Highlights

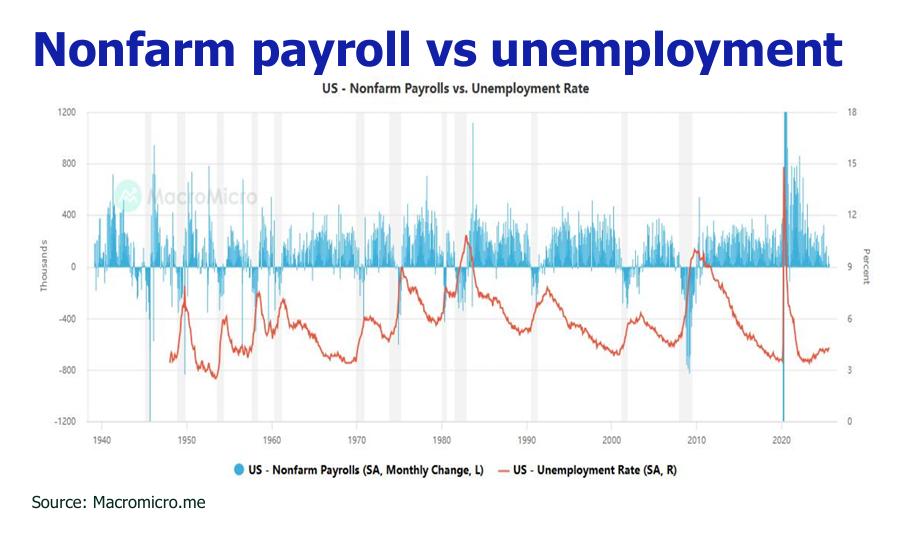

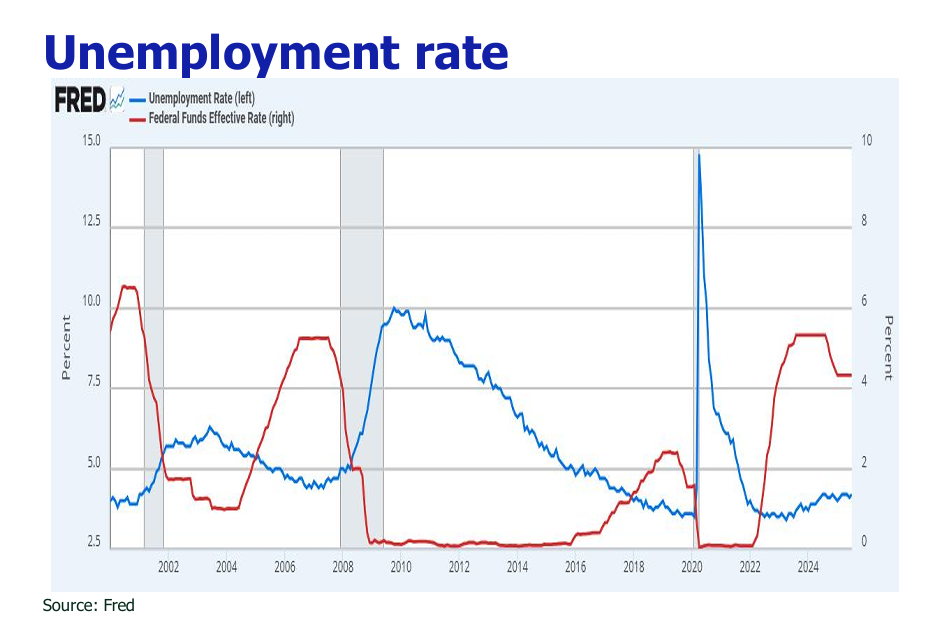

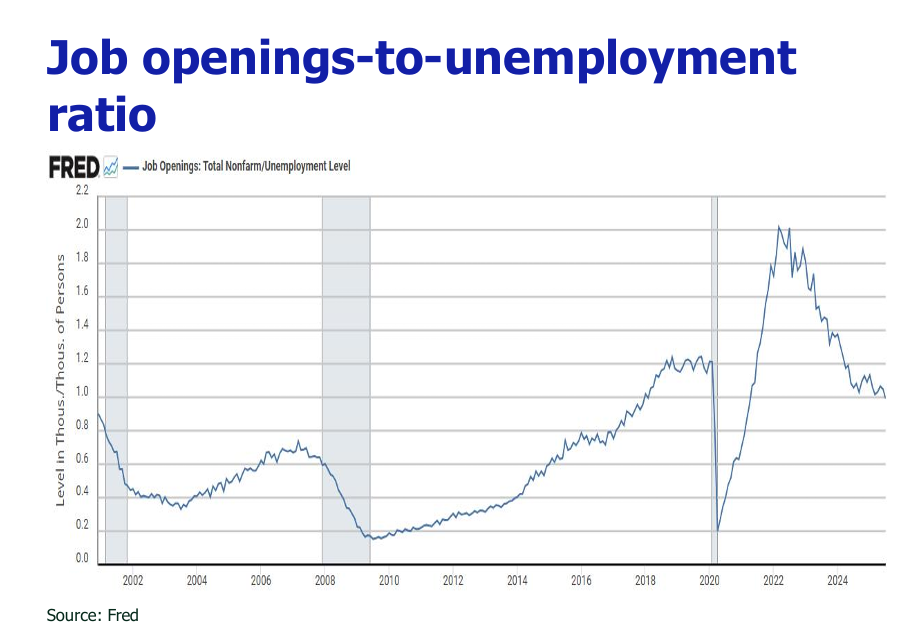

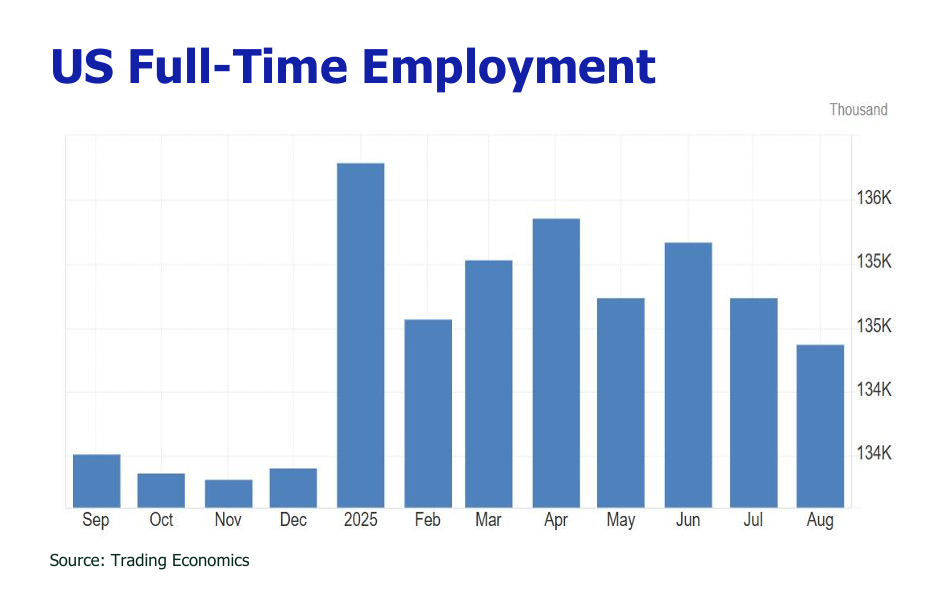

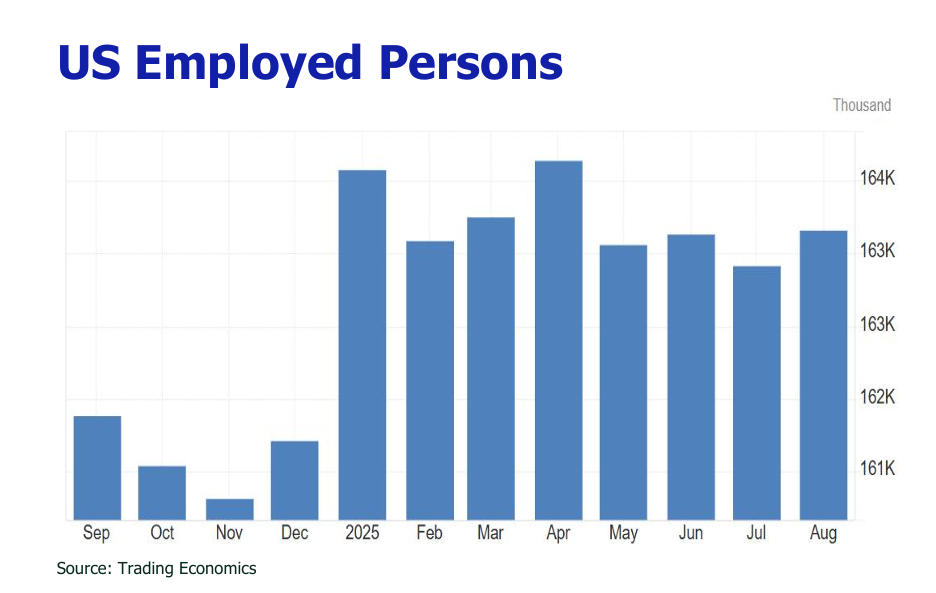

![]() August’s paltry 22,000 job growth and upward-trending unemployment rate to 4.3% signify a pronounced deceleration, exacerbated by whopping downward benchmark revisions and an ominous shift from full-time to part-time employment.

August’s paltry 22,000 job growth and upward-trending unemployment rate to 4.3% signify a pronounced deceleration, exacerbated by whopping downward benchmark revisions and an ominous shift from full-time to part-time employment.

