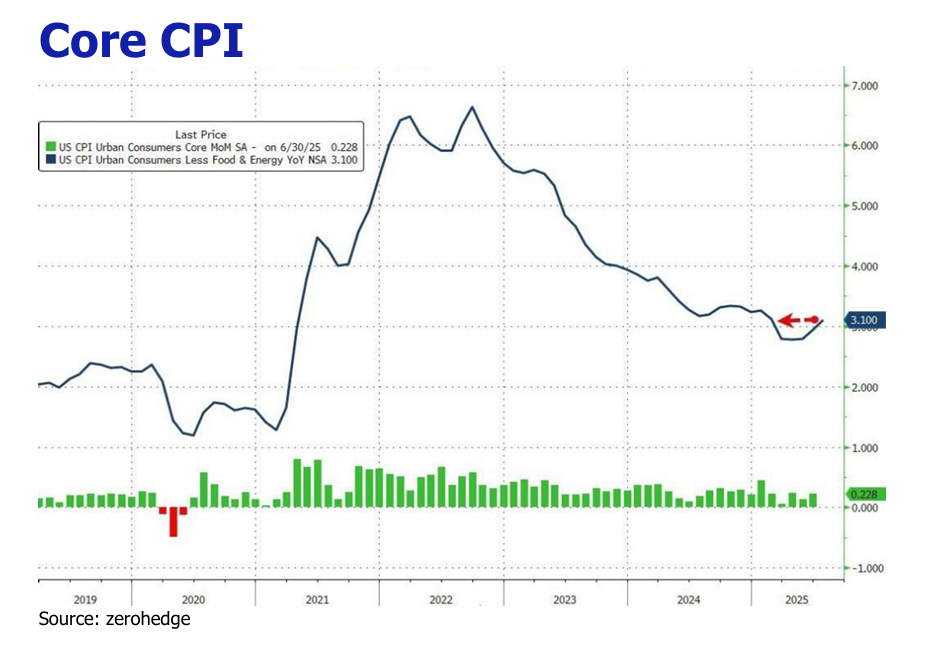

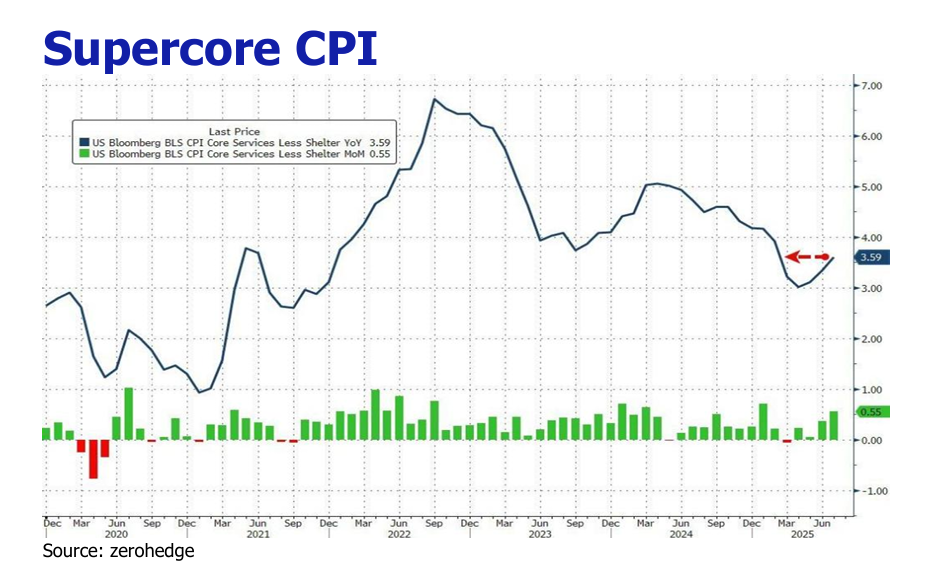

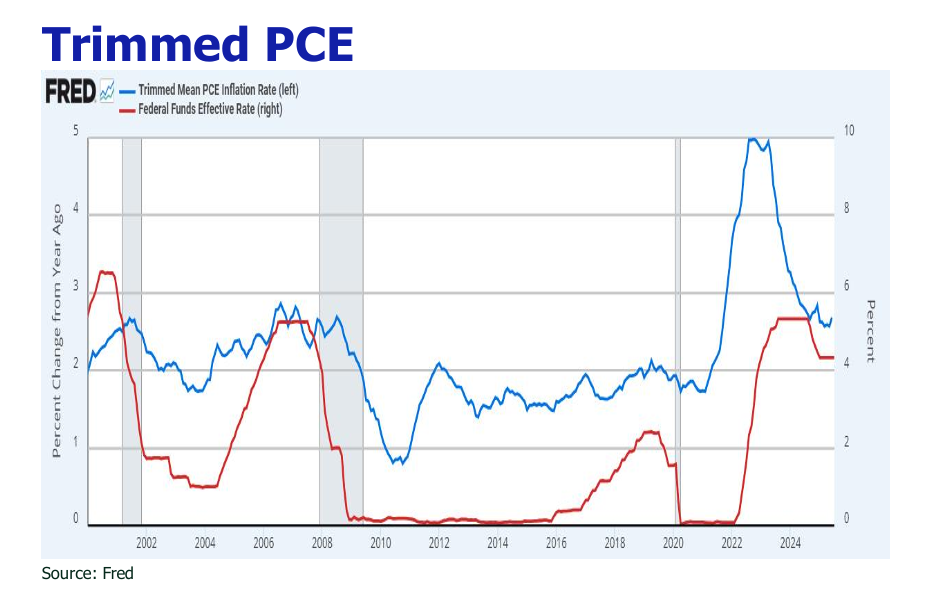

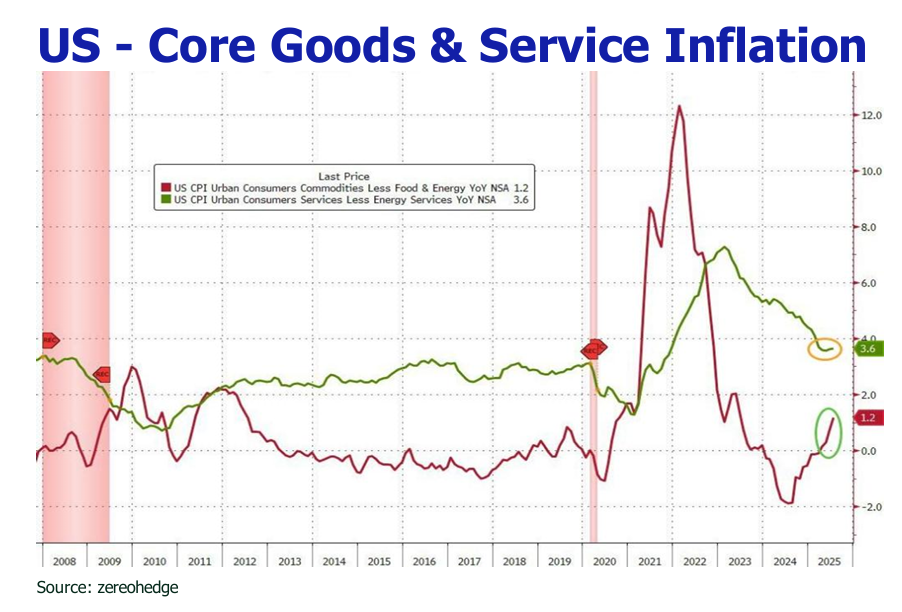

![]() July 2025’s inflation canvas splashed a cooling headline CPI (+0.2% MoM and +2.7% YoY), yet core (+0.3% MoM, +3.1% YoY) and supercore (+0.5% MoM, +3.7% YoY) measures simmered with persistent heat from shelter and tariff-spiked goods.

July 2025’s inflation canvas splashed a cooling headline CPI (+0.2% MoM and +2.7% YoY), yet core (+0.3% MoM, +3.1% YoY) and supercore (+0.5% MoM, +3.7% YoY) measures simmered with persistent heat from shelter and tariff-spiked goods.

![]() July’s retail scene sparkled with a +0.5% MoM rise, buoyed by strong auto sales linked to expiring credits and robust discount-driven online shopping.

July’s retail scene sparkled with a +0.5% MoM rise, buoyed by strong auto sales linked to expiring credits and robust discount-driven online shopping.

