Highlights

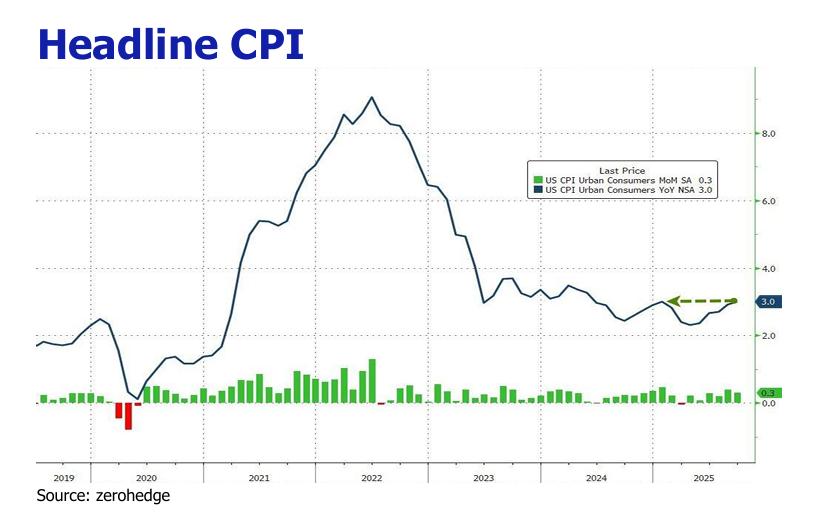

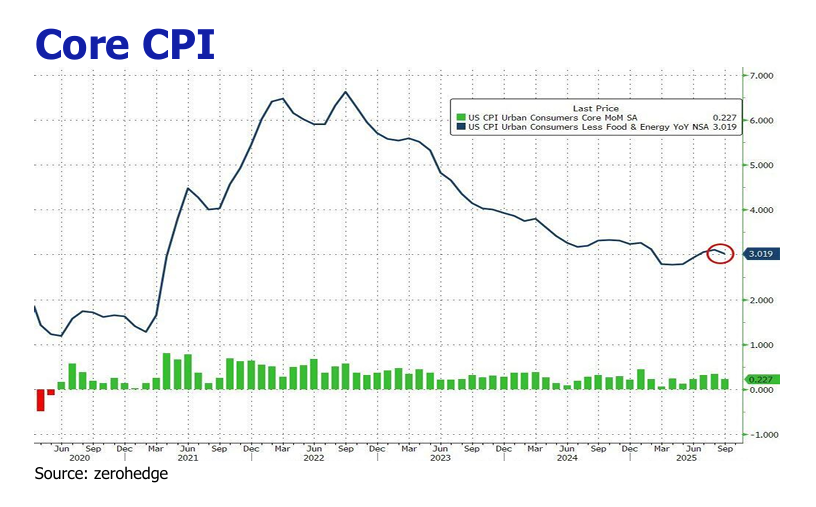

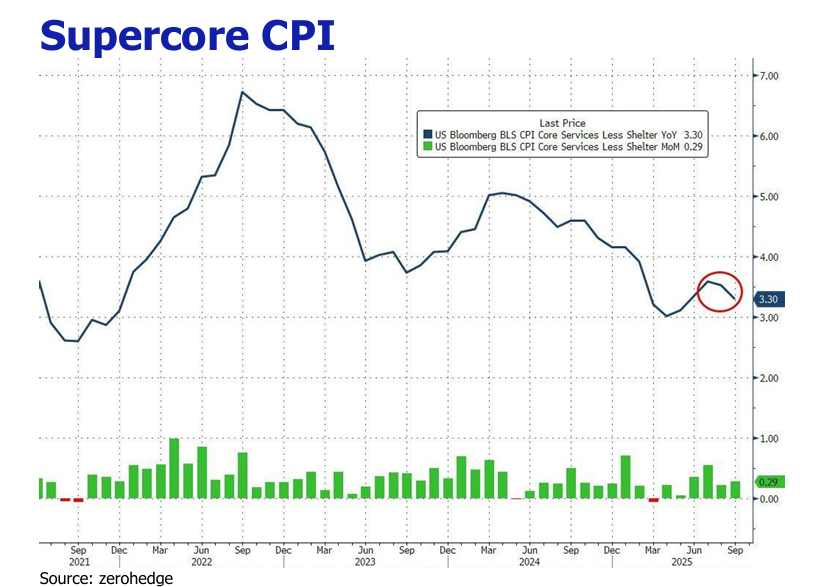

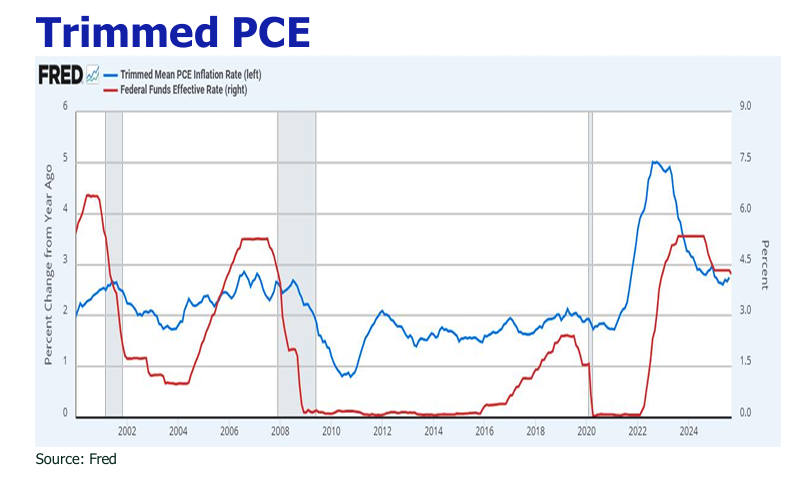

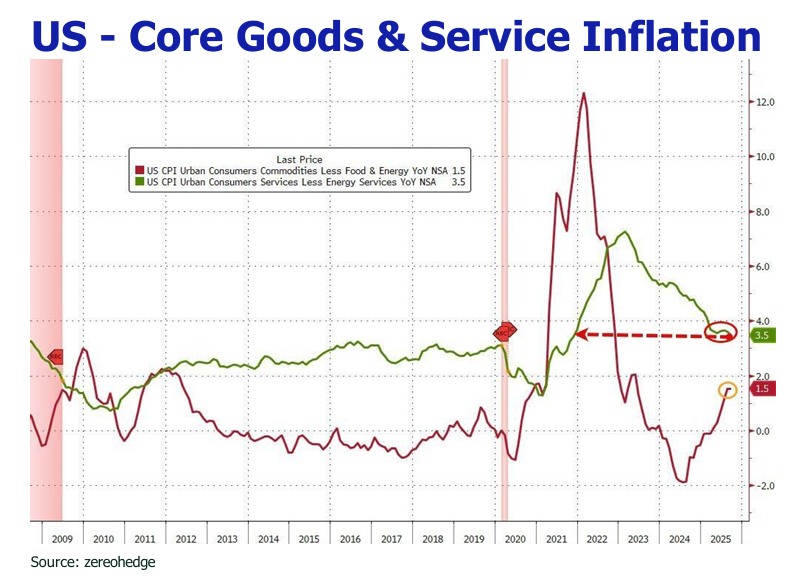