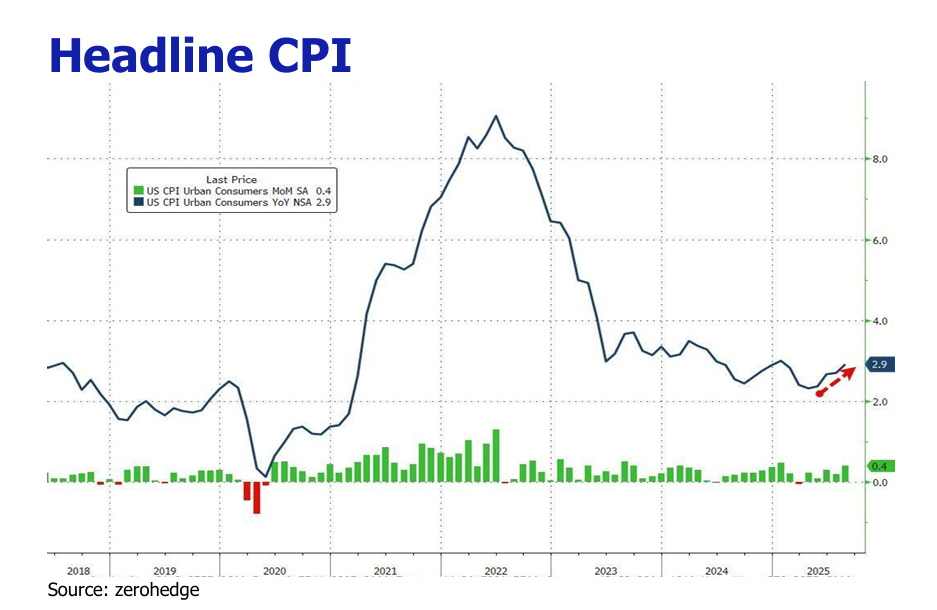

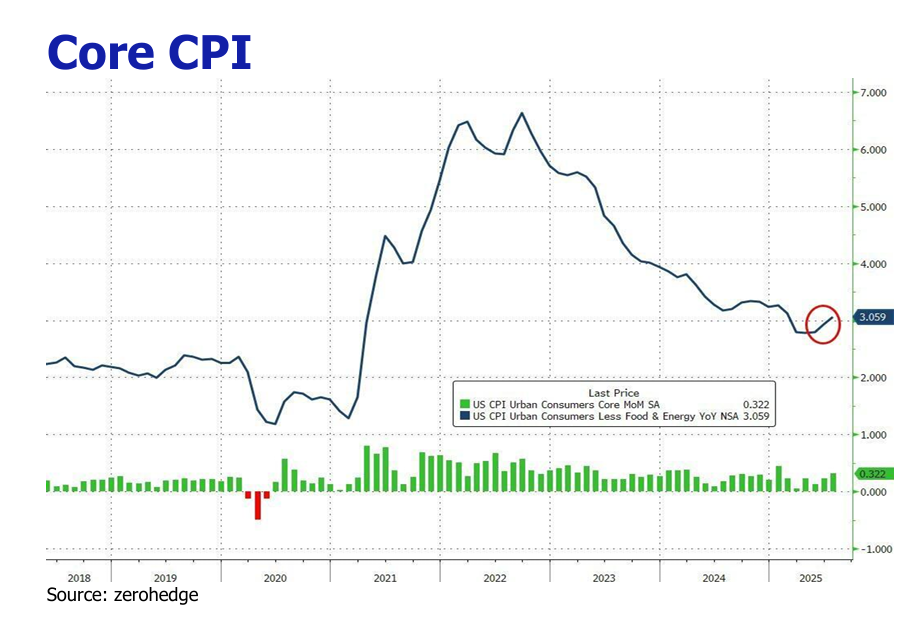

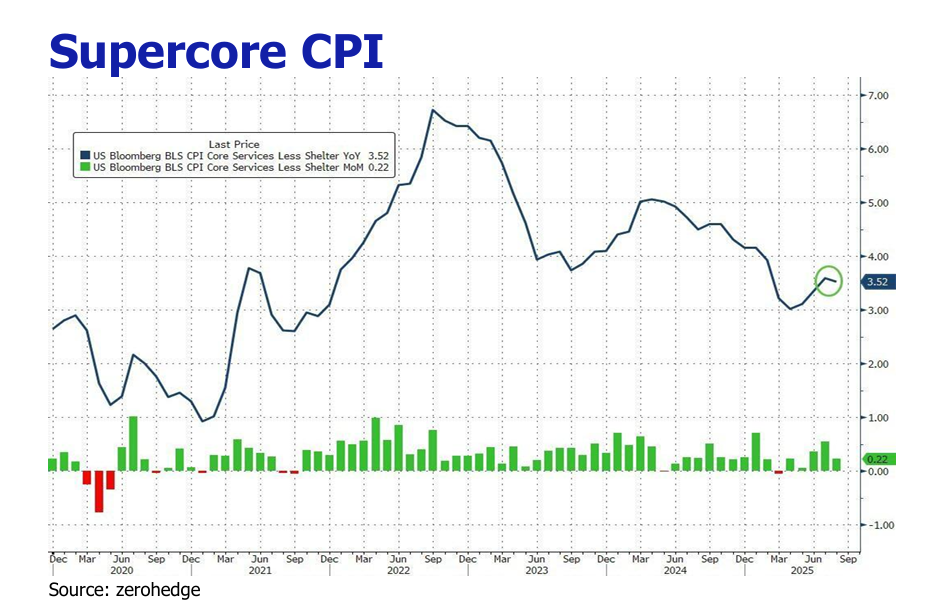

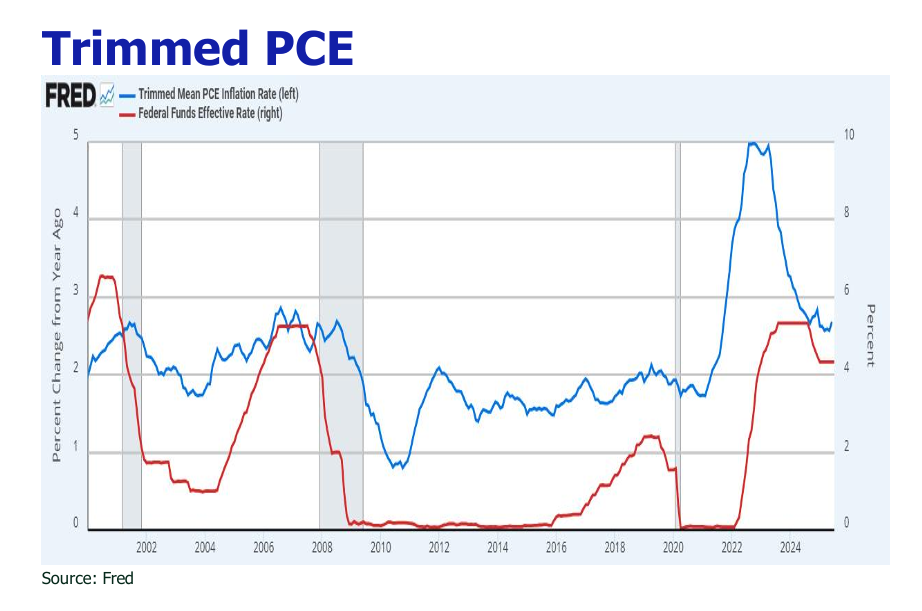

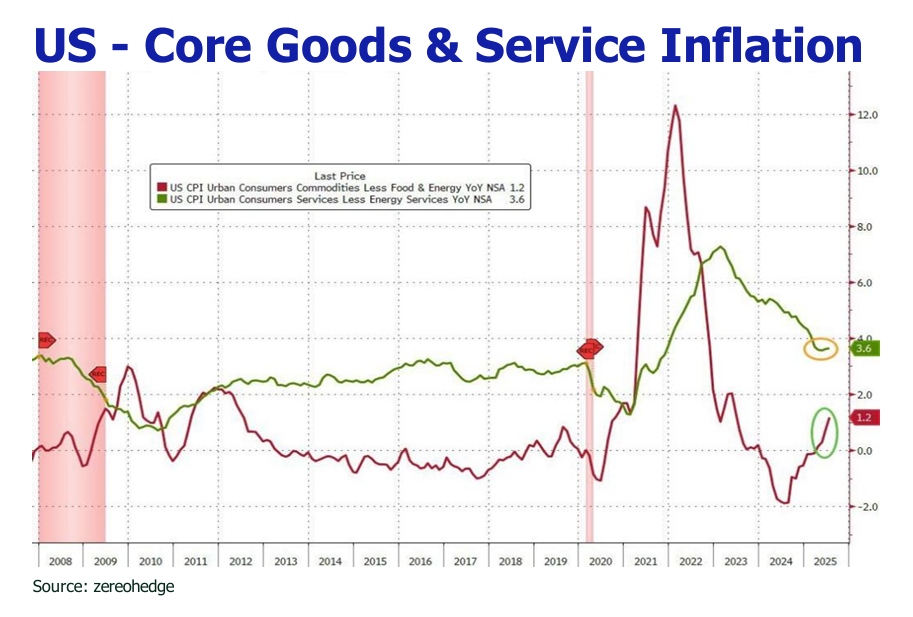

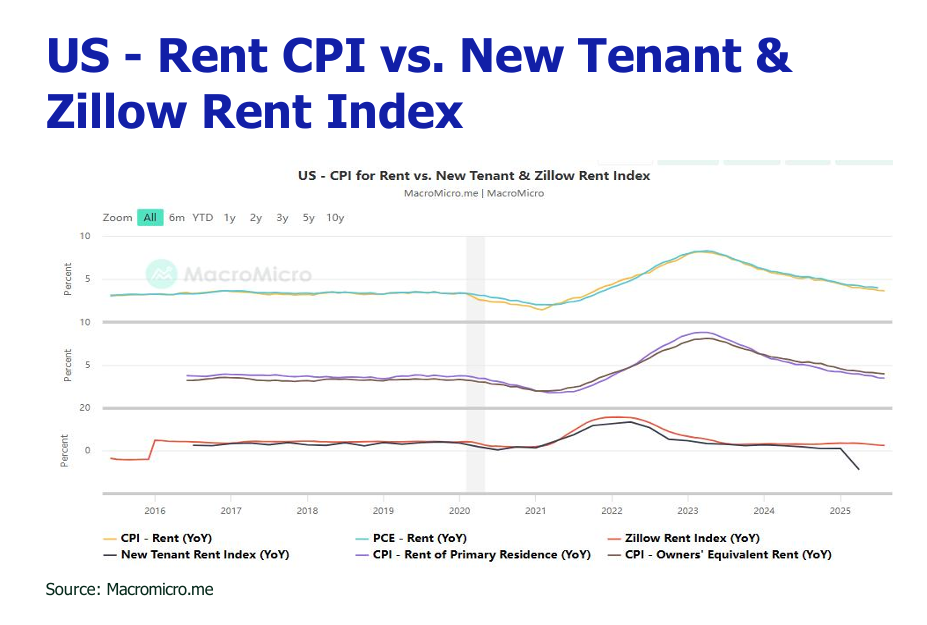

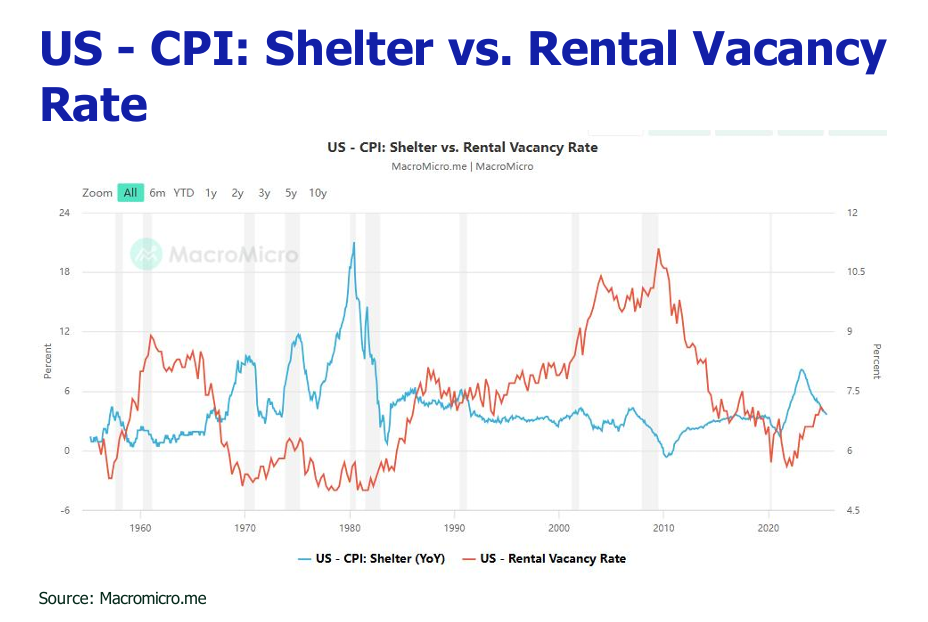

![]() The acceleration in headline CPI with 0.2% YoY and MoM upticks compared to July, underscores the entrenchment of inflationary pressures, with the pronounced passthrough of tariffs into core goods prices signaling an incipient broadening of price gains beyond shelter and food.

The acceleration in headline CPI with 0.2% YoY and MoM upticks compared to July, underscores the entrenchment of inflationary pressures, with the pronounced passthrough of tariffs into core goods prices signaling an incipient broadening of price gains beyond shelter and food.