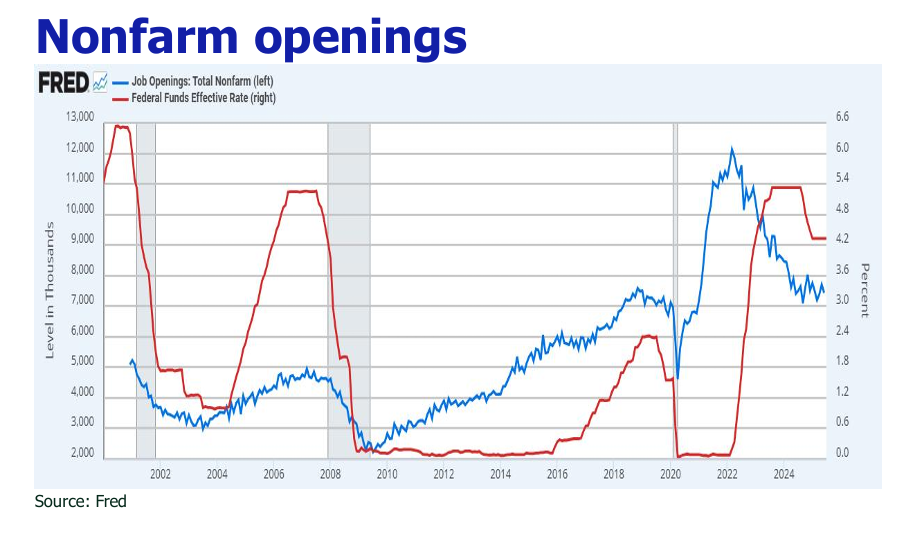

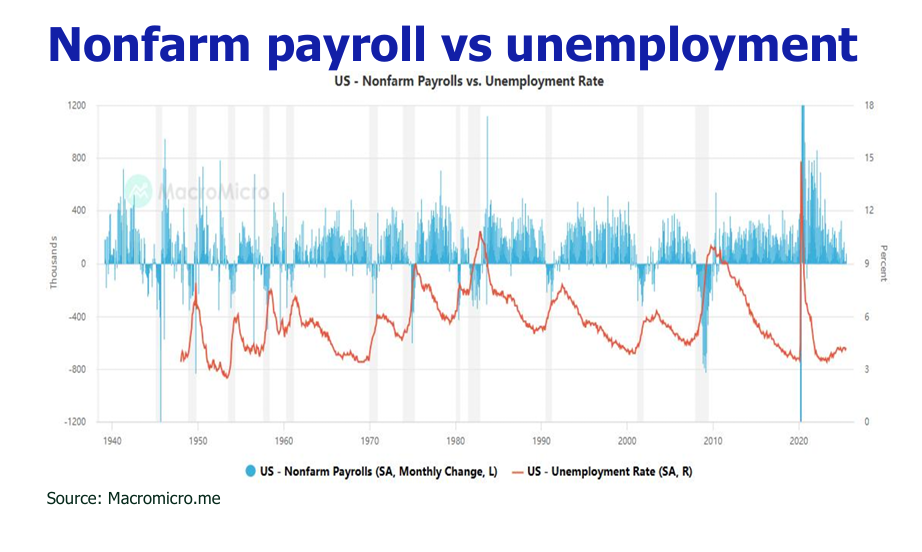

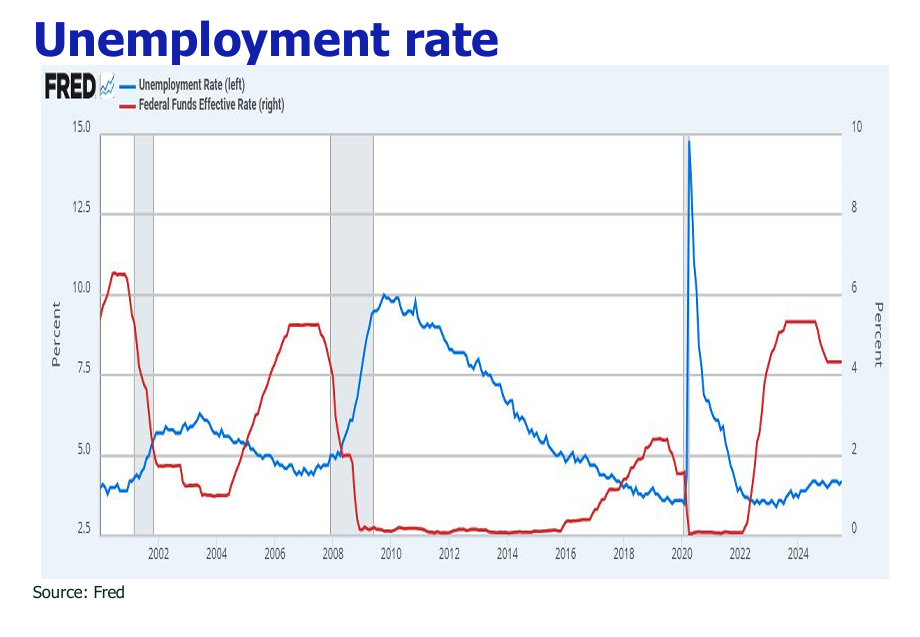

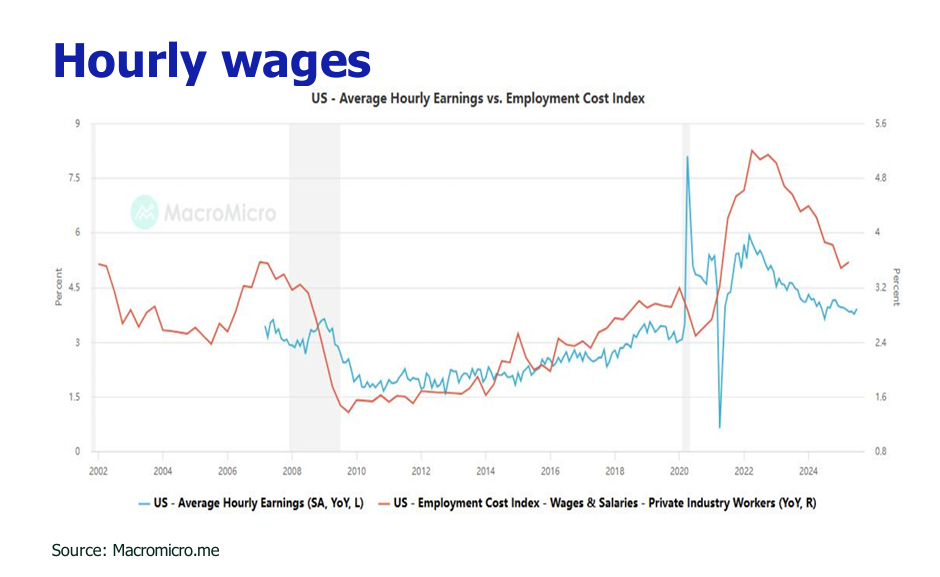

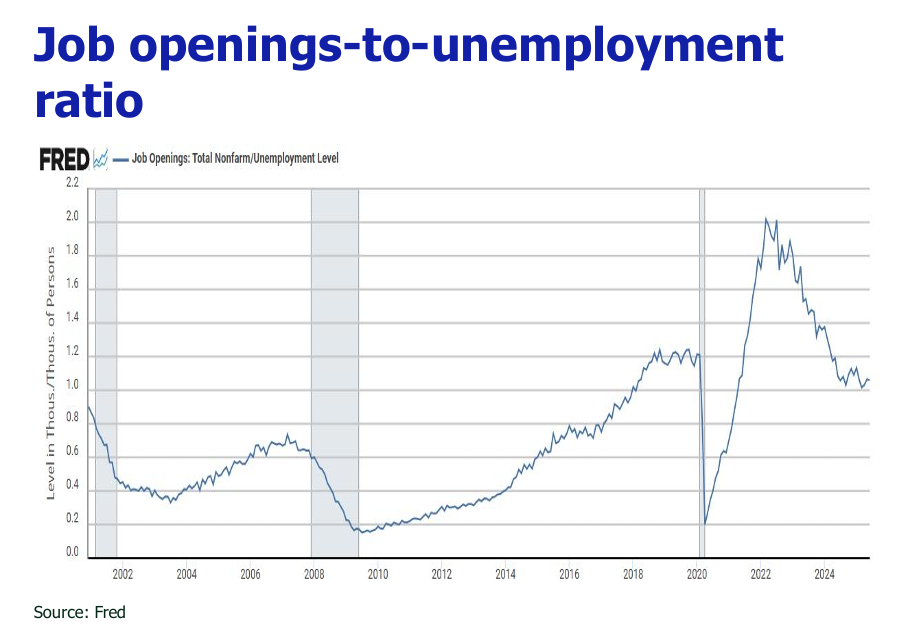

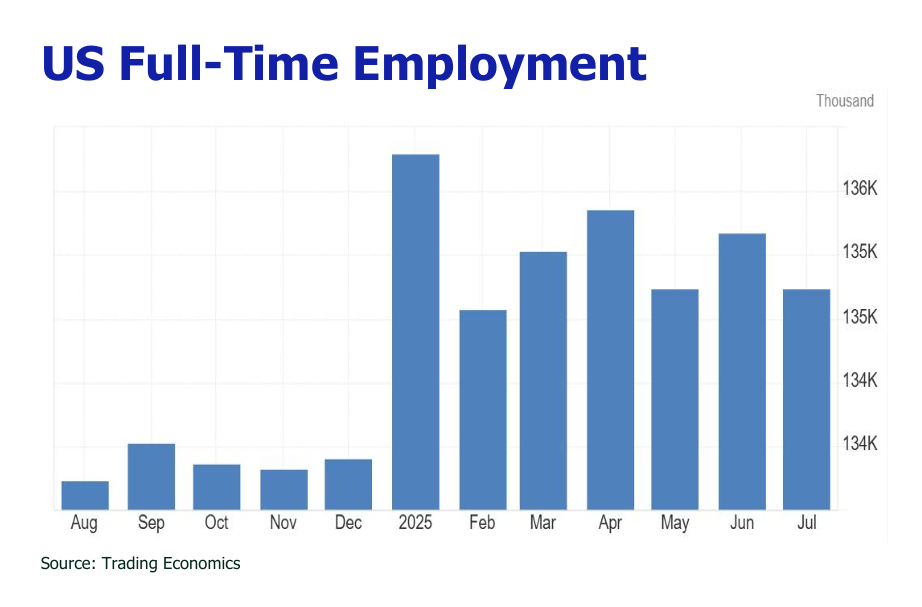

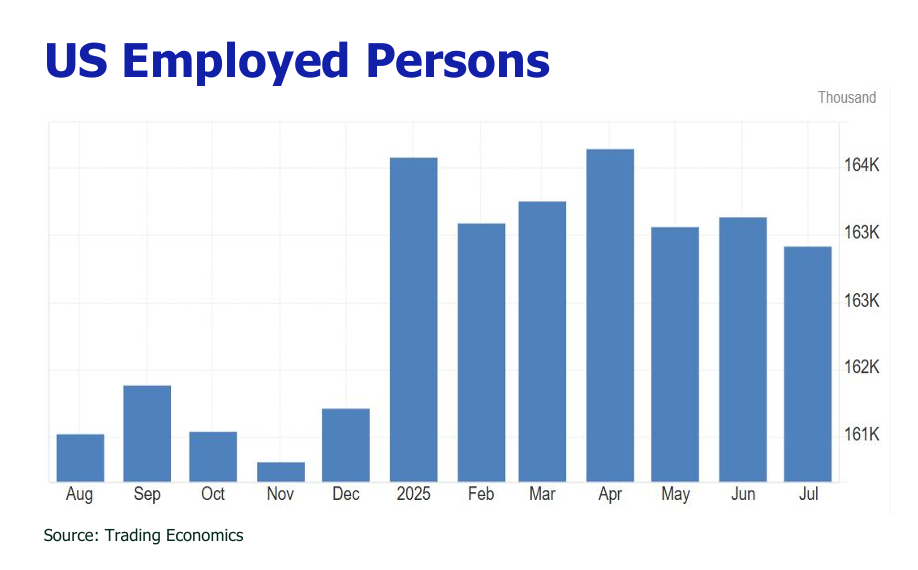

![]() Abroad-based slowdown in the U.S. labor market was evident in July as job creation caught off guard with only 73,000 positions added, preceded by near-stallion in previous months, and the unemployment rate climbed to 4.2%.

Abroad-based slowdown in the U.S. labor market was evident in July as job creation caught off guard with only 73,000 positions added, preceded by near-stallion in previous months, and the unemployment rate climbed to 4.2%.

![]() Inflation’s slow burn is poised to flare as foreign producers and depleted inventories lead to more tariff costs being passed to consumers, though a faltering labor market and restrained spending may keep the blaze in check.

Inflation’s slow burn is poised to flare as foreign producers and depleted inventories lead to more tariff costs being passed to consumers, though a faltering labor market and restrained spending may keep the blaze in check.

