Highlights

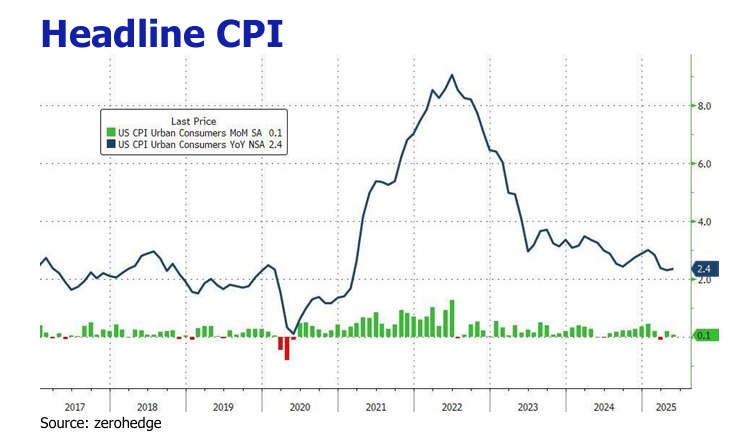

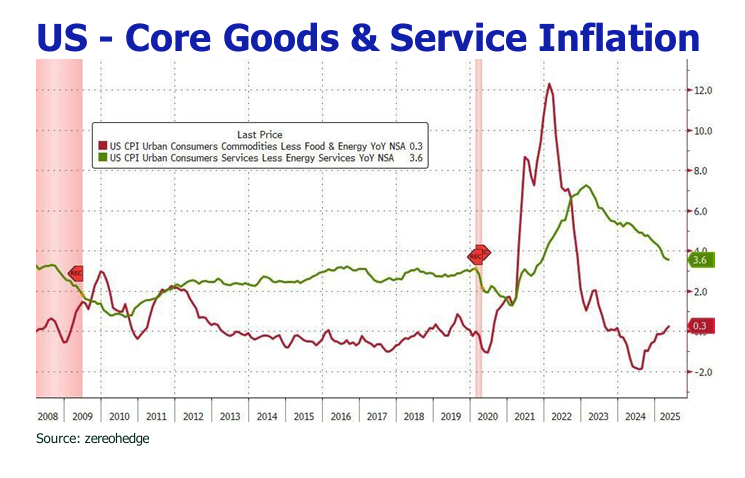

![]() U.S. CPI edged up marginally to 2.4% YoY in May (from 2.3% in April), with MoM growth slowing to 0.1% (from 0.2%), as firms absorbed costs or drew down inventories amid demand uncertainty.

U.S. CPI edged up marginally to 2.4% YoY in May (from 2.3% in April), with MoM growth slowing to 0.1% (from 0.2%), as firms absorbed costs or drew down inventories amid demand uncertainty.

