Highlights

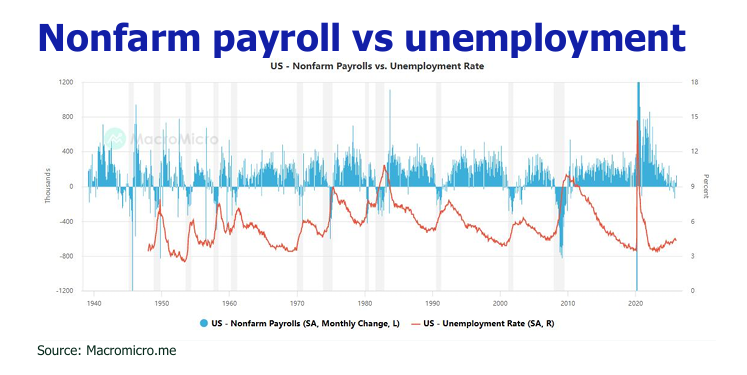

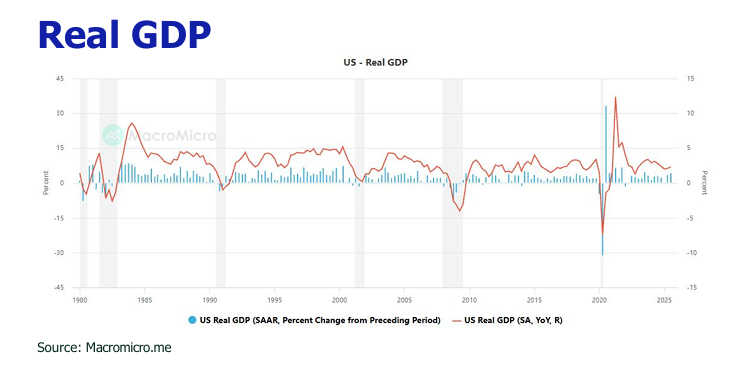

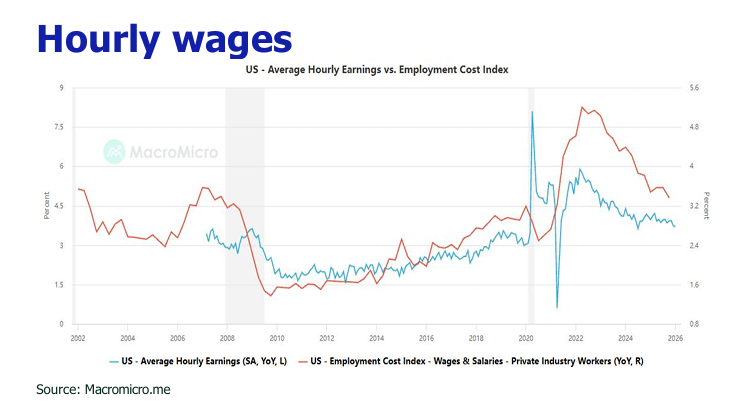

![]() January NFP rebounded to +130,000, improving on Dec’s revised +48,000, with unemployment dipping to 4.3%, yet strength is contested due to massive prior downward revisions.

January NFP rebounded to +130,000, improving on Dec’s revised +48,000, with unemployment dipping to 4.3%, yet strength is contested due to massive prior downward revisions.

