Highlights

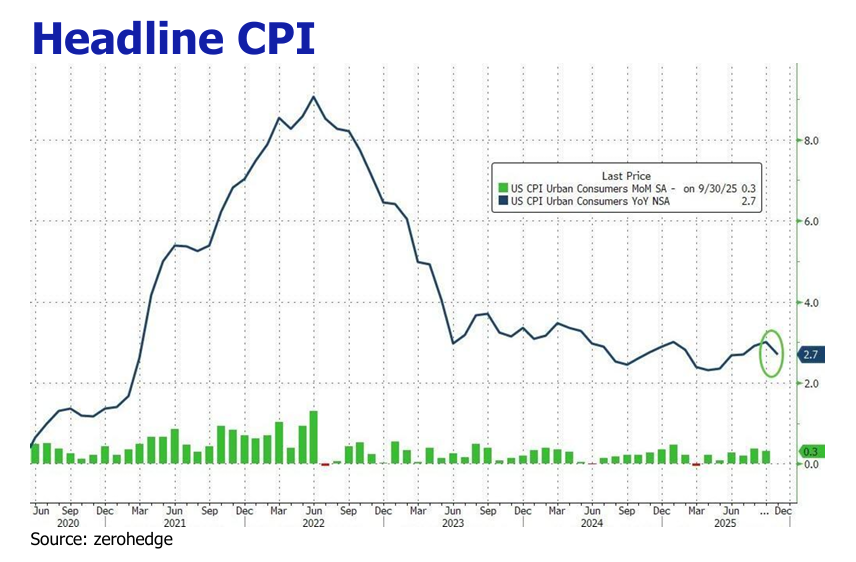

![]() November CPI eased to 2.7%YoY yet distorted by Black Friday discounts and October owners’ equivalent rent (OER) adjustment.

November CPI eased to 2.7%YoY yet distorted by Black Friday discounts and October owners’ equivalent rent (OER) adjustment.