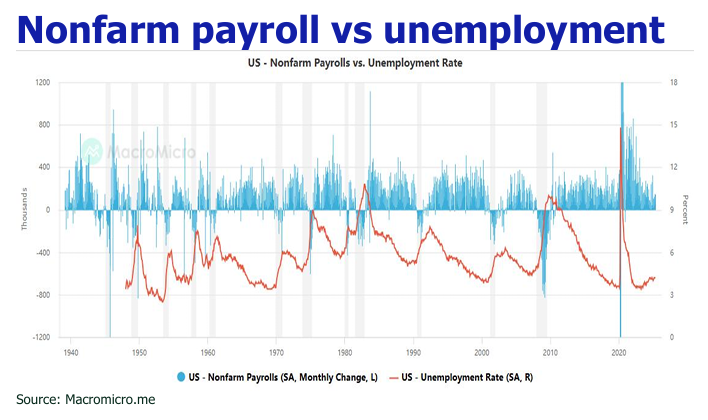

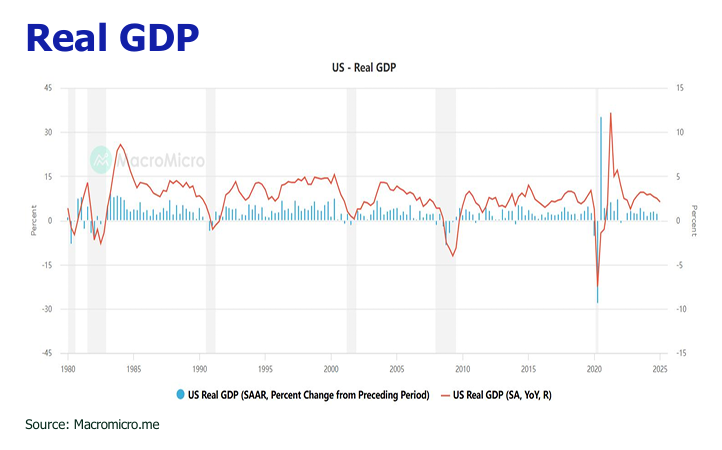

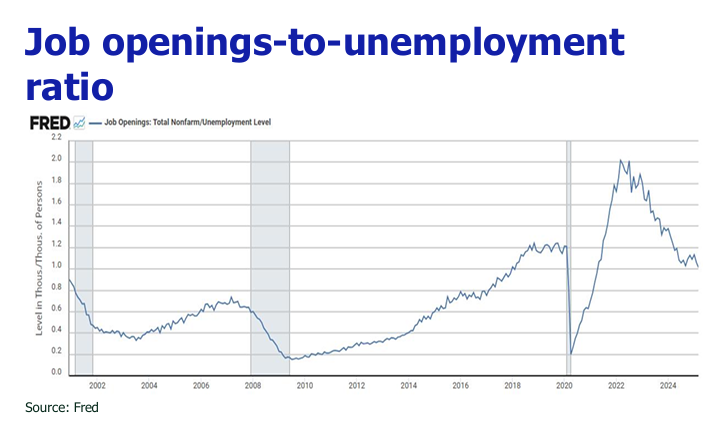

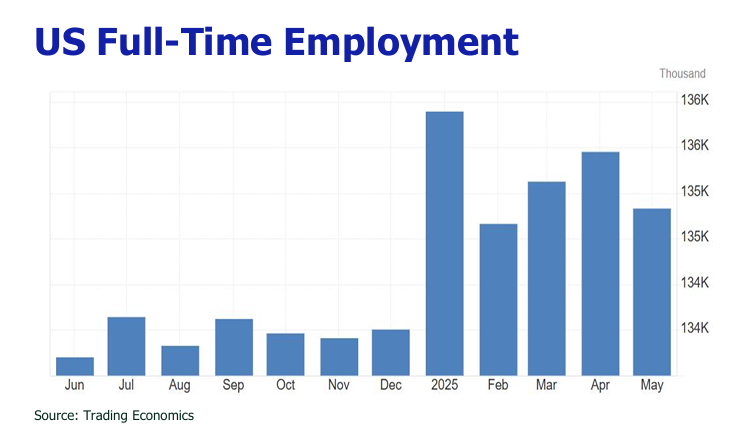

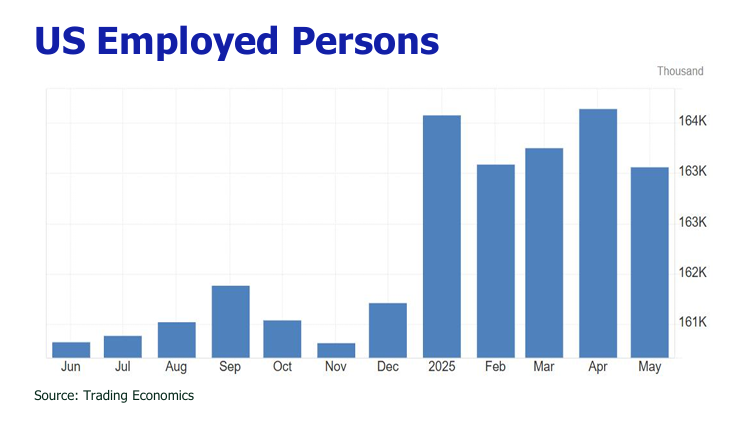

![]() Despite a seemingly benign nonfarm payroll print, the household survey revealed a concerning contraction in employed workers, exacerbated by persistent federal job cuts (22,000 in May, 59,000 YTD) and mounting corporate layoffs as firms recalibrate for prolonged tariff strains.

Despite a seemingly benign nonfarm payroll print, the household survey revealed a concerning contraction in employed workers, exacerbated by persistent federal job cuts (22,000 in May, 59,000 YTD) and mounting corporate layoffs as firms recalibrate for prolonged tariff strains.

