Highlights

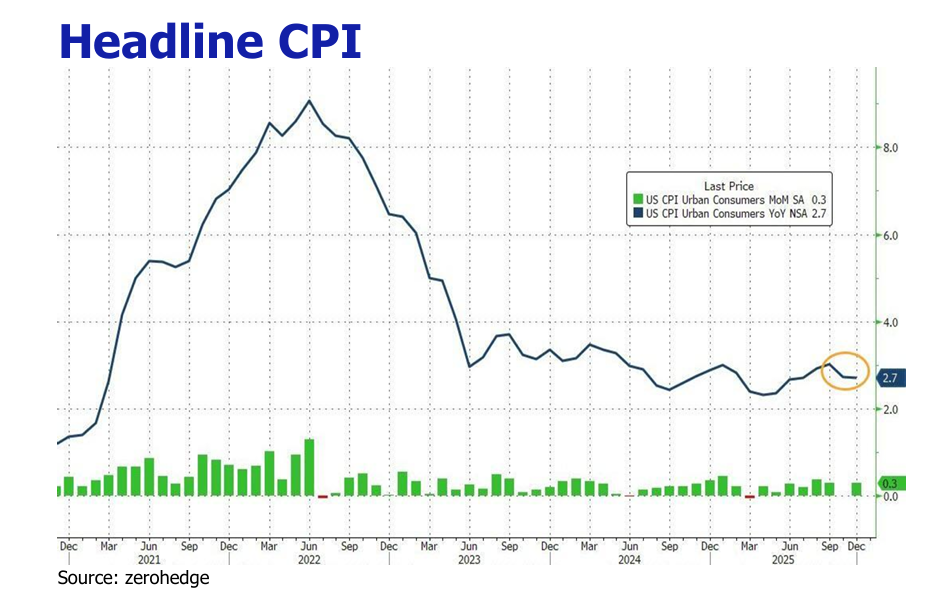

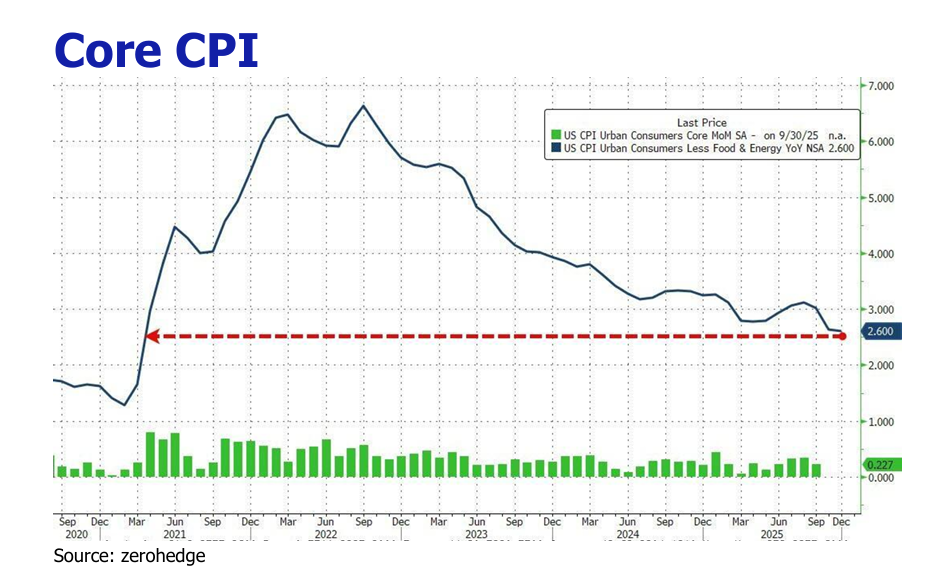

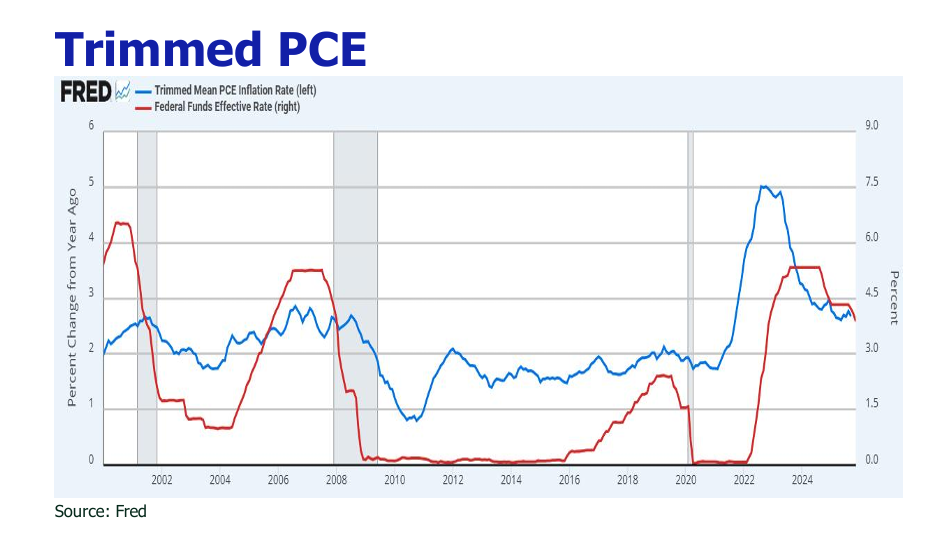

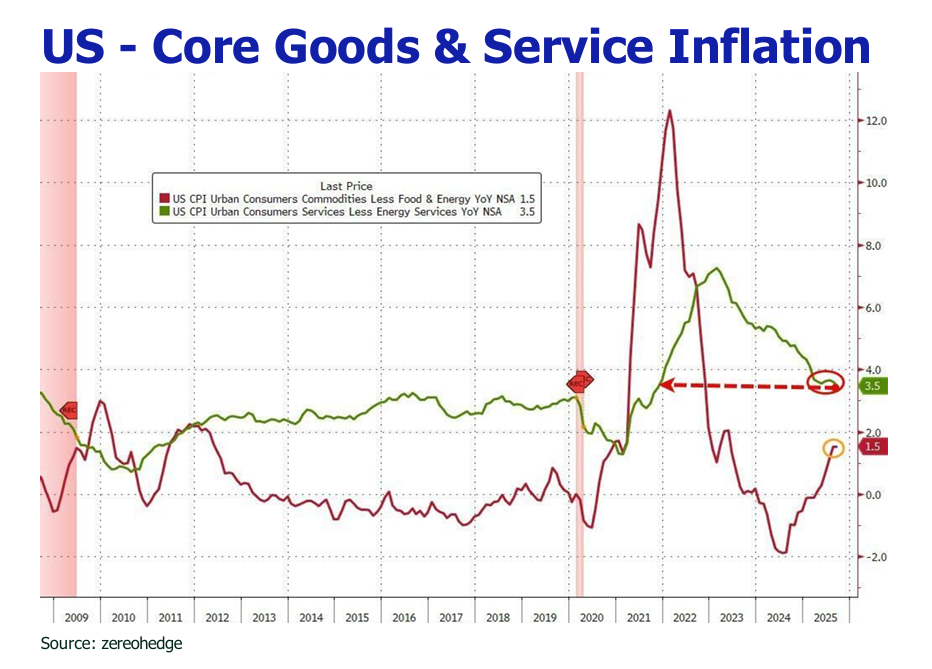

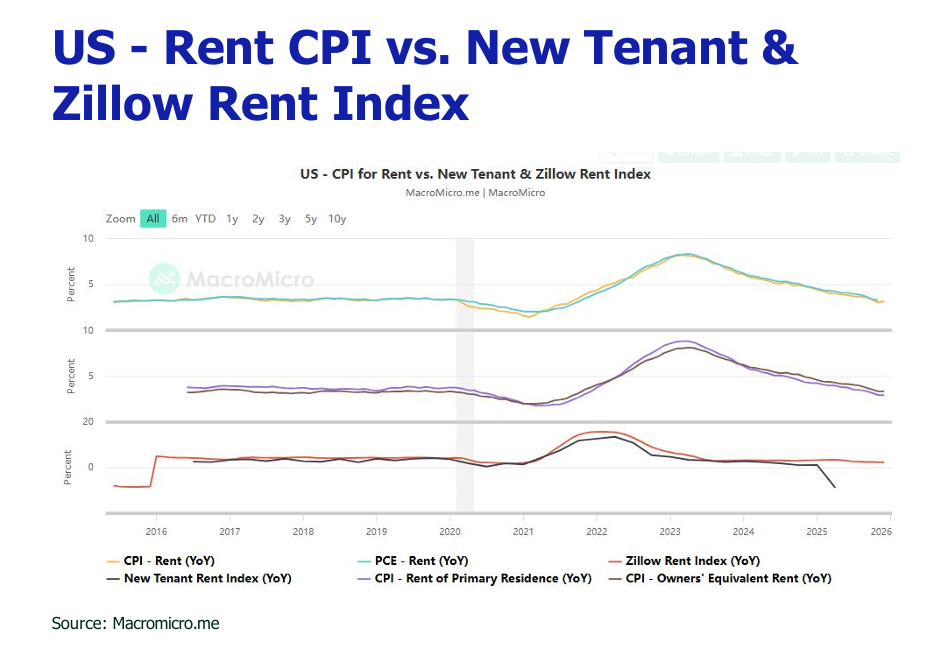

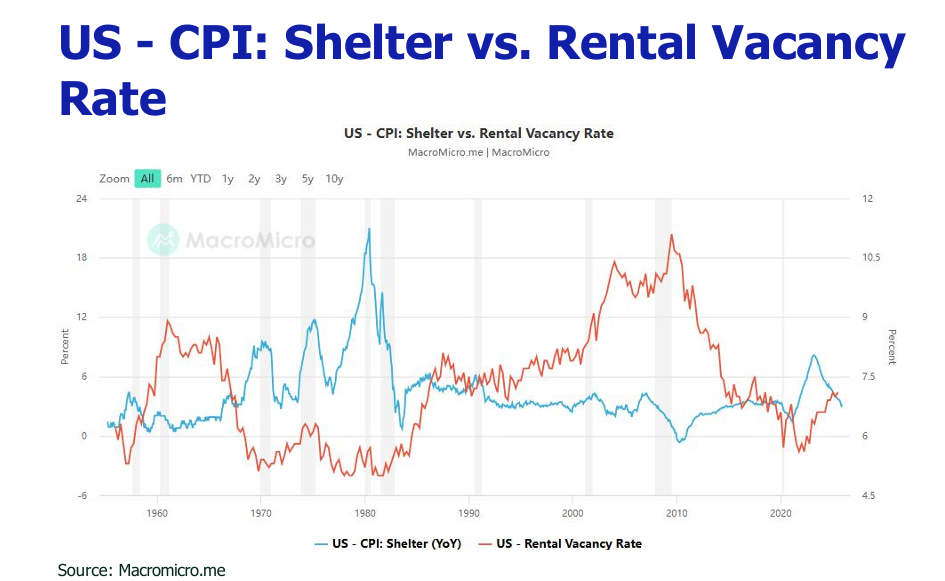

![]() US December CPI remained stagnant at 2.7% year-over-year as rising food and shelter costs offset falling energy prices, with core inflation holding steady at 2.6% despite mixed sectoral trends like holiday-driven airfare spikes and declining used vehicle prices.

US December CPI remained stagnant at 2.7% year-over-year as rising food and shelter costs offset falling energy prices, with core inflation holding steady at 2.6% despite mixed sectoral trends like holiday-driven airfare spikes and declining used vehicle prices.