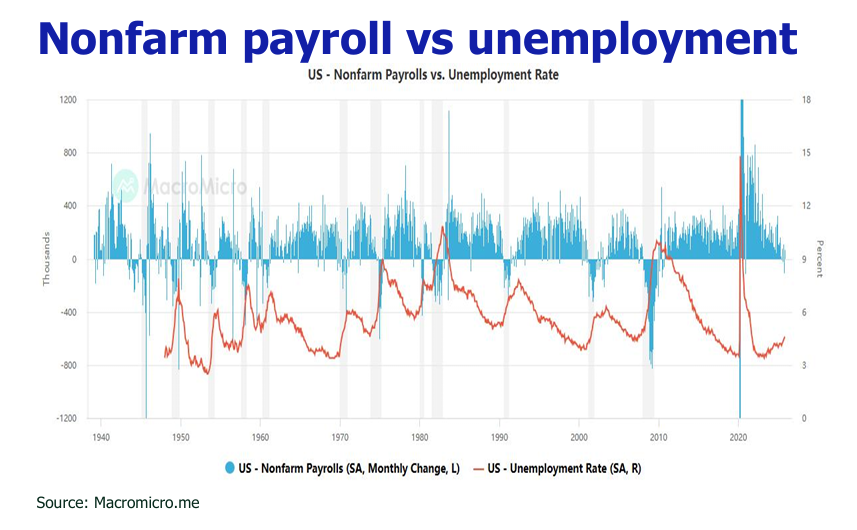

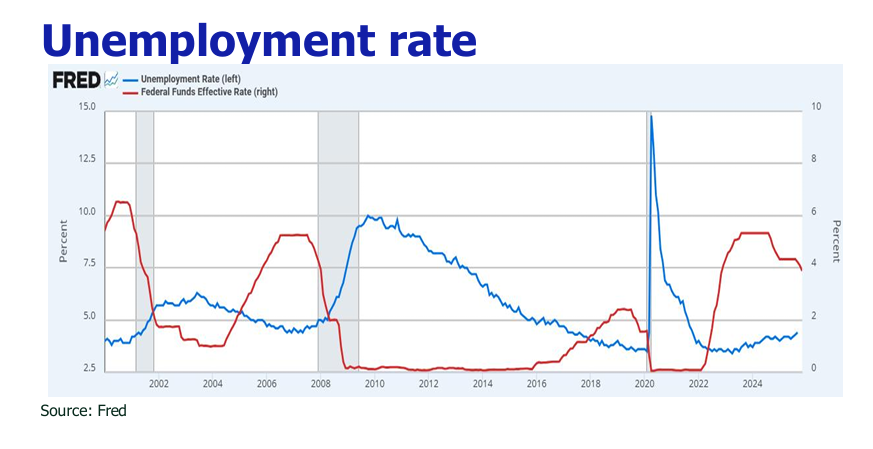

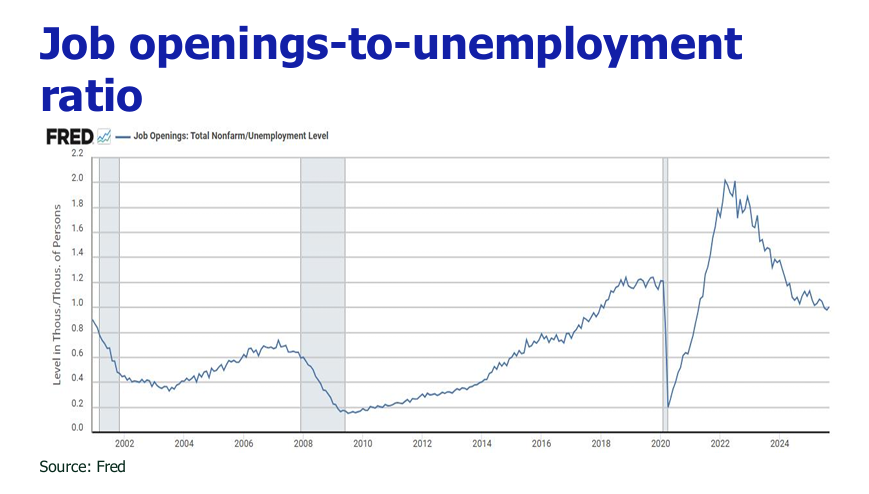

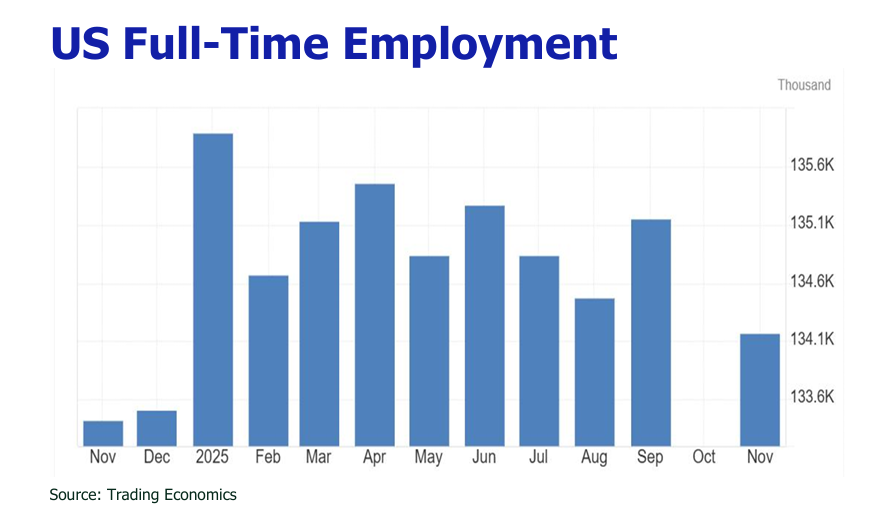

![]() Jitter on sharp October and September downward nonfarm payroll adjustment and higher unemployment rate belie euphoria on the better-than-expected November nonfarm payroll growth.

Jitter on sharp October and September downward nonfarm payroll adjustment and higher unemployment rate belie euphoria on the better-than-expected November nonfarm payroll growth.