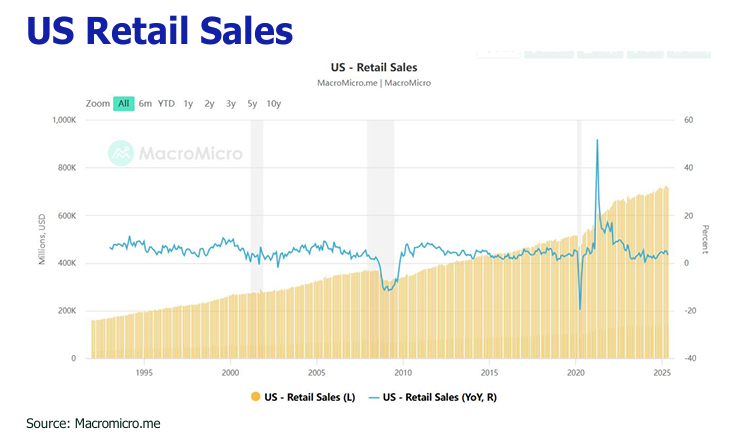

![]() Retail sales declined 0.9% MoM in May (following a revised-0.1% in April), dragged lower by energy price deflation and fading pre-tariff spending momentum.

Retail sales declined 0.9% MoM in May (following a revised-0.1% in April), dragged lower by energy price deflation and fading pre-tariff spending momentum.

![]() Crude surged ~15% in June on escalating Iran-Israel hostilities, Hormuz disruption risks, and potential Iranian supply curbs.

Crude surged ~15% in June on escalating Iran-Israel hostilities, Hormuz disruption risks, and potential Iranian supply curbs.

![]() Gold—historically a wartime outperformer (e.g., +35–50% in 1973, +10–15% in 1990)—is poised for a further upside, bolstered by safe-haven demand, oil-driven inflation expectations, and USD depreciation.

Gold—historically a wartime outperformer (e.g., +35–50% in 1973, +10–15% in 1990)—is poised for a further upside, bolstered by safe-haven demand, oil-driven inflation expectations, and USD depreciation.

![]() July–August risks accentuated economic softness due to seasonal lethargy, tariff moratorium expiry (July 8 deadline), ebbing consumer resilience and cascading corporate layoffs and federal austerity.

July–August risks accentuated economic softness due to seasonal lethargy, tariff moratorium expiry (July 8 deadline), ebbing consumer resilience and cascading corporate layoffs and federal austerity.

![]() The USD slumped 2.3% against the EUR and 1% on the DXY in June, with UBS forecasting a further 3.3% EUR appreciation and Morgan Stanley anticipating a 9% DXY plunge—consistent with our bearish verdict amid twin deficits, Fed rate cut dovishness, and global reserve diversification.

The USD slumped 2.3% against the EUR and 1% on the DXY in June, with UBS forecasting a further 3.3% EUR appreciation and Morgan Stanley anticipating a 9% DXY plunge—consistent with our bearish verdict amid twin deficits, Fed rate cut dovishness, and global reserve diversification.