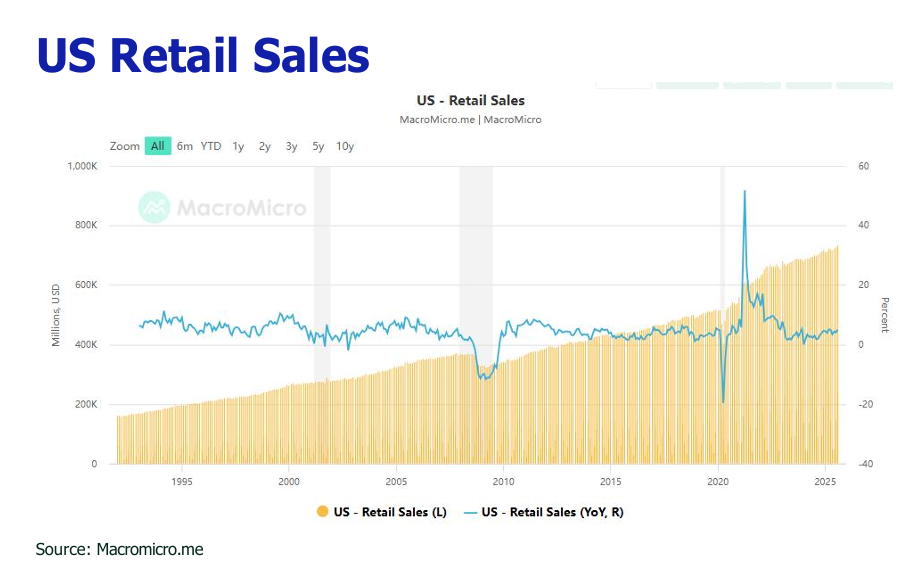

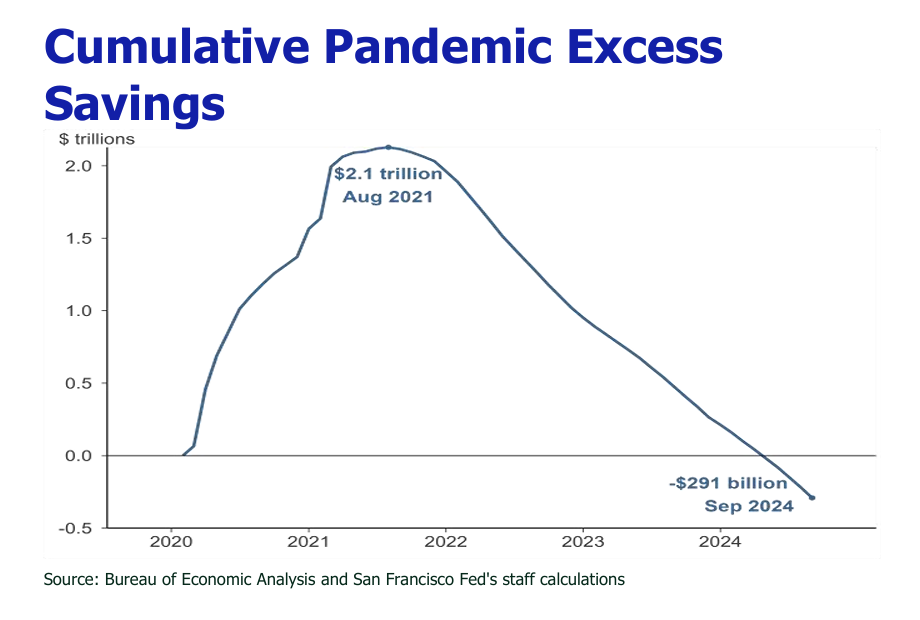

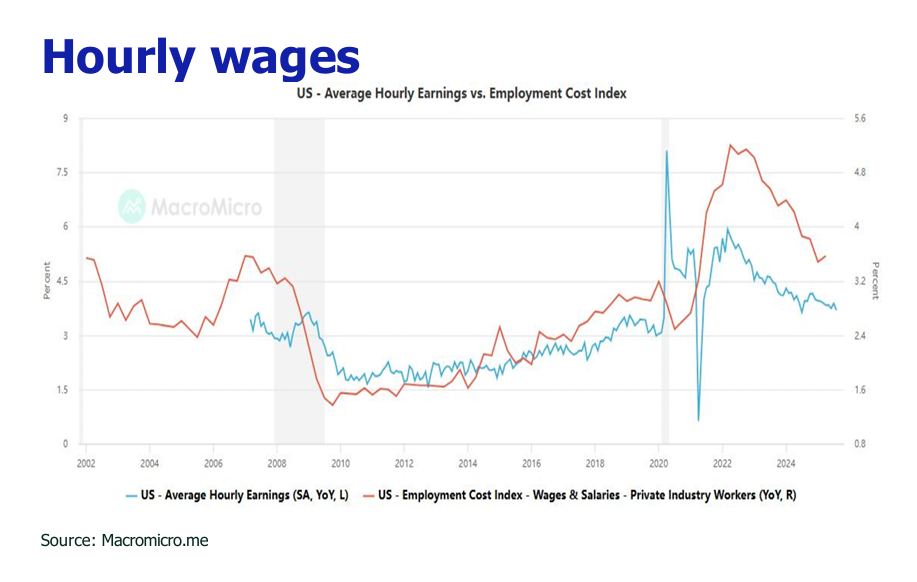

![]() Robust retail sales stay afloat by sustained wage growth and robust equity markets, countervailing headwinds from a softening labor market and tariff-induced inflation.

Robust retail sales stay afloat by sustained wage growth and robust equity markets, countervailing headwinds from a softening labor market and tariff-induced inflation.

