Highlights

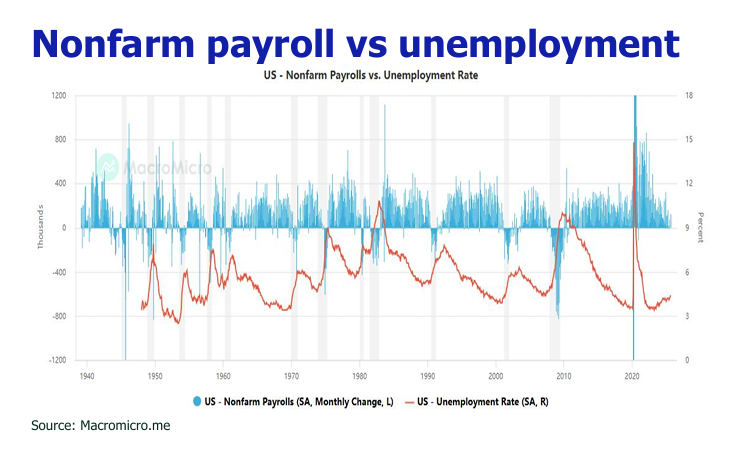

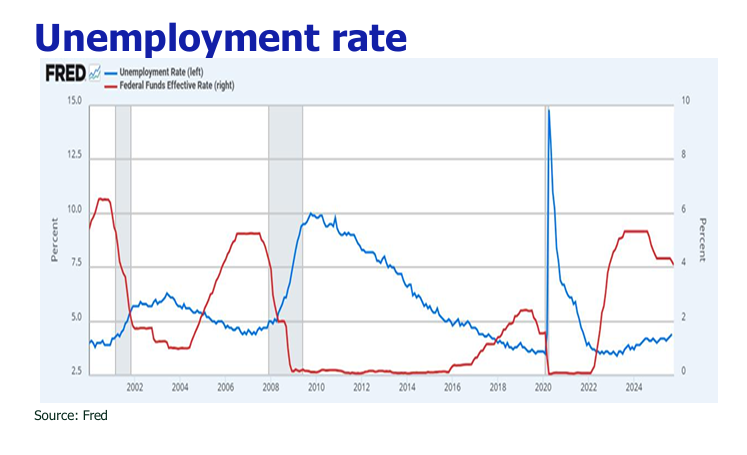

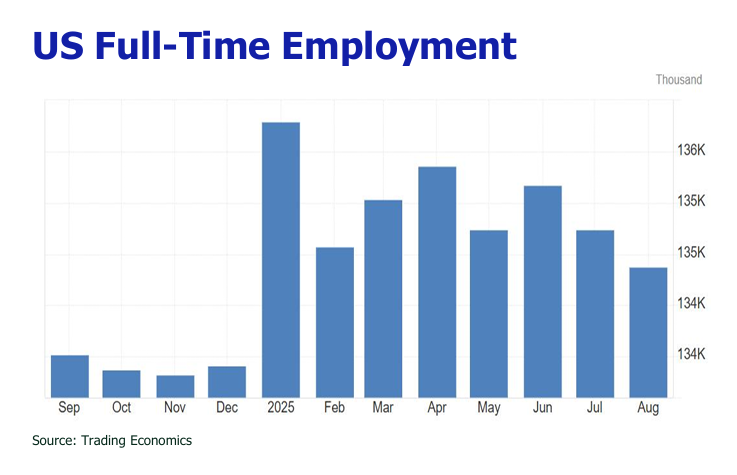

![]() A significant wave of layoffs, led by tech sector restructuring and spreading to other industries, signals a rapidly deteriorating US labor market yet September nonfarm payrolls rose by 119,000.

A significant wave of layoffs, led by tech sector restructuring and spreading to other industries, signals a rapidly deteriorating US labor market yet September nonfarm payrolls rose by 119,000.

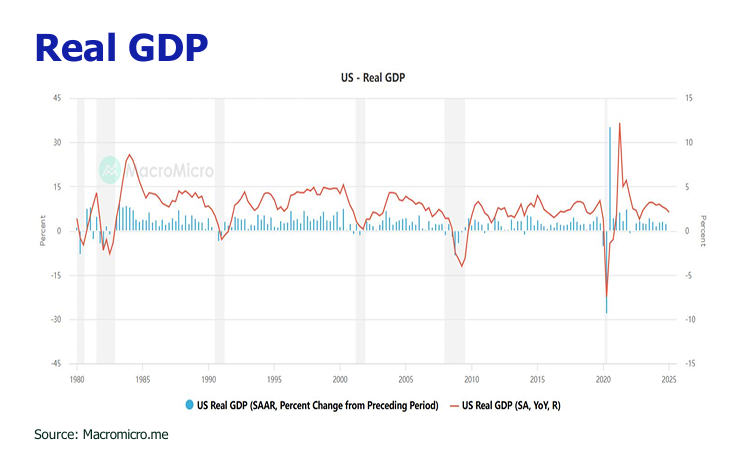

![]() The 43-day U.S. government shutdown (Oct 1–Nov 12/13, 2025) acted as a massive liquidity drain, pressuring stocks (S&P-4%) and crypto (Bitcoin-20%); estimated 1.5pp drag on Q4 GDP, with risk of another shutdown in 2026.