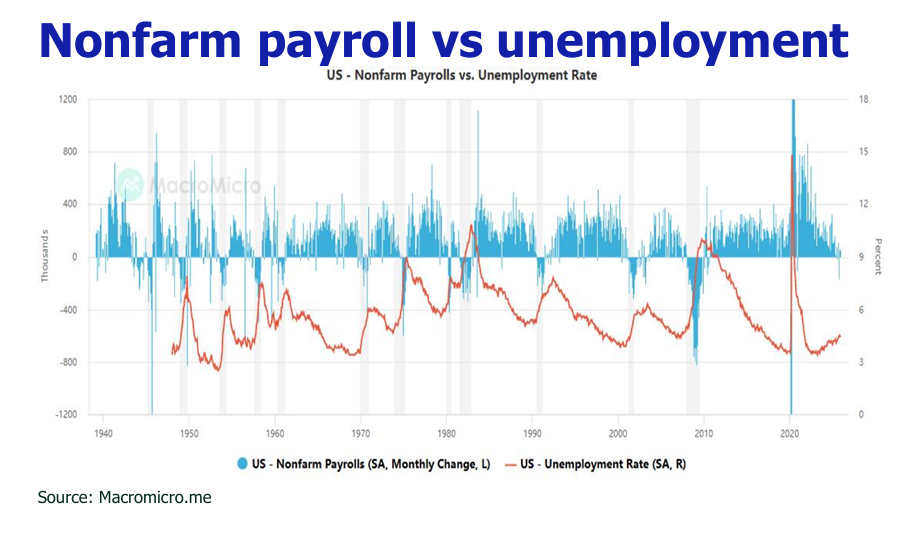

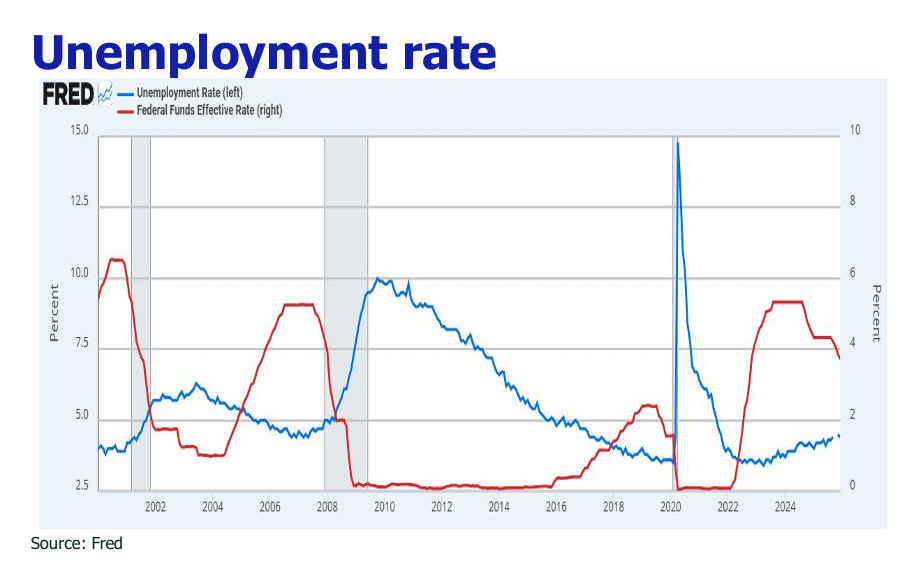

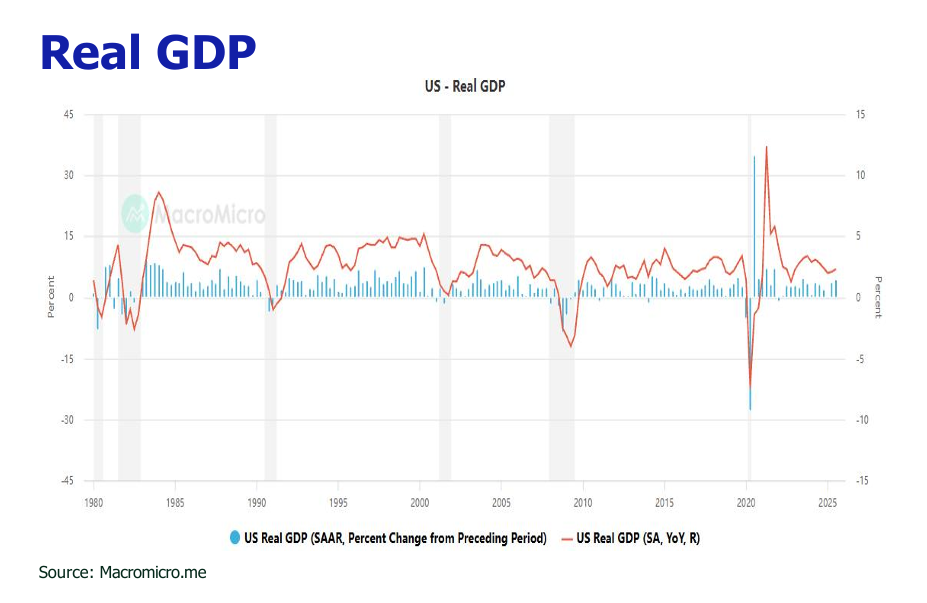

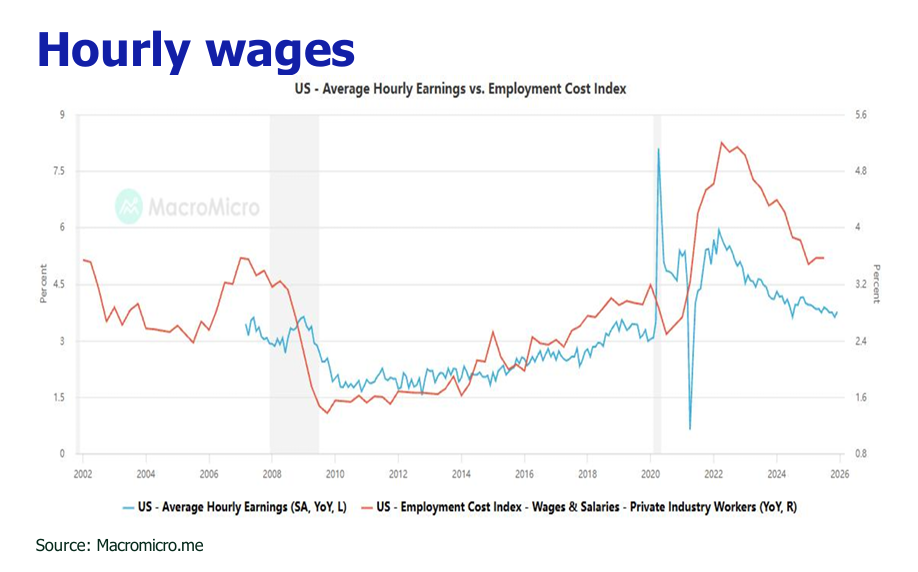

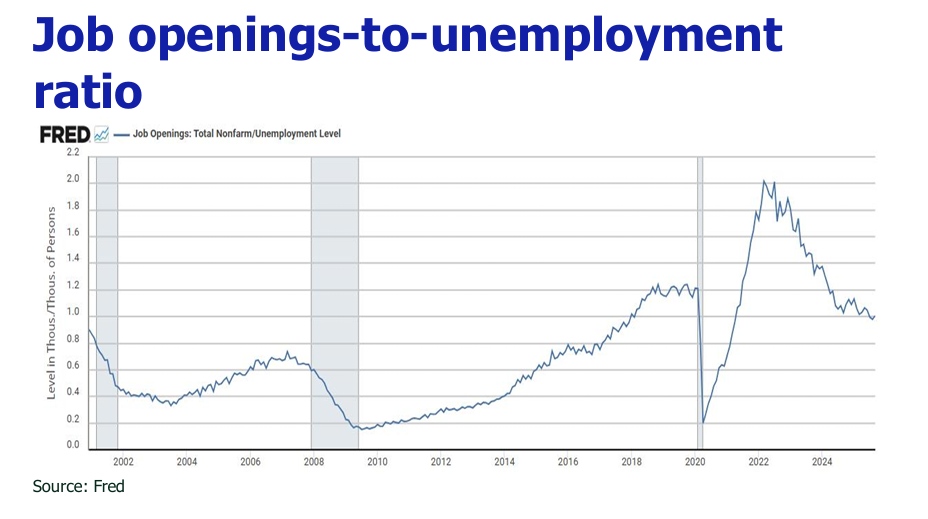

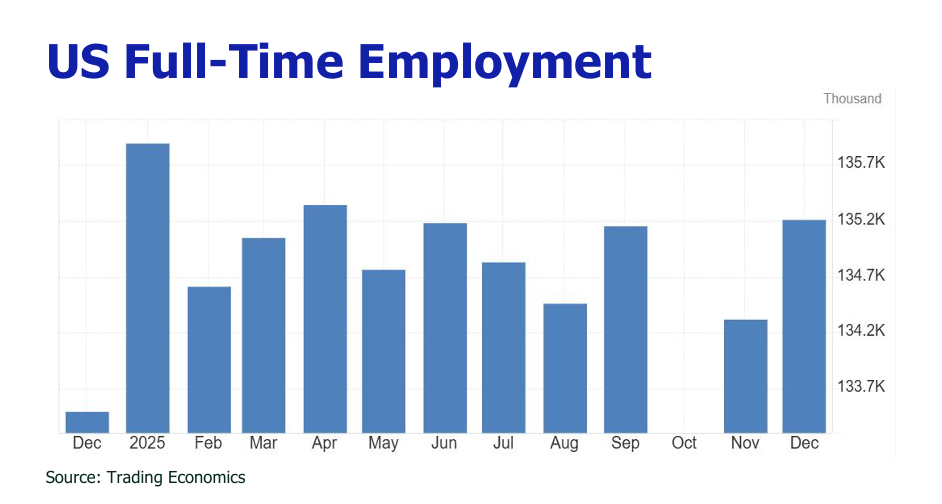

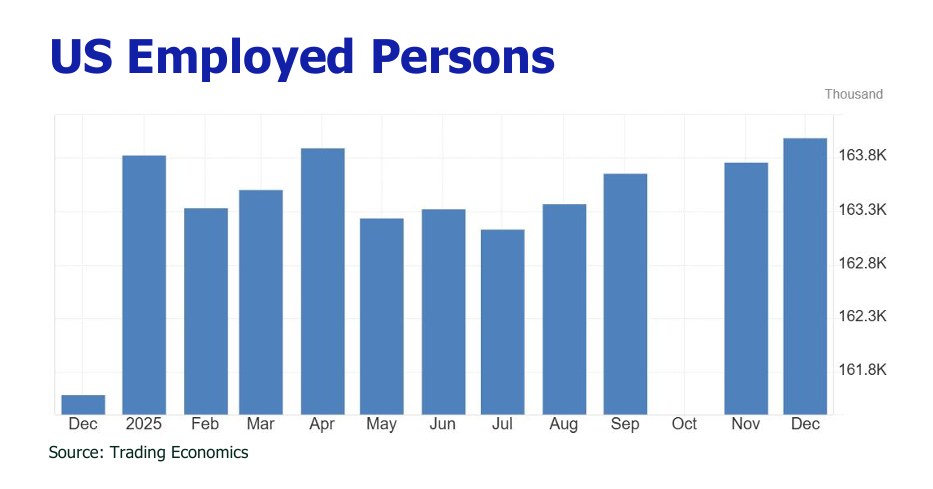

![]() The US labor market exhibited mixed dynamics with the weakest annual job growth since 2020 (adding only 50,000 jobs in December), yet the unemployment rate dipped to 4.4% as service sectors added positions while manufacturing, construction, and retail cut jobs.