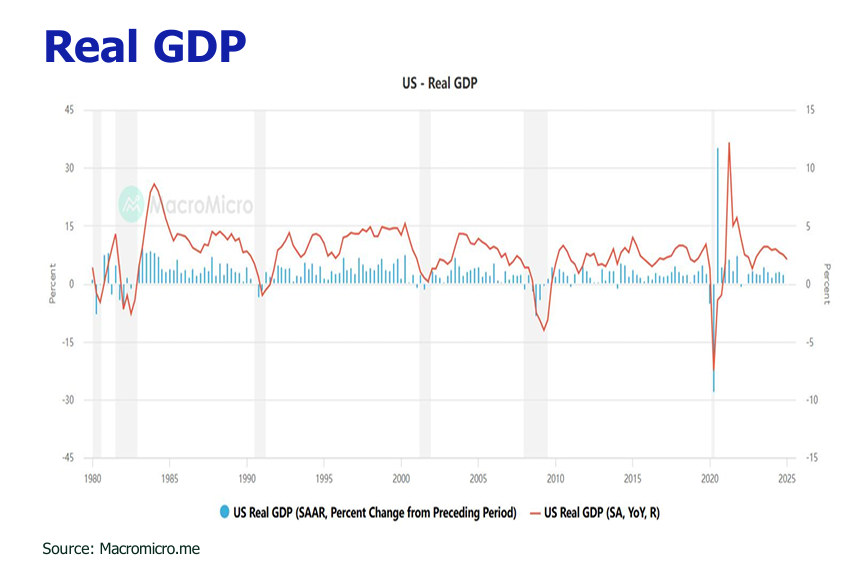

![]() The Genesis Mission is instituted to pull off a new epoch of American-led technological and economic prosperity leveraging AI investment, holding the potential to inject an additional $1 to $2 trillion into U.S. GDP by 2035.

The Genesis Mission is instituted to pull off a new epoch of American-led technological and economic prosperity leveraging AI investment, holding the potential to inject an additional $1 to $2 trillion into U.S. GDP by 2035.