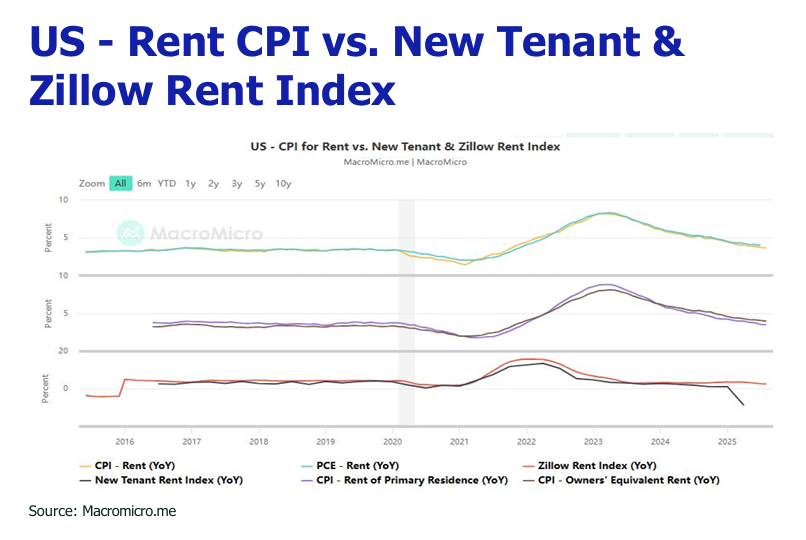

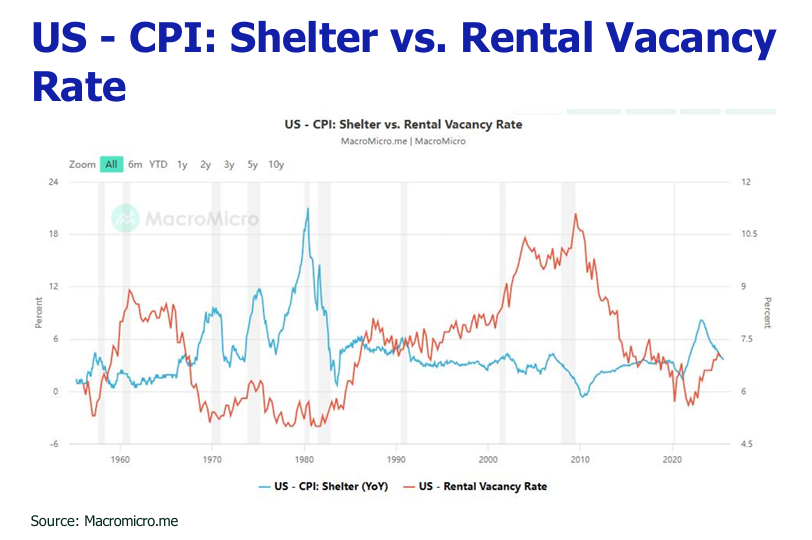

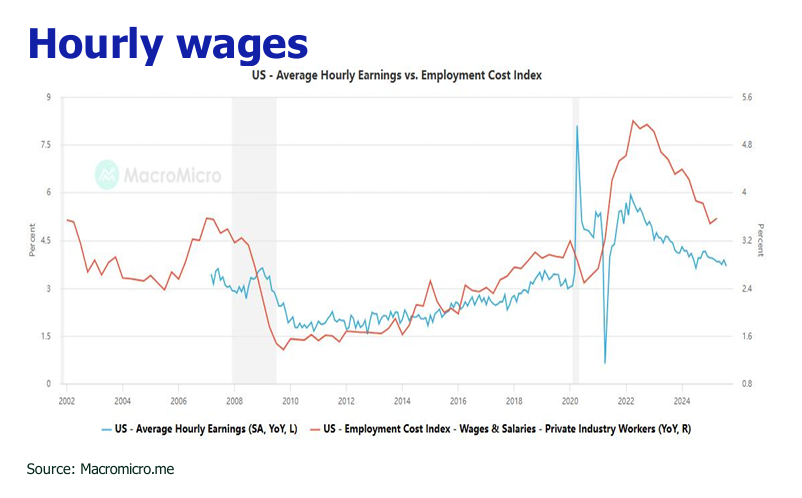

![]() US inflation pressure eased and tariff pass-through