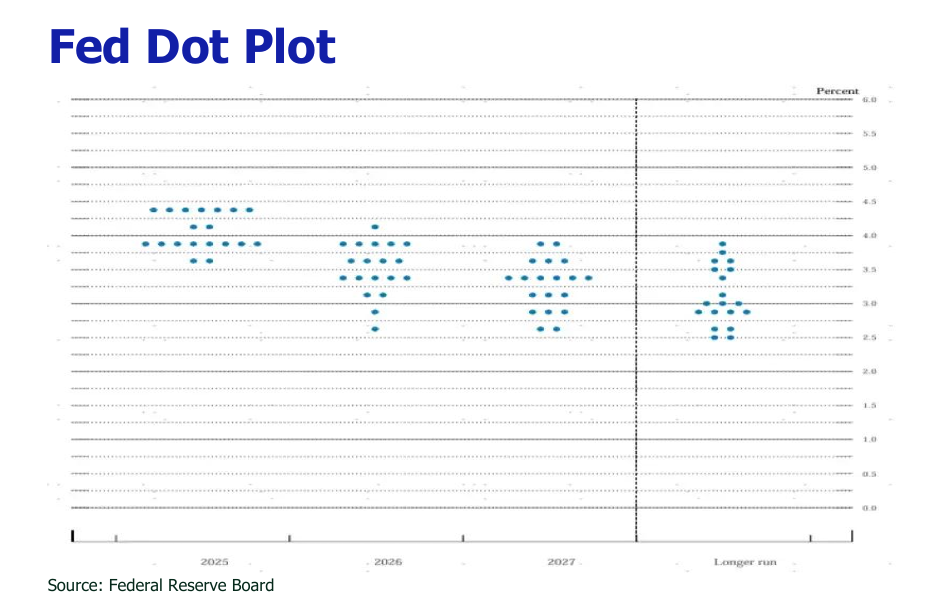

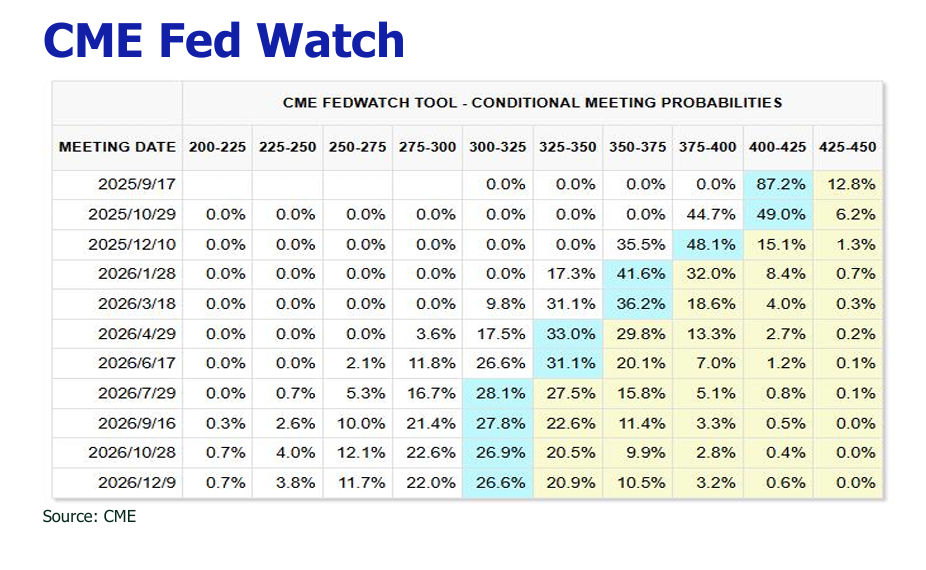

![]() Dimming job market prospect, deferred tariff pressures, a measured ascendance of inflation and Powell’s remark of restrictive policy shift in Jackson Hole have woven an 87% market bet for a sleek 25 basis point Fed rate cut in September.

Dimming job market prospect, deferred tariff pressures, a measured ascendance of inflation and Powell’s remark of restrictive policy shift in Jackson Hole have woven an 87% market bet for a sleek 25 basis point Fed rate cut in September.

![]() In August, the Hang Seng Index sustained a vibrant tune, closing above 25,000 with over 2% monthly surge, fueled by a tech stock frenzy and U.S.-China tariff truce optimism, with daily trading volumes pulsating between HK$200-320 billion.

In August, the Hang Seng Index sustained a vibrant tune, closing above 25,000 with over 2% monthly surge, fueled by a tech stock frenzy and U.S.-China tariff truce optimism, with daily trading volumes pulsating between HK$200-320 billion.