The 43-day U.S. government shutdown (Oct 1–Nov 12/13, 2025) acted as a massive liquidity drain, pressuring stocks (S&P-4%) and crypto (Bitcoin-20%); estimated 1.5pp drag on Q4 GDP, with risk of another shutdown in 2026.

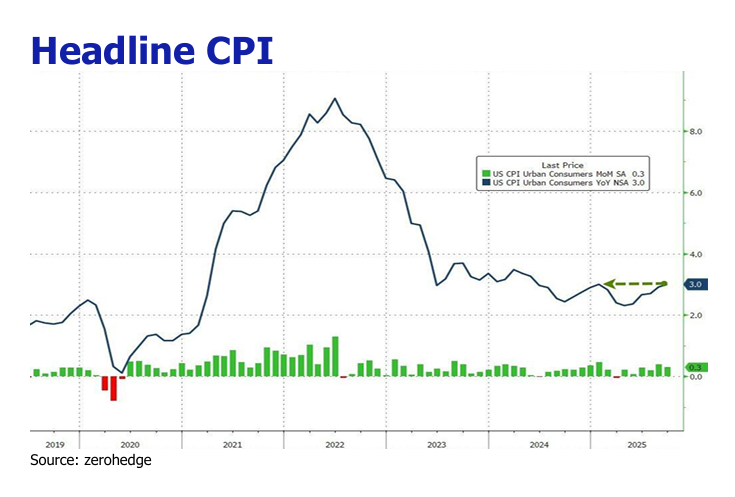

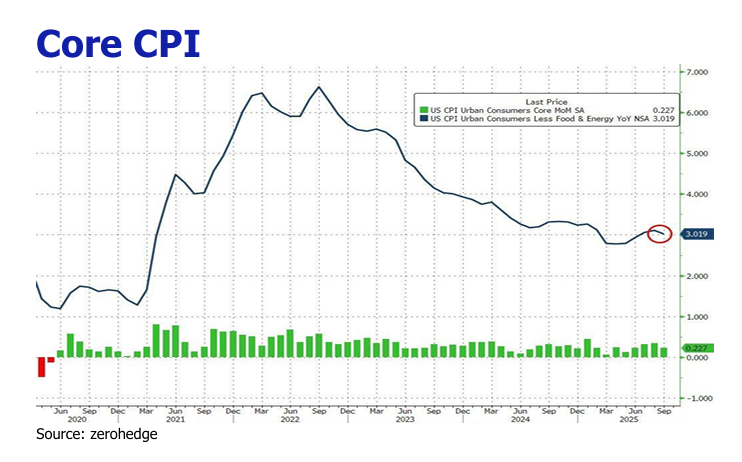

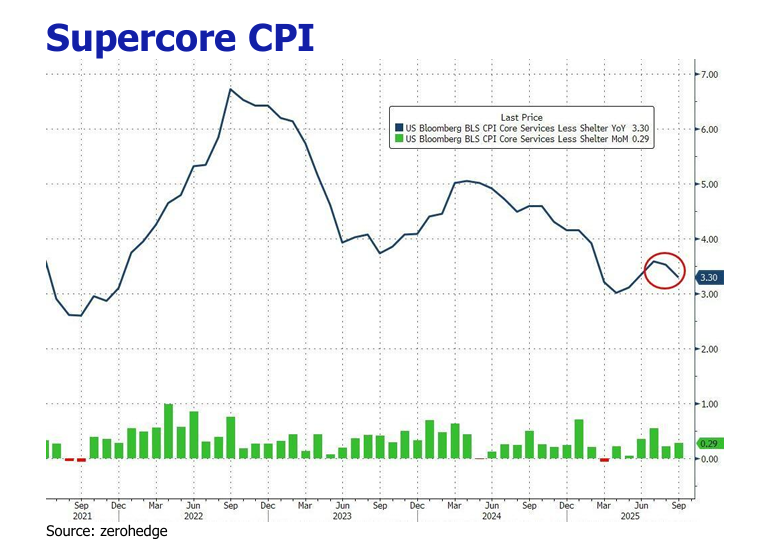

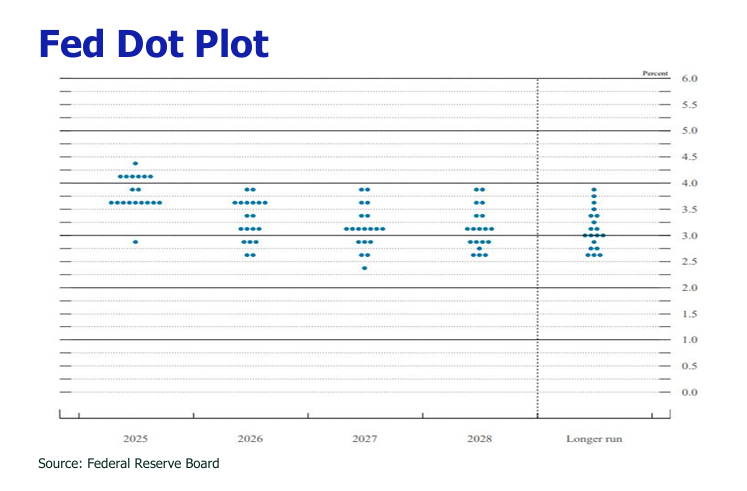

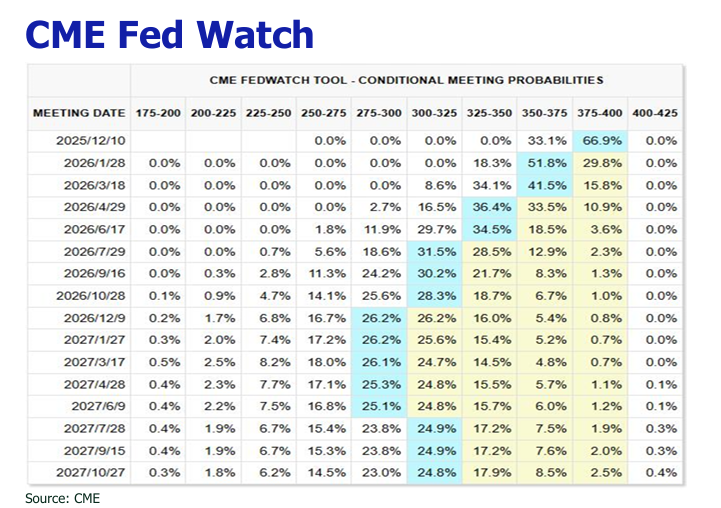

![]() Hawkish Fed rhetoric and a post-shutdown economic data blackout have significantly reduced the likelihood of a December rate cut.

Hawkish Fed rhetoric and a post-shutdown economic data blackout have significantly reduced the likelihood of a December rate cut.

![]() Despite layoffs, delayed easing, and AI doubts, current risk-off is viewed as temporary; a powerful future rally is expected from resilient earnings, AI maturation, and fiscal stimulus convergence.

Despite layoffs, delayed easing, and AI doubts, current risk-off is viewed as temporary; a powerful future rally is expected from resilient earnings, AI maturation, and fiscal stimulus convergence.

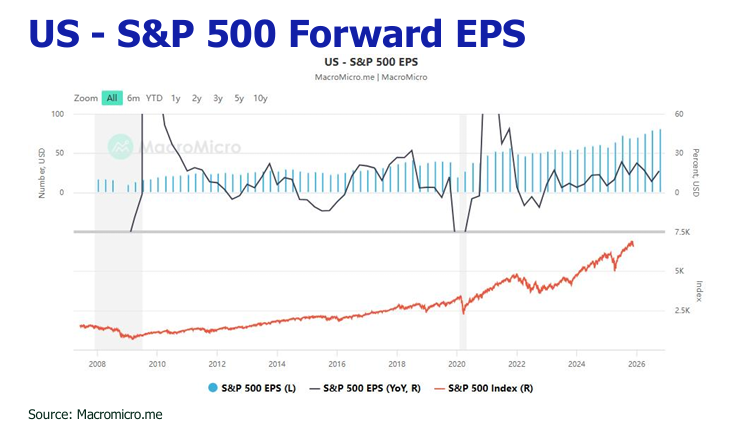

![]() Recent layoffs reflect proactive, strategic restructuring for efficiency and AI integration, which has preserved corporate profitability and margin resilience.

Recent layoffs reflect proactive, strategic restructuring for efficiency and AI integration, which has preserved corporate profitability and margin resilience.