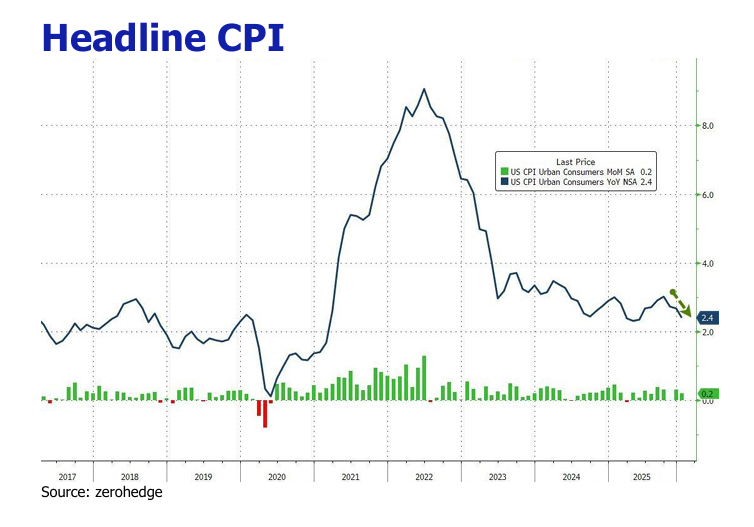

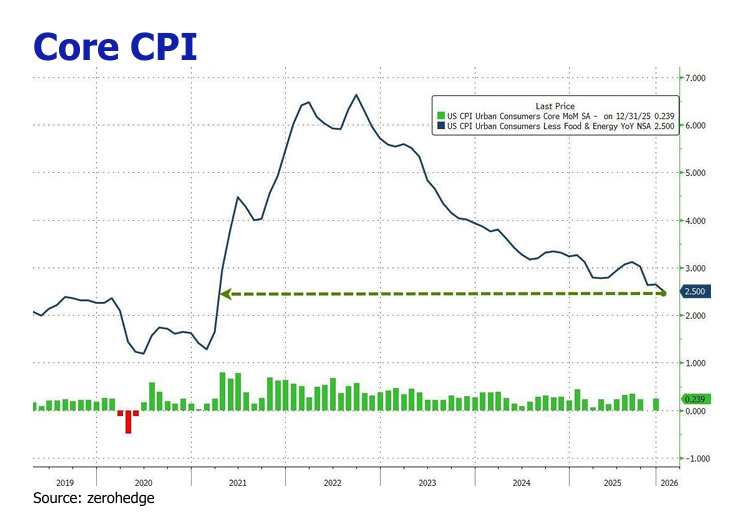

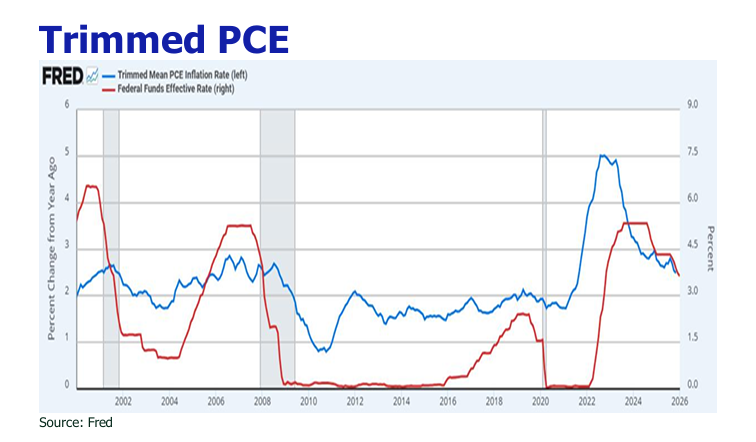

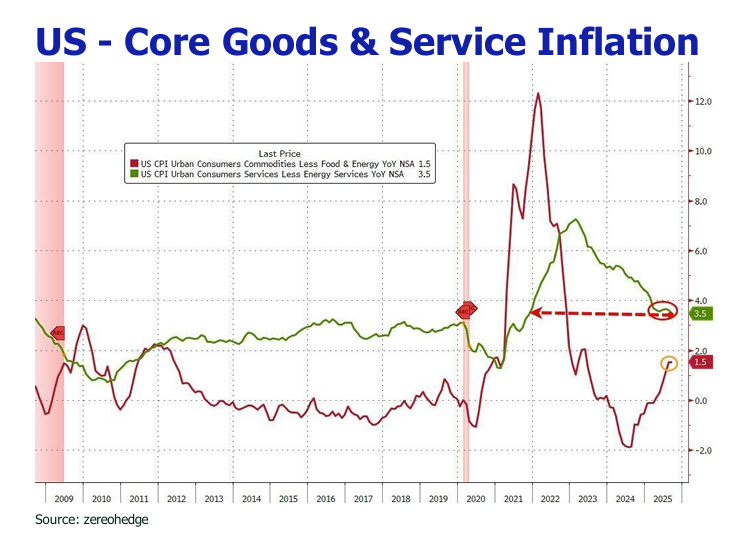

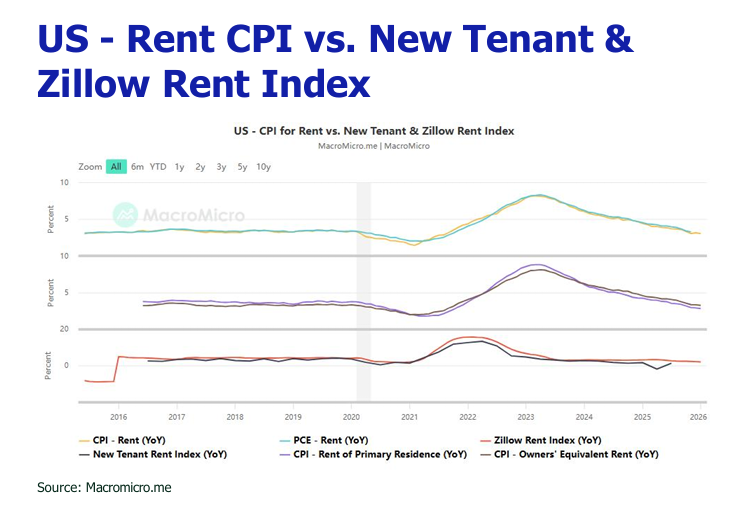

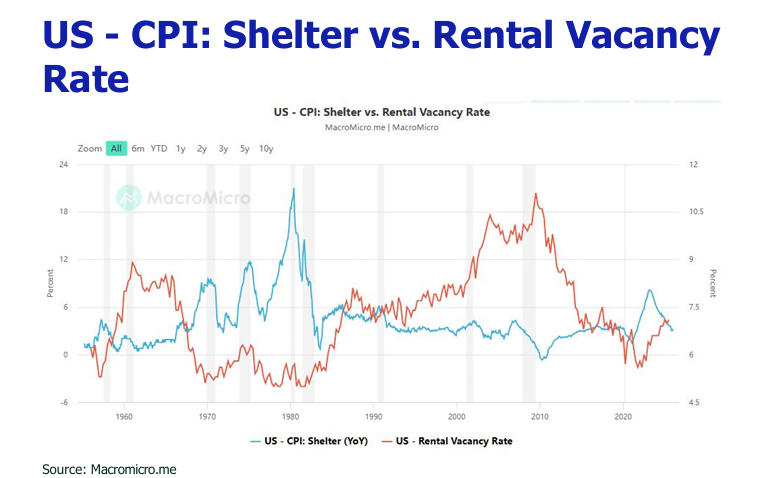

![]() Headline CPI cooled to 2.4% YoY and core CPI to 2.5% YoY, with broad-based relief across food, energy, shelter, and used cars.

Headline CPI cooled to 2.4% YoY and core CPI to 2.5% YoY, with broad-based relief across food, energy, shelter, and used cars.

![]() The Greenland acquisition hiccup has ignited a conflict that menaces U.S.-EU trade with the prospect of severe tariffs.

The Greenland acquisition hiccup has ignited a conflict that menaces U.S.-EU trade with the prospect of severe tariffs.

![]() Oil prices hit six-month highs (Brent ~$71.70, WTI ~$66.50) as President Trump signals an imminent strike on Iran’s nuclear program.

Oil prices hit six-month highs (Brent ~$71.70, WTI ~$66.50) as President Trump signals an imminent strike on Iran’s nuclear program.

![]() Investors sold “AI losers” vulnerable to disruption and worried about hyperscalers’ $740 billion capital expenditure in 2026 which could turn Mag 7 free cash flow to zero or negative.

Investors sold “AI losers” vulnerable to disruption and worried about hyperscalers’ $740 billion capital expenditure in 2026 which could turn Mag 7 free cash flow to zero or negative.

![]() Entrenched inflation (tariff and service) and shaky labor strength have locked the Fed in hold mode.

Entrenched inflation (tariff and service) and shaky labor strength have locked the Fed in hold mode.