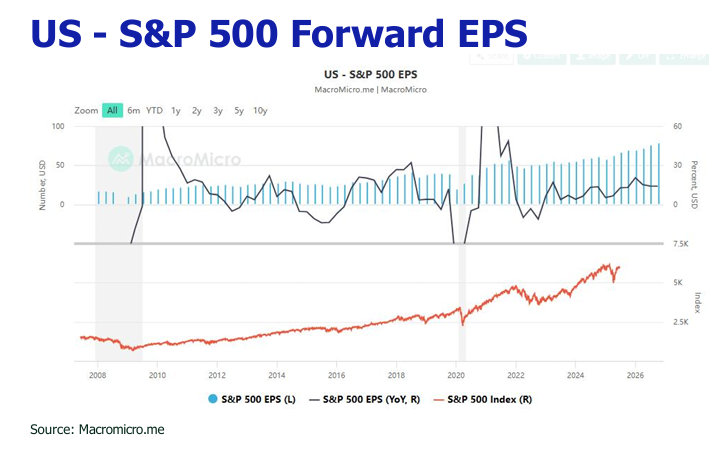

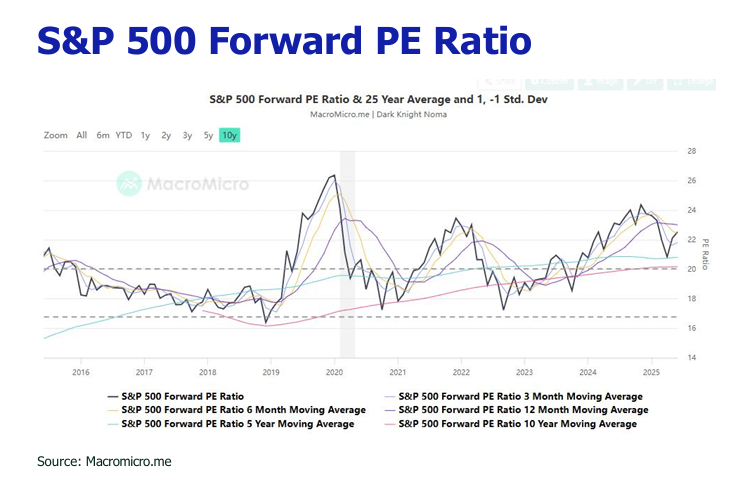

![]() S&P500is projected to experience muted gains or range-bound performance in Q3 2025. While more pronounced tariff shocks (higher inflation, labor market strain and weaker consumption) and Middle East tensions drive risk-off sentiment, AI-driven earnings growth to tech stocks, potential tariff detente (EU, Japan negotiations), Trump’s pro-business policies and deregulation, as well as dovish Fed rate cut signals (one or two times in 2025) will provide the counterbalance.

S&P500is projected to experience muted gains or range-bound performance in Q3 2025. While more pronounced tariff shocks (higher inflation, labor market strain and weaker consumption) and Middle East tensions drive risk-off sentiment, AI-driven earnings growth to tech stocks, potential tariff detente (EU, Japan negotiations), Trump’s pro-business policies and deregulation, as well as dovish Fed rate cut signals (one or two times in 2025) will provide the counterbalance.

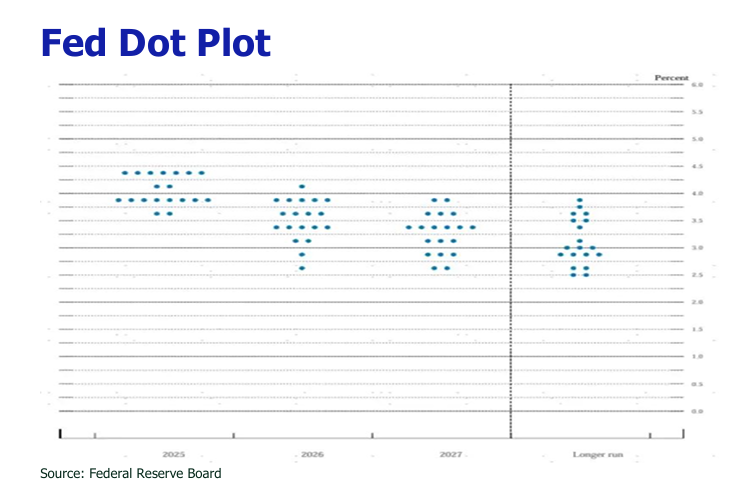

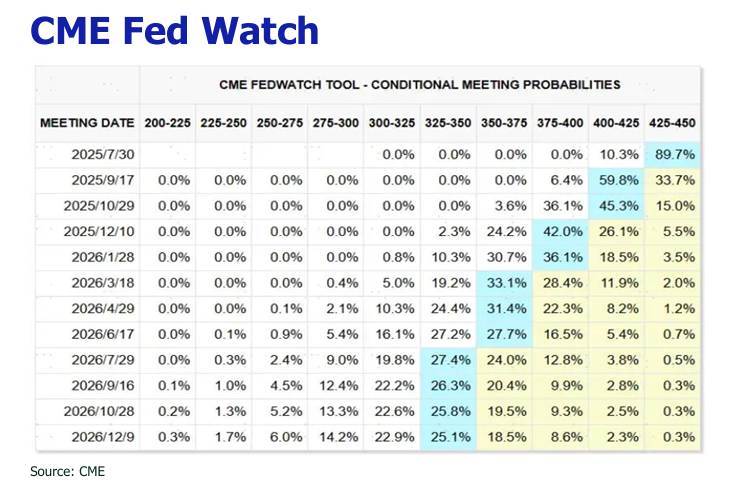

![]() Fedwill stand pat for rate cut, adopting a cautious stance as it evaluates the economic impact of ongoing trade negotiations, particularly with the EU and China, through July and August.

Fedwill stand pat for rate cut, adopting a cautious stance as it evaluates the economic impact of ongoing trade negotiations, particularly with the EU and China, through July and August.

![]() InJune, the Hang Seng Index rose from 23,290 to approximately 24,200 points, driven by tech stock gains, the U.S.-China tariff truce, and post-ceasefire oil price declines with daily volume sustaining HK$200-300B.

InJune, the Hang Seng Index rose from 23,290 to approximately 24,200 points, driven by tech stock gains, the U.S.-China tariff truce, and post-ceasefire oil price declines with daily volume sustaining HK$200-300B.