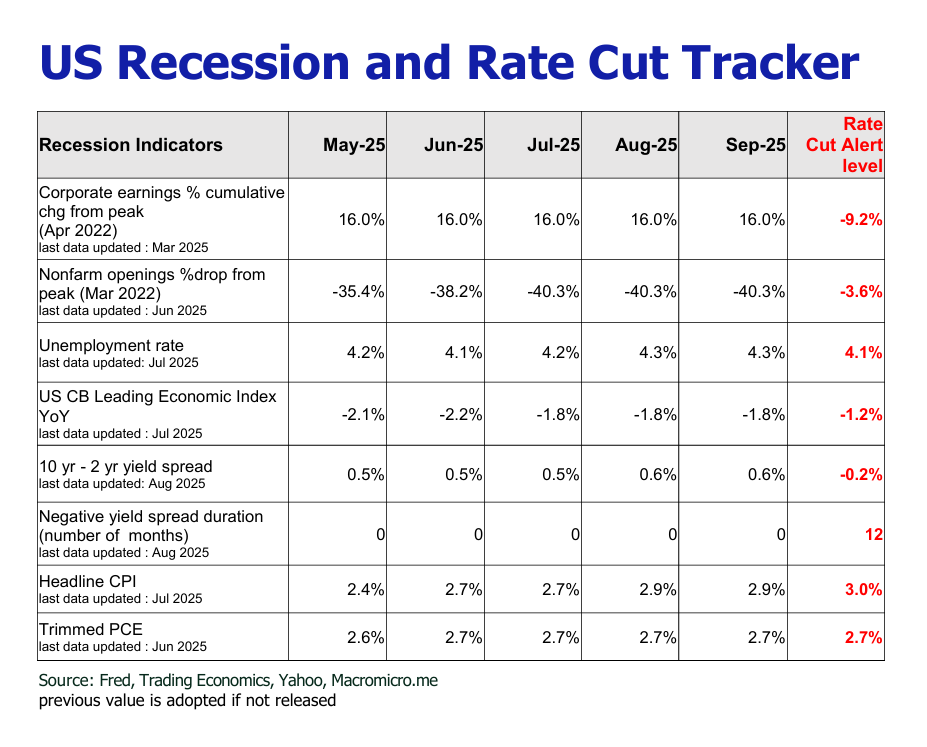

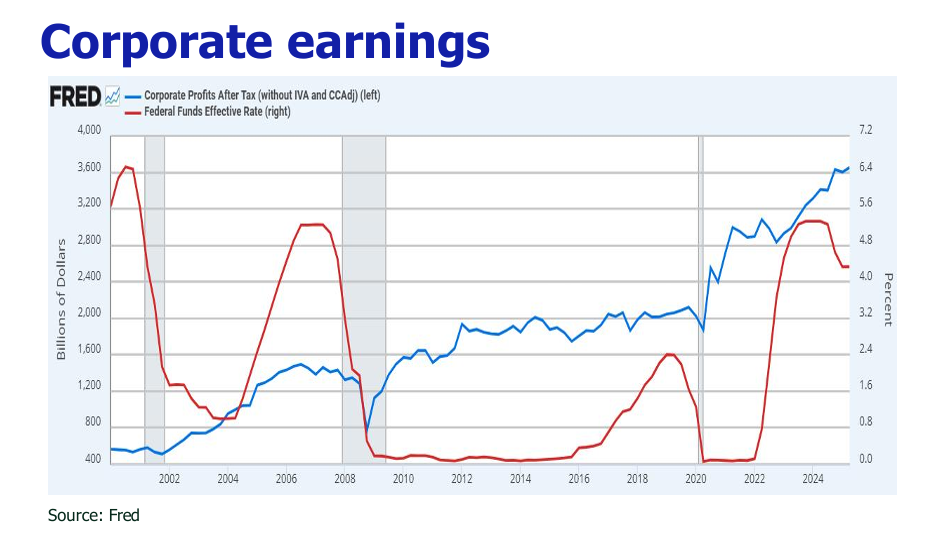

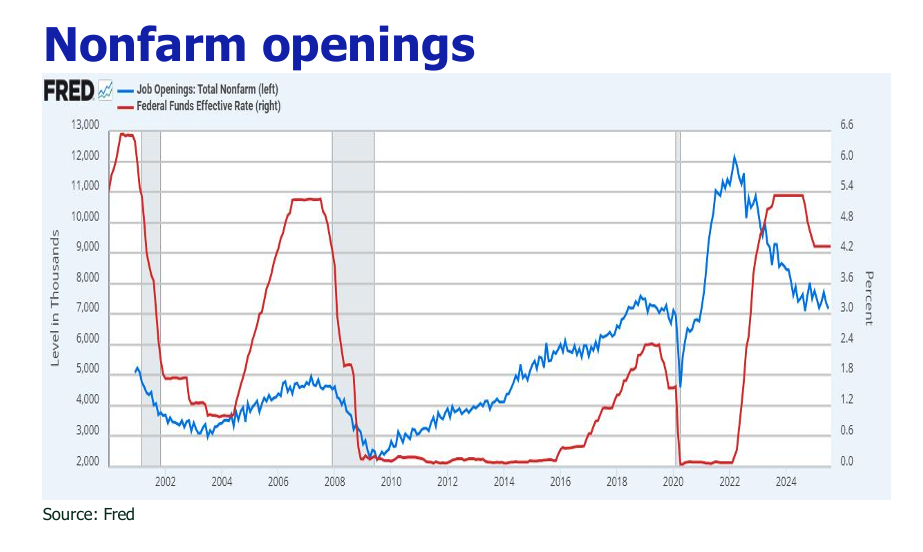

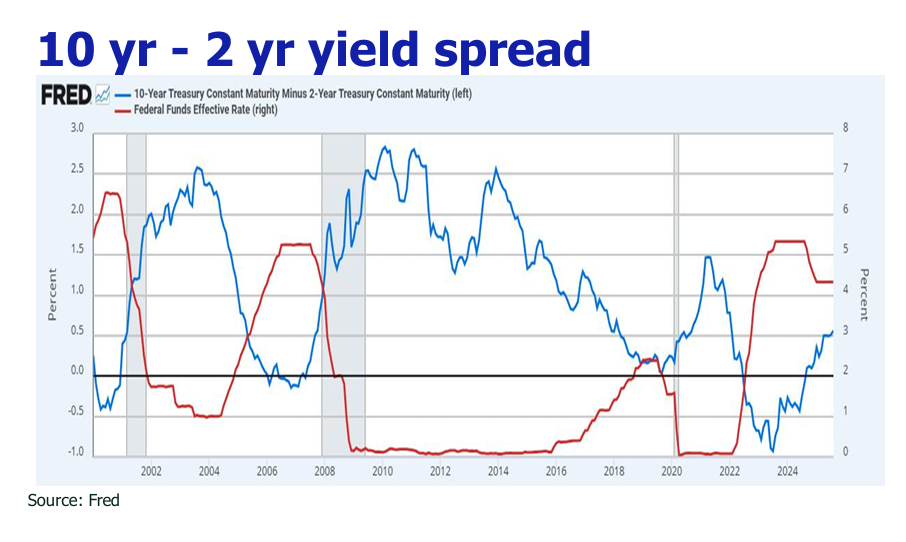

