Highlights

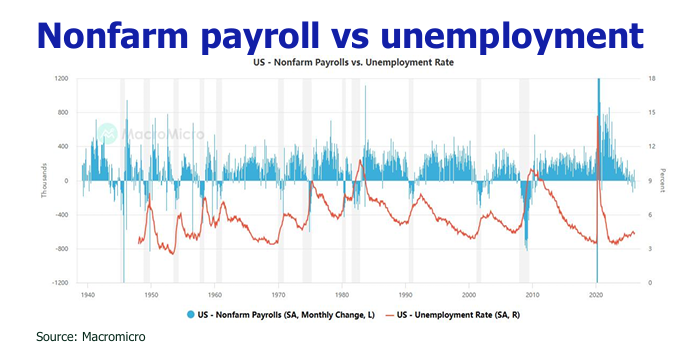

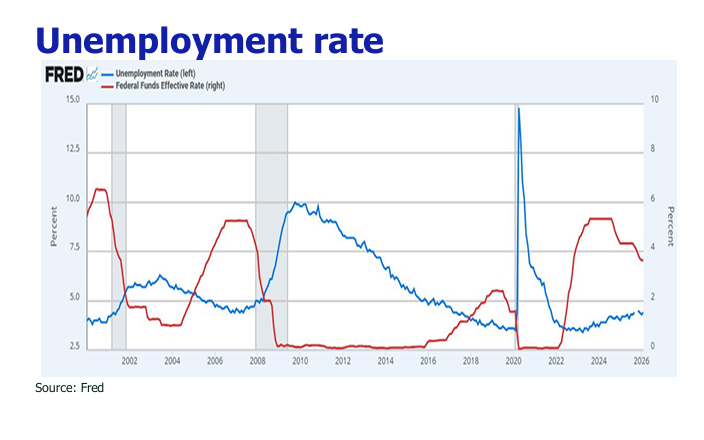

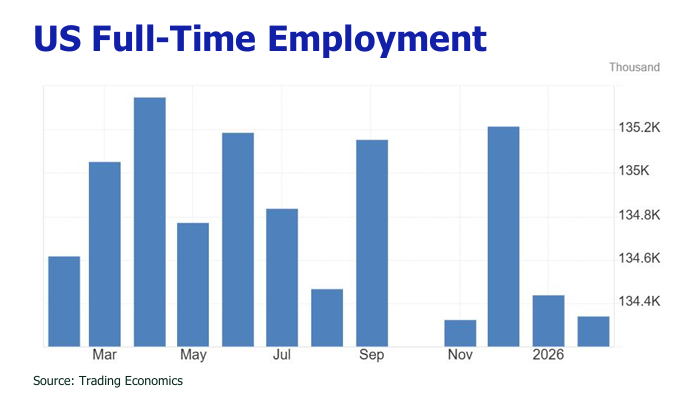

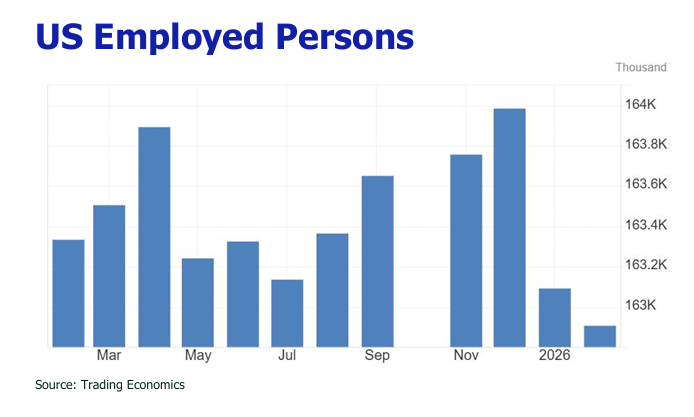

![]() Nonfarm payrolls fell by 92,000 in February—the third decline in five months—with unemployment rising to 4.4%, the highest since November of the prior year.

Nonfarm payrolls fell by 92,000 in February—the third decline in five months—with unemployment rising to 4.4%, the highest since November of the prior year.