The US labor market exhibited mixed dynamics with the weakest annual job growth since 2020 (adding only 50,000 jobs in December), yet the unemployment rate dipped to 4.4% as service sectors added positions while manufacturing, construction, and retail cut jobs.

![]() The Greenland acquisition hiccup has ignited a conflict that menaces U.S.-EU trade with the prospect of severe tariffs.

The Greenland acquisition hiccup has ignited a conflict that menaces U.S.-EU trade with the prospect of severe tariffs.

![]() Oilprices in January 2026 experienced sharp but temporary volatility, briefly pushing Brent above $66/bbl due to geopolitical instability in Venezuela and Iran, before retreating to the mid-$50s and low-$60s as risks de-escalated and the market refocused on global oversupply.

Oilprices in January 2026 experienced sharp but temporary volatility, briefly pushing Brent above $66/bbl due to geopolitical instability in Venezuela and Iran, before retreating to the mid-$50s and low-$60s as risks de-escalated and the market refocused on global oversupply.

![]() Asurgein Japan’s government bond yields, driven by fiscal stimulus fears, briefly roiled global markets, lifting U.S. yields and pressuring stocks.

Asurgein Japan’s government bond yields, driven by fiscal stimulus fears, briefly roiled global markets, lifting U.S. yields and pressuring stocks.