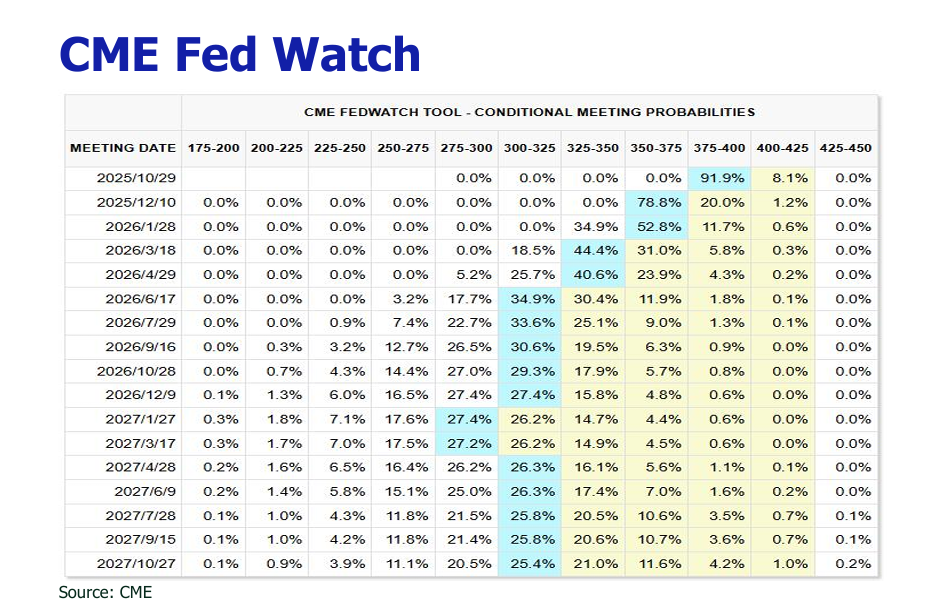

![]() Three or two additional rate cuts are contingent on the wrestling between deteriorating labor metrics and persistent inflation.

