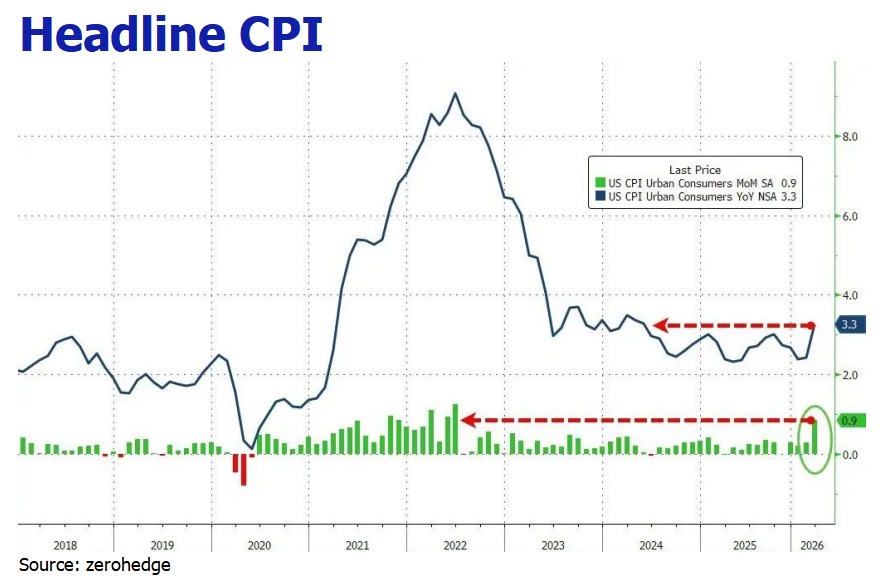

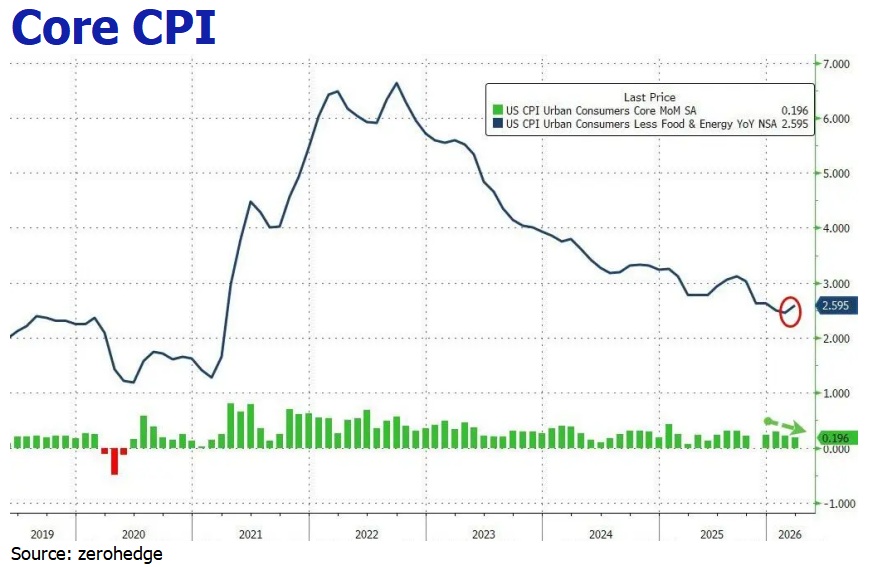

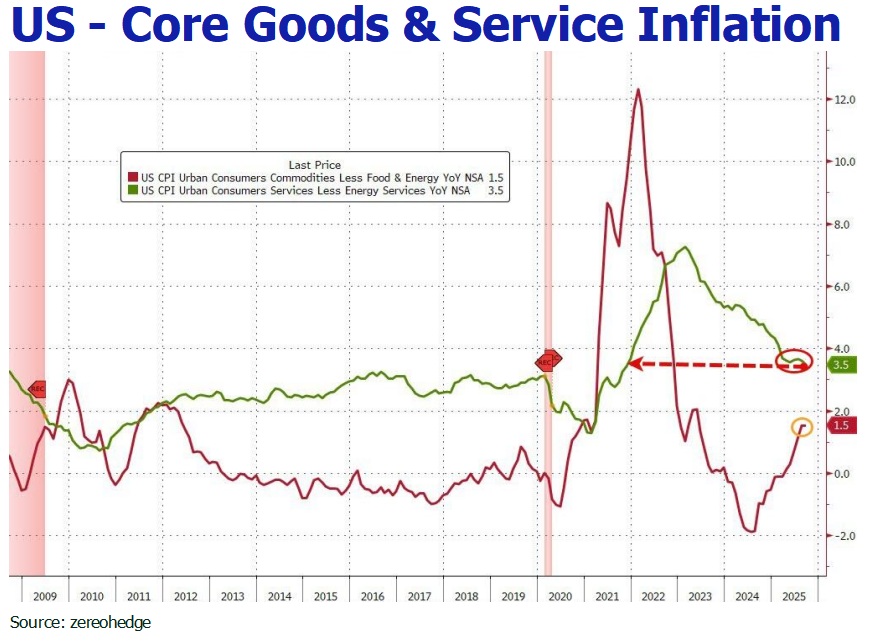

1.Inflation continues to creep up in May

Despite the significant pullback in oil prices during April, we predict US inflation will mount in May due to secondary transmission effects. Generally, oil prices affect consumer inflation with a lag of two to three months as higher energy costs ripple through the supply chain. Once inflation passes through the initial layer of gasoline, jet fuel, and diesel, it impacts airline fares, transportation costs, and shipping surcharges. Eventually, these costs filter into fertilizer and plastics, and finally, food prices.