remained at the modest level.

US inflation pressure eased and tariff pass-through remained at the modest level.

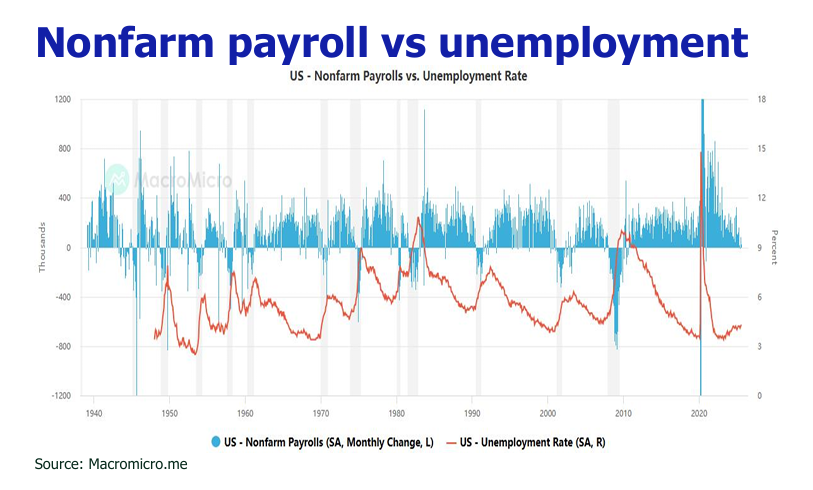

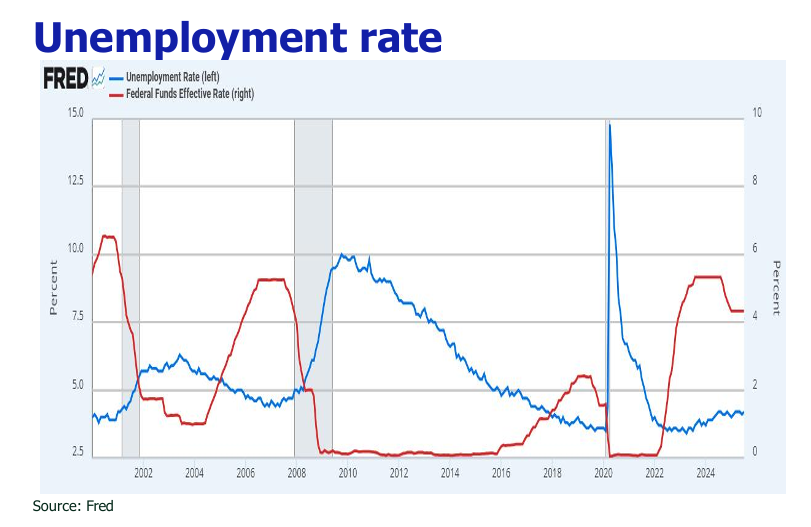