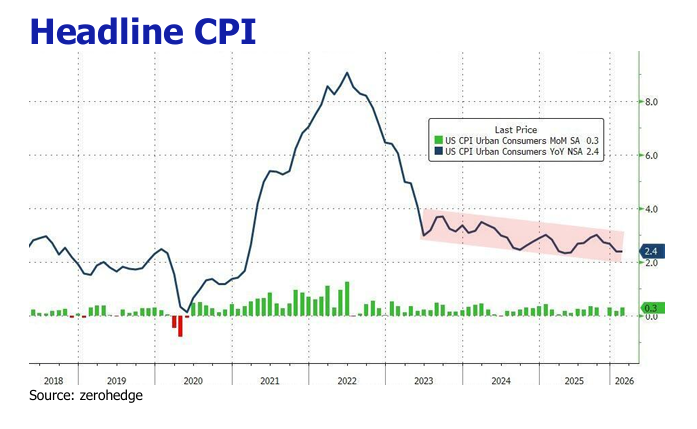

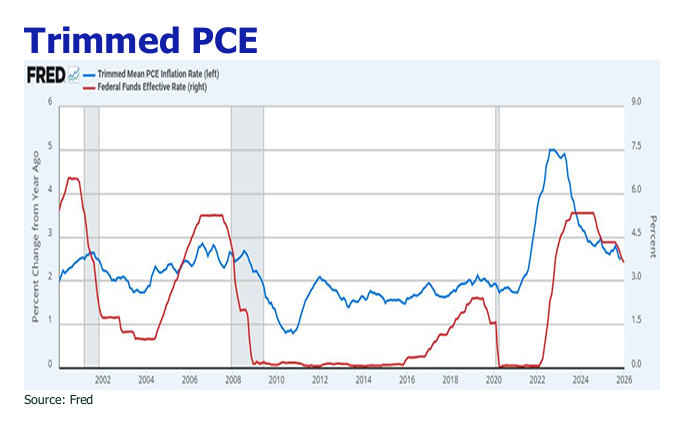

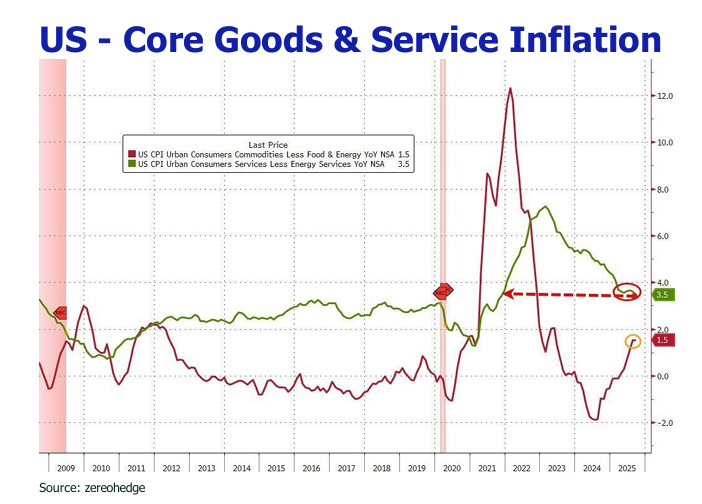

![]() Headline and core inflation held steady at 2.4% and 2.5% year-over-year, respectively, with monthly gains of 0.3% and 0.2%.

Headline and core inflation held steady at 2.4% and 2.5% year-over-year, respectively, with monthly gains of 0.3% and 0.2%.

![]() Brent crude surged over 23% to $110/bbl, gold tumbled 16–20%, silver plunged 22–30%, driven by the Federal Reserve’s pivot to higher-for-longer rates, a strong dollar, and fears of reduced industrial demand.

Brent crude surged over 23% to $110/bbl, gold tumbled 16–20%, silver plunged 22–30%, driven by the Federal Reserve’s pivot to higher-for-longer rates, a strong dollar, and fears of reduced industrial demand.

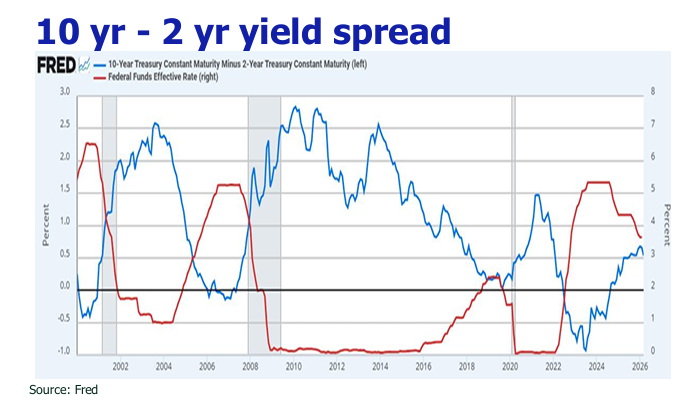

![]() US markets slid 5%; China’s benchmarks shed 4–6%; Japan’s Nikkei fell 5–7%, Korea’s KOSPI plunged 6–8% as the US 10-year yield hit 4.40%.