![]() AI ismaturing from a speculative hype cycle into a tangible driver of a “productivity boom,” creating persistent, structural demand for computing infrastructure.

AI ismaturing from a speculative hype cycle into a tangible driver of a “productivity boom,” creating persistent, structural demand for computing infrastructure.

![]() The new fiscal act- OBBBA provides a powerful, pro-cyclical boost through corporate tax incentives and individual benefits, set to lift earnings and fuel consumer spending.

The new fiscal act- OBBBA provides a powerful, pro-cyclical boost through corporate tax incentives and individual benefits, set to lift earnings and fuel consumer spending.

![]() An initial rally spurred by a PBOC RRR cut and a US-China tariff truce was swiftly undone by negative spillover from US markets. As AI concerns and a halted Fed rate cut cycle sparked a Wall Street sell-off, the HSI gave up its gains. The index ended the period slightly down, consolidating around 26,000 amid subdued daily turnover of HK$200-250 billion.

An initial rally spurred by a PBOC RRR cut and a US-China tariff truce was swiftly undone by negative spillover from US markets. As AI concerns and a halted Fed rate cut cycle sparked a Wall Street sell-off, the HSI gave up its gains. The index ended the period slightly down, consolidating around 26,000 amid subdued daily turnover of HK$200-250 billion.