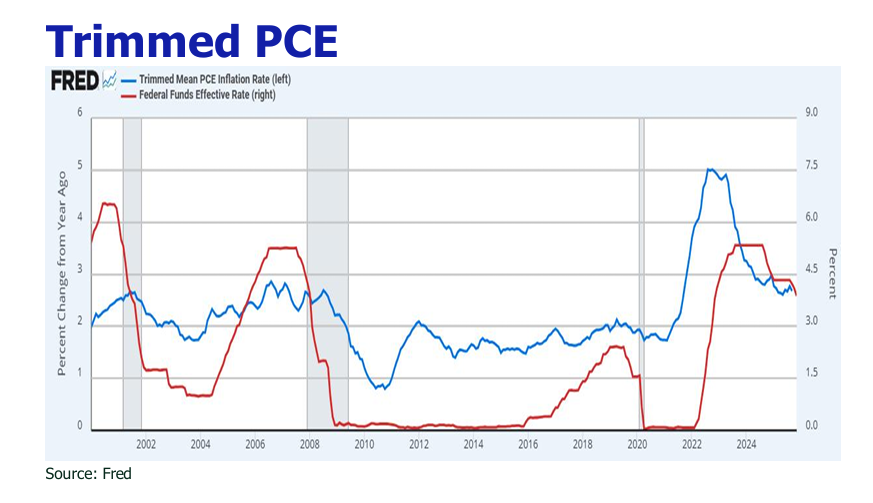

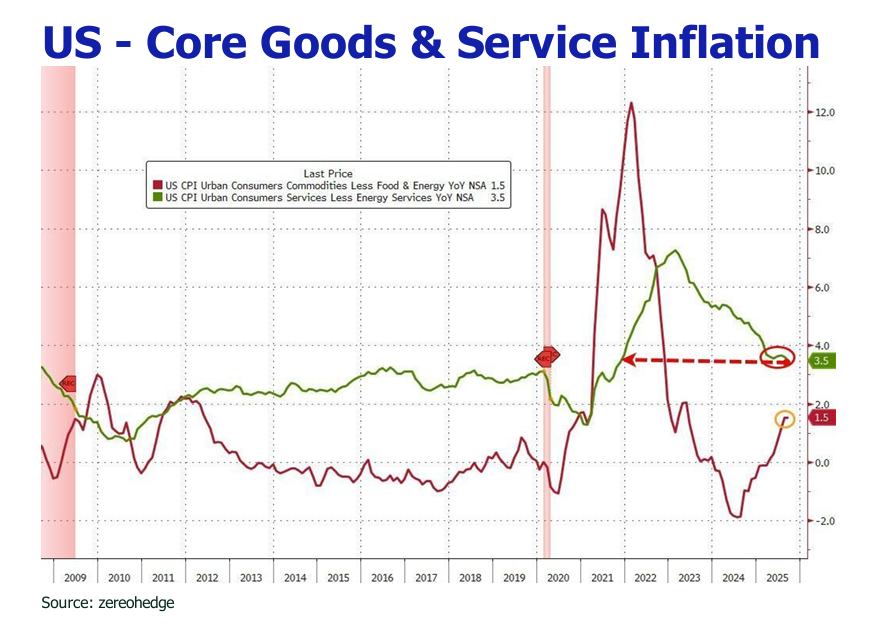

![]() Although initial tariff impacts have been muted by preemptive corporate inventory stockpiling and promotional pricing, the risk of a resurgent price impulse remains.

Although initial tariff impacts have been muted by preemptive corporate inventory stockpiling and promotional pricing, the risk of a resurgent price impulse remains.