![]() Incoming Fed Chair Warsh’s ” lower rates + smaller balance sheet” policy combo, safe-haven buying ignited by geopolitical tensions with Iran and strong central bank accumulation momentum uphold the bull thesis for gold.

Incoming Fed Chair Warsh’s ” lower rates + smaller balance sheet” policy combo, safe-haven buying ignited by geopolitical tensions with Iran and strong central bank accumulation momentum uphold the bull thesis for gold.

![]() With Iran rejecting red lines and U.S. strikes on the horizon, Brent could test $80–85 or higher, echoing last year’s conflict spike.

With Iran rejecting red lines and U.S. strikes on the horizon, Brent could test $80–85 or higher, echoing last year’s conflict spike.

![]() By striking down broad tariffs, the Supreme Court has undermined tariff revenue and opened the door for refunds, delivering lower inflation and stronger growth while simultaneously straining the federal deficit.

By striking down broad tariffs, the Supreme Court has undermined tariff revenue and opened the door for refunds, delivering lower inflation and stronger growth while simultaneously straining the federal deficit.

![]() The Hang Seng Index hovered between 26,000 and 27000, with daily turnover of HK$250-350 billion, experiencing a significant “AI stock heat,” characterized by a strong rally in AI application & model stocks, robotics companies, storage chip and semiconductor stocks.

The Hang Seng Index hovered between 26,000 and 27000, with daily turnover of HK$250-350 billion, experiencing a significant “AI stock heat,” characterized by a strong rally in AI application & model stocks, robotics companies, storage chip and semiconductor stocks.