US markets slid 5%; China’s benchmarks shed 4–6%; Japan’s Nikkei fell 5–7%, Korea’s KOSPI plunged 6–8% as the US 10-year yield hit 4.40%.

![]() The U.S. dollar strengthened (+3%) significantly as a safe haven, while the Japanese yen (-1.9%) and South Korean won (-4.1%) weakened under the pressure of soaring energy import costs and economic vulnerability.

The U.S. dollar strengthened (+3%) significantly as a safe haven, while the Japanese yen (-1.9%) and South Korean won (-4.1%) weakened under the pressure of soaring energy import costs and economic vulnerability.

![]() Severe supply constraints and insufficient mitigation measures are expected to keep oil prices elevated above $100 per barrel for the near term, with potential for extreme spikes to $130-$150 if supply disruptions continue longer than anticipated.

Severe supply constraints and insufficient mitigation measures are expected to keep oil prices elevated above $100 per barrel for the near term, with potential for extreme spikes to $130-$150 if supply disruptions continue longer than anticipated.

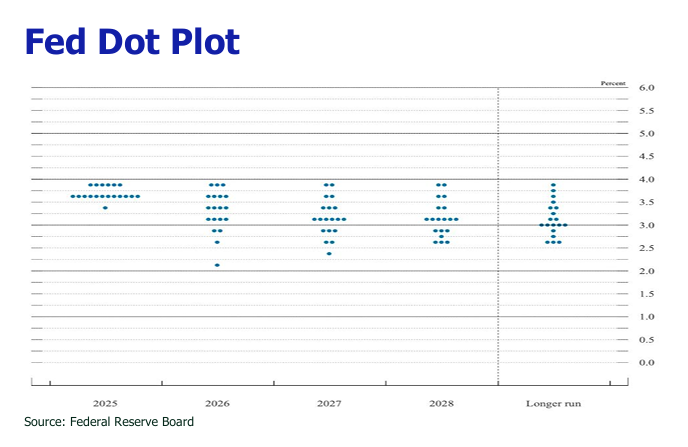

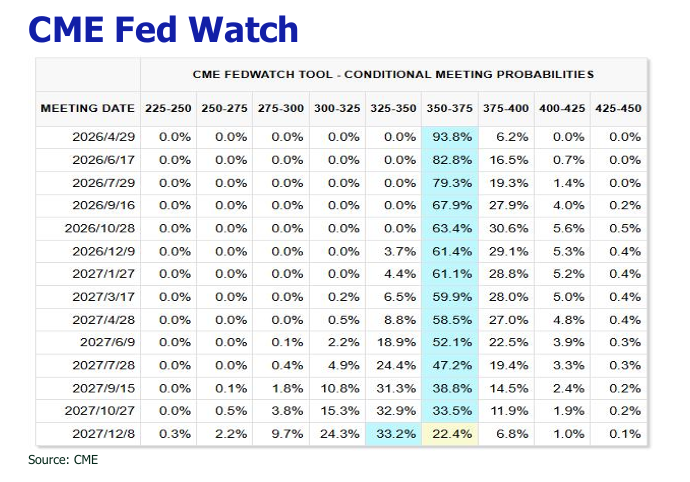

![]() The Federal Reserve is expected to delay rate cuts until late 2026, with the possibility of no easing at all if oil prices surge further.

The Federal Reserve is expected to delay rate cuts until late 2026, with the possibility of no easing at all if oil prices surge further.

![]() Weak labor market data and political pressure will likely prevent the Fed from hiking rates, forcing it to tolerate temporary inflation to avoid triggering a recession.

Weak labor market data and political pressure will likely prevent the Fed from hiking rates, forcing it to tolerate temporary inflation to avoid triggering a recession.

![]() Rising stagflation risks favor defensive investment strategies, shifting focus away from traditional growth stocks toward energy, gold, and value sectors.

Rising stagflation risks favor defensive investment strategies, shifting focus away from traditional growth stocks toward energy, gold, and value sectors.

![]() The Hang Seng Index dived 6% to around 25000, with daily turnover surging to HK$250-400 billion, driven by global risk-off positioning.

The Hang Seng Index dived 6% to around 25000, with daily turnover surging to HK$250-400 billion, driven by global risk-off positioning.