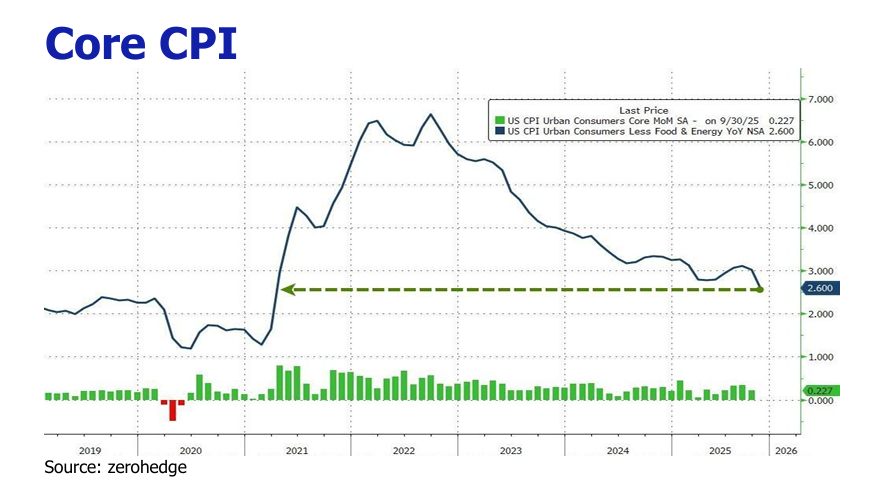

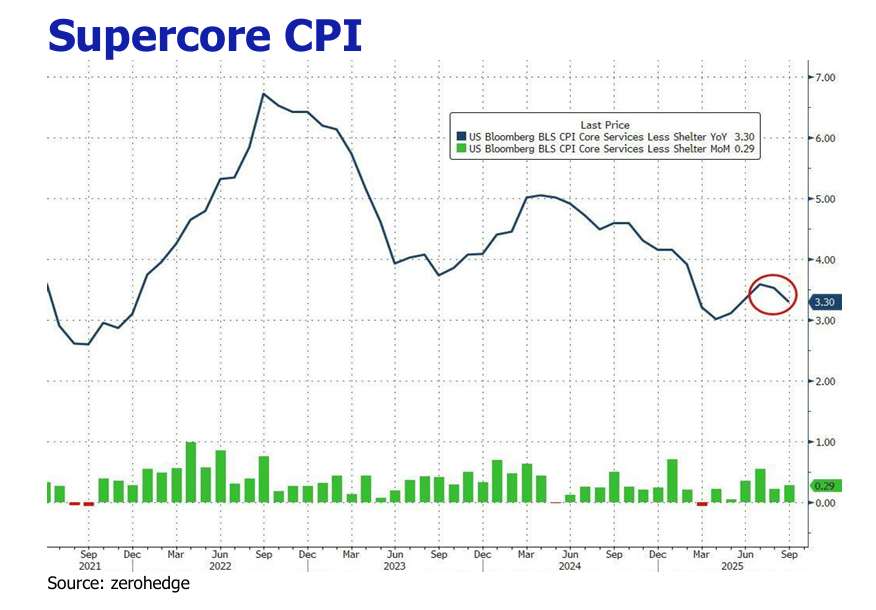

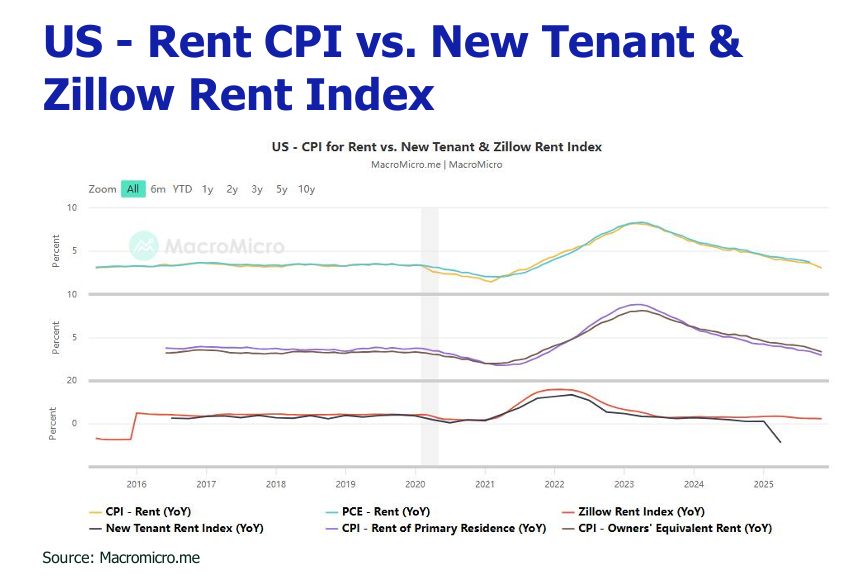

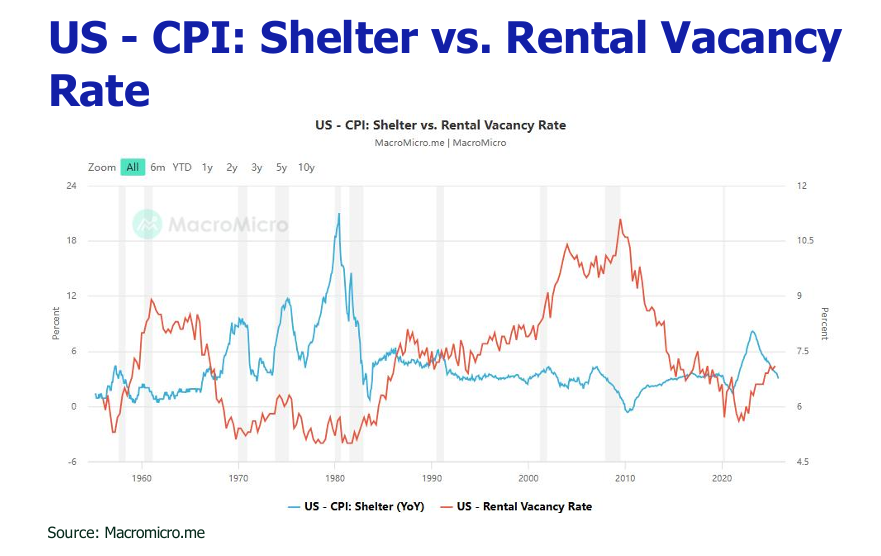

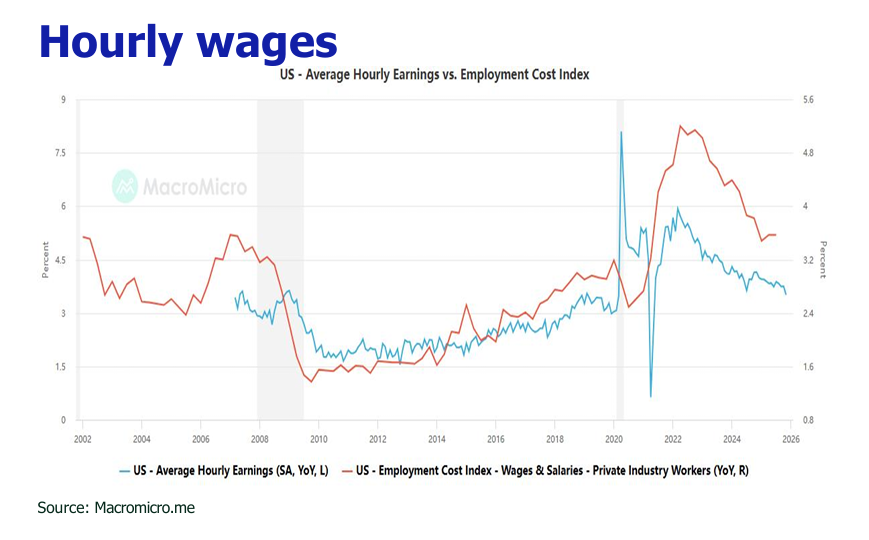

![]() Aclearly easing labor market is tempering wage growth, while a confluence of lagging lease pipelines, rising rental listings, and increased new construction is poised to materially decelerate shelter inflation in 2026.

Aclearly easing labor market is tempering wage growth, while a confluence of lagging lease pipelines, rising rental listings, and increased new construction is poised to materially decelerate shelter inflation in 2026.