Three or two additional rate cuts are contingent on the wrestling between deteriorating labor metrics and persistent inflation.

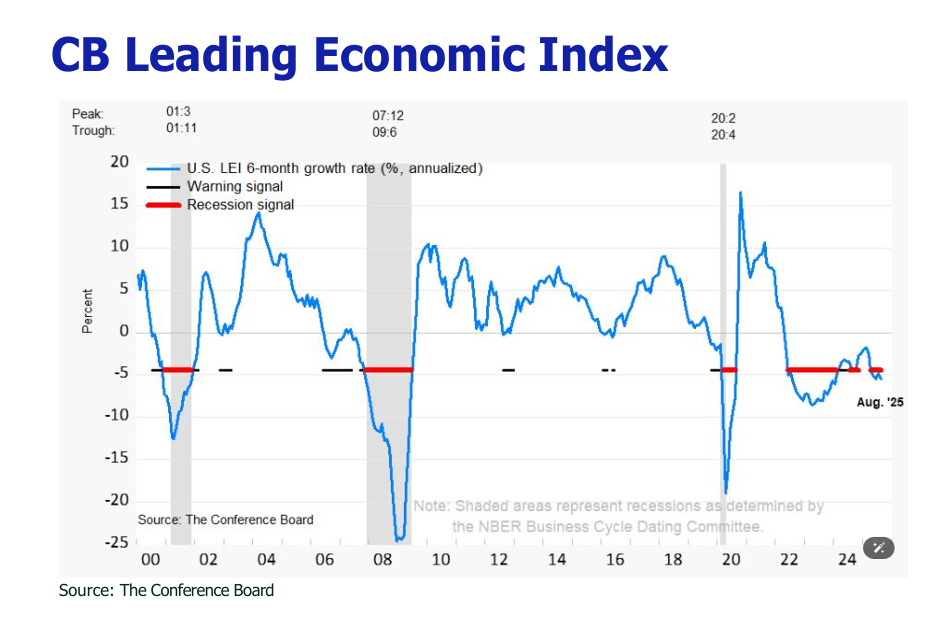

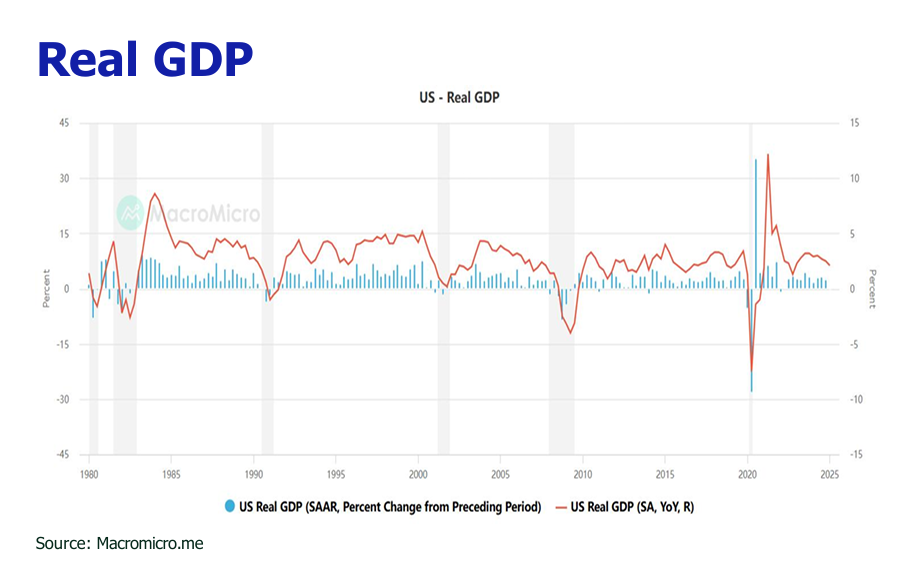

![]() Buoyant PMI data and strong Q2 GDP growth bolster the narrative of a non-recessionary expansion.

Buoyant PMI data and strong Q2 GDP growth bolster the narrative of a non-recessionary expansion.

![]() Rate reductions are bound to undermine the USD (to 95), elevate the EUR (to 1.2), and bolster gold (targeting $4,000/oz by mid-2026) and cryptocurrencies (BTC to $124,000-$210,000 by year-end).

Rate reductions are bound to undermine the USD (to 95), elevate the EUR (to 1.2), and bolster gold (targeting $4,000/oz by mid-2026) and cryptocurrencies (BTC to $124,000-$210,000 by year-end).

![]() Historical precedent suggests that “insurance” rate cuts during non-recessionary periods have presaged significant equity appreciation, with the S&P 500 aiming for 6,800-7,100 by end-2025 and 7,000-7,500 by end-2026.

Historical precedent suggests that “insurance” rate cuts during non-recessionary periods have presaged significant equity appreciation, with the S&P 500 aiming for 6,800-7,100 by end-2025 and 7,000-7,500 by end-2026.

![]() The HSI gained 3.4% in August, carving out an on-ramp to 28,000 in 2025 and 30,000 in 2026, propelled by US ongoing monetary easing, China’s AI progression and U.S.-China tariff truce optimism.

The HSI gained 3.4% in August, carving out an on-ramp to 28,000 in 2025 and 30,000 in 2026, propelled by US ongoing monetary easing, China’s AI progression and U.S.-China tariff truce optimism.