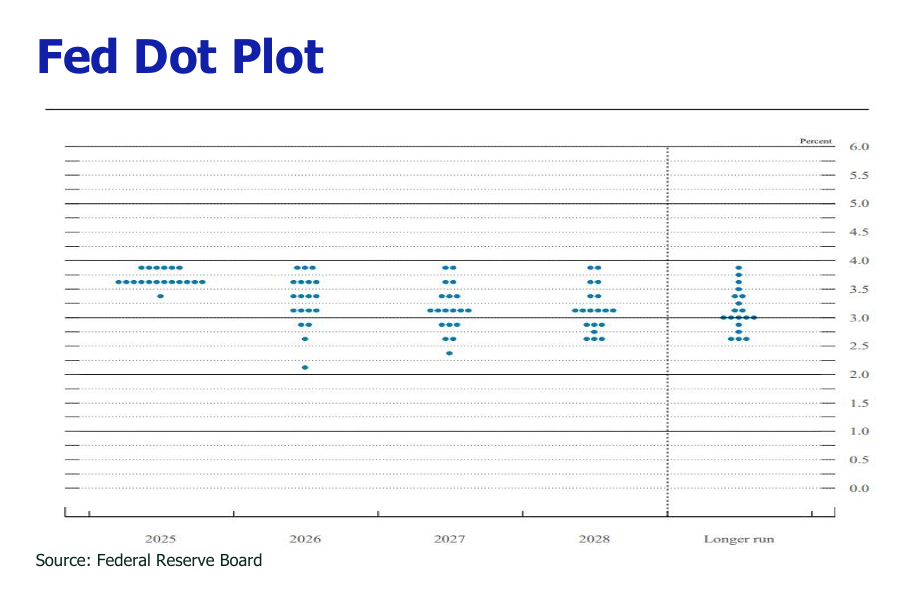

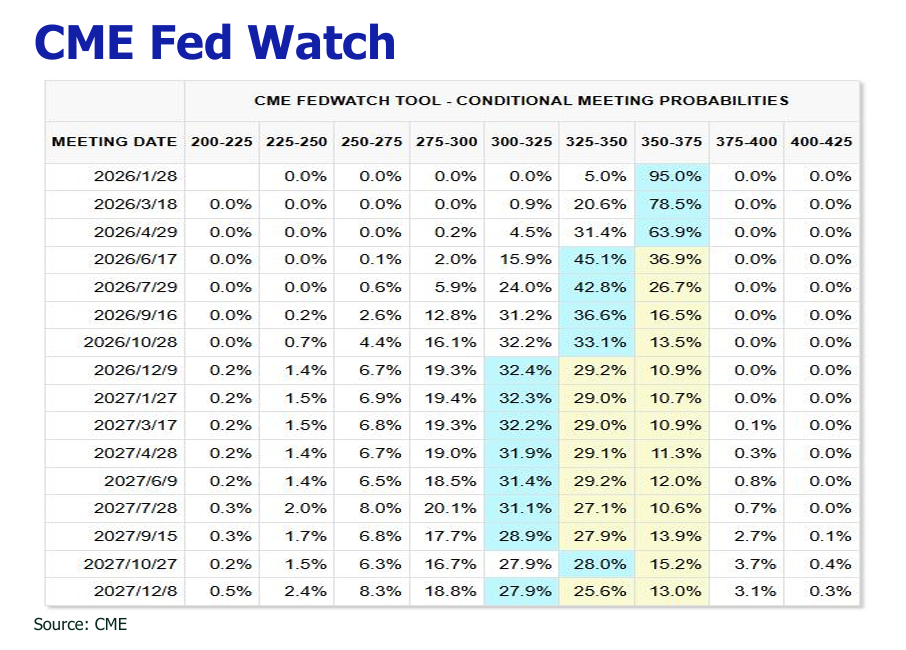

![]() The Federal Reserve is expected to halt rate cuts in Q1 2026, prioritizing inflation control over labor market cooling, as it waits for the full impact of new tariffs to pass through to consumer prices and for clearer evidence of core inflation sustainably falling toward its 2% target.

The Federal Reserve is expected to halt rate cuts in Q1 2026, prioritizing inflation control over labor market cooling, as it waits for the full impact of new tariffs to pass through to consumer prices and for clearer evidence of core inflation sustainably falling toward its 2% target.

![]() The outlook for gold in 2026 remains strongly bullish, underpinned by persistent structural drivers including sustained central bank buying, low real yields, high geopolitical hedging demand, and substantial room for increased allocations in private and institutional portfolios.

The outlook for gold in 2026 remains strongly bullish, underpinned by persistent structural drivers including sustained central bank buying, low real yields, high geopolitical hedging demand, and substantial room for increased allocations in private and institutional portfolios.

![]() The USD is expected to depreciate 4–8% in 2026, driven by anticipated Fed rate cuts that erode its yield advantage.

The USD is expected to depreciate 4–8% in 2026, driven by anticipated Fed rate cuts that erode its yield advantage.

![]() The Hang Seng Index topped out 26,000, with daily turnover surging to above HK$250 billion, driven by PBoC’s monetary easing (0.25% lending rate cut, further RRR and rate cuts signals), sustained southbound capital inflows through Stock Connect, and rate cut positive (Dec and more in 2026) from the U.S..

The Hang Seng Index topped out 26,000, with daily turnover surging to above HK$250 billion, driven by PBoC’s monetary easing (0.25% lending rate cut, further RRR and rate cuts signals), sustained southbound capital inflows through Stock Connect, and rate cut positive (Dec and more in 2026) from the U.S..