2.A prolonged period of US-Iran tension

A US-Iran deal is likely to remain deadlocked in the short run due to several irreconcilable disagreements, including demands for nuclear abandonment, a halt to funding for regional groups like Hamas and Hezbollah, guarantees against future attacks from the US, and Iranian demands for sanctions relief and access to frozen assets.

The US naval blockade—and Iran’s resumed closure of the Strait—have further hardened positions, as both sides seek economic leverage to secure a deal favorable to their interests. Iran has publicly insisted that President Trump lift the blockade on ships entering or exiting Iranian ports in the Strait before Tehran will engage in new talks. Trump has resisted this demand, insisting a final deal must come first.

We believe the US has signaled a strong reluctance to escalate military action in response to threatened missile attacks on Gulf oil facilities. Instead, Washington is resorting to intercepting Iranian oil exports as a lever to pressure Tehran back to the table.

However, Iran will not simply submit to US terms, as the regime views capitulation as an existential threat. If the US blocks its oil exports and Iran feels economically suffocated, it can fight back through multiple channels: smuggling oil via land routes and ghost tankers, threatening to mine the Strait of Hormuz, and launching proxy warfare through the Houthis, Syria, and Hezbollah. By threatening global energy supplies and regional stability through its proxies while simultaneously building economic resilience and opening diplomatic backchannels, Tehran aims to make any confrontation or continued economic strangulation so costly, protracted, and disruptive that the US is ultimately compelled to seek a diplomatic solution on more favorable terms.

3.Oil, gold, and equities to stay volatile

Oil: Prices are elevated and unstable, with Brent at $106/bbl and WTI at $96/bbl. The closure of the Strait of Hormuz, which previously handled roughly 20 million barrels per day, continues to tighten supply. If the blockade persists, prices could challenge $150 per barrel. Any headline regarding diplomatic progress or military escalation is likely to trigger sharp swings.

Gold: Volatility is being driven by a paradoxical environment. While geopolitical crises typically boost safe-haven demand, the oil shock has intensified inflation fears, leading markets to price in potential rate hikes rather than cuts. This creates a headwind for non-yielding gold. We expect gold prices to remain range-bound (roughly $4,500–$4,850) until credible prospects for peace emerge.

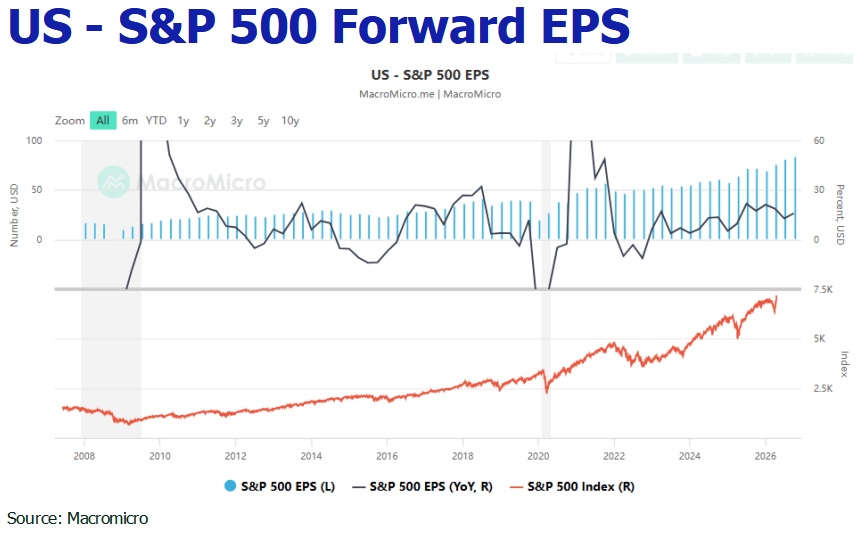

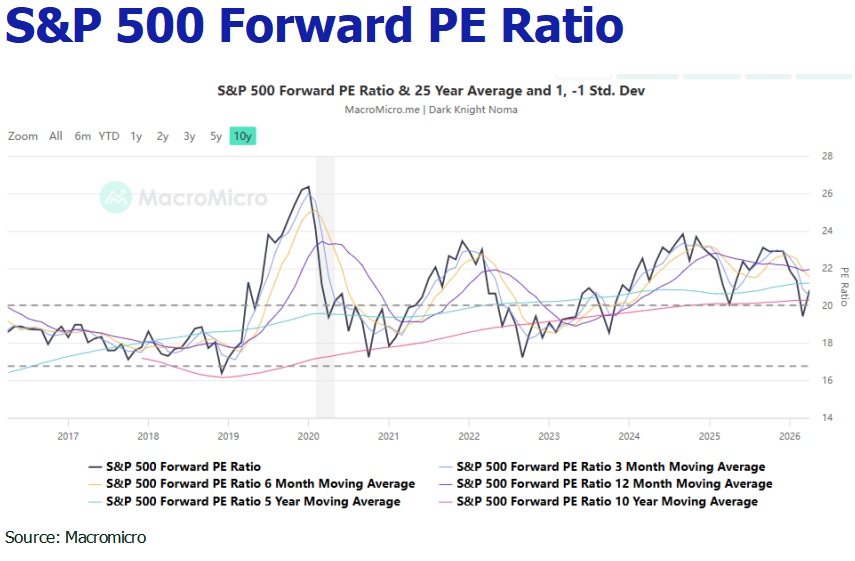

Equities: The market is currently buoyed by resilient Q1 corporate earnings and intense AI enthusiasm. However, a failure to reach a new US-Iran deal and a prolonged closure of the Strait of Hormuz would drive oil prices higher. This could spark stagflation—reigniting rate hike risks, deterring economic growth, and weighing heavily on equity valuations.