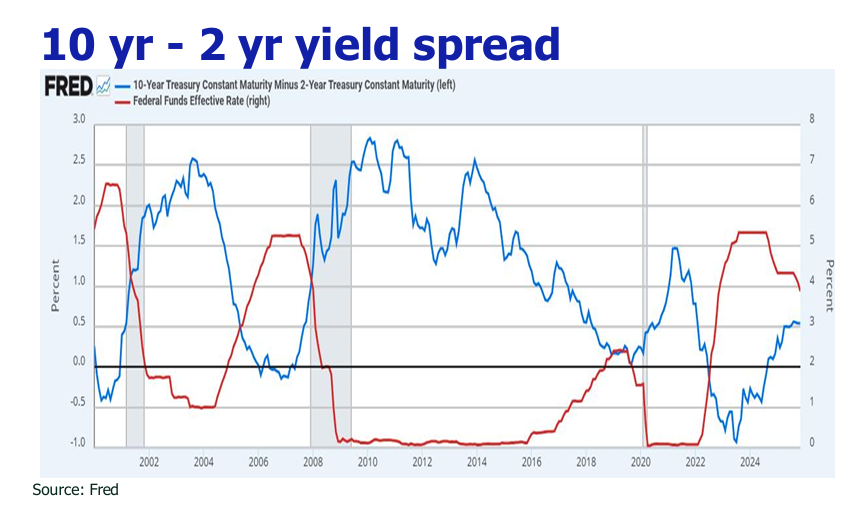

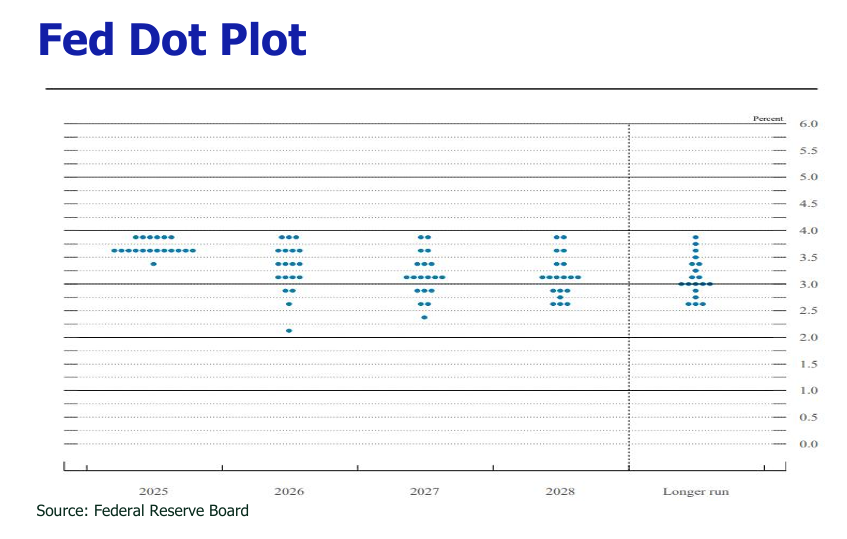

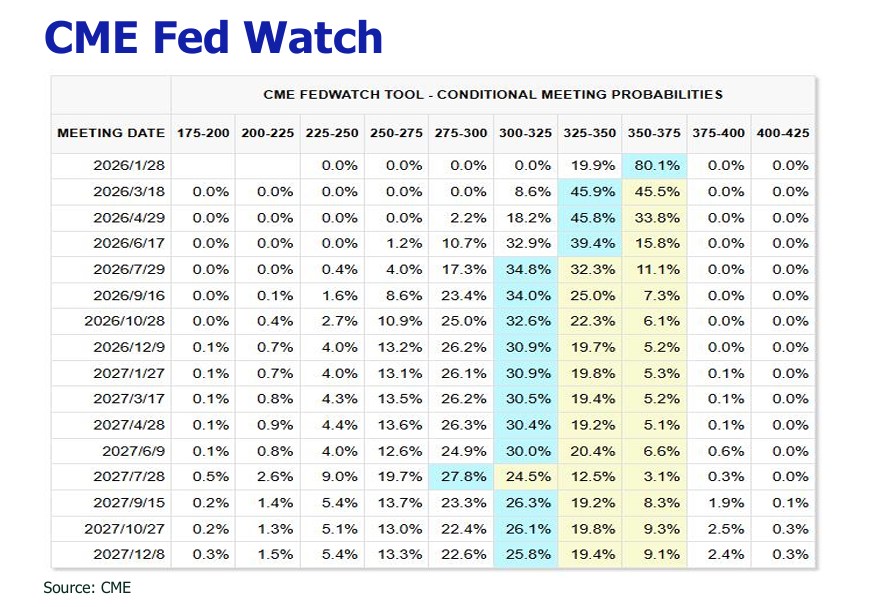

![]() Against this backdrop of muddied inflation signals and mounting labor market slack, the Federal Reserve is expected to continue its normalization path in 2026.

Against this backdrop of muddied inflation signals and mounting labor market slack, the Federal Reserve is expected to continue its normalization path in 2026.

![]() Alabor market facing multifaceted headwinds from continued government layoffs (projected 50k-100k), AI-driven role displacement, and tariff-affected sectors.

Alabor market facing multifaceted headwinds from continued government layoffs (projected 50k-100k), AI-driven role displacement, and tariff-affected sectors.

![]() Ourbaseline forecast anticipates one further 25bp cut in 2026, and the ultimate pace will be a function of confirmed inflation moderation and, critically, the doctrinal leanings of the next Fed Chair.

Ourbaseline forecast anticipates one further 25bp cut in 2026, and the ultimate pace will be a function of confirmed inflation moderation and, critically, the doctrinal leanings of the next Fed Chair.

![]() The Hang Seng Index remained capped below 26,000 throughout much of the period, with daily turnover ranging between HK$160–240 billion.

The Hang Seng Index remained capped below 26,000 throughout much of the period, with daily turnover ranging between HK$160–240 billion.

![]() The tailwind from the Federal Reserve’s mid-December 25-basis-point rate cut was largely offset by persistent liquidity concerns among Hong Kong and mainland developers, compounded by November’s low single-digit growth in China retail sales.

The tailwind from the Federal Reserve’s mid-December 25-basis-point rate cut was largely offset by persistent liquidity concerns among Hong Kong and mainland developers, compounded by November’s low single-digit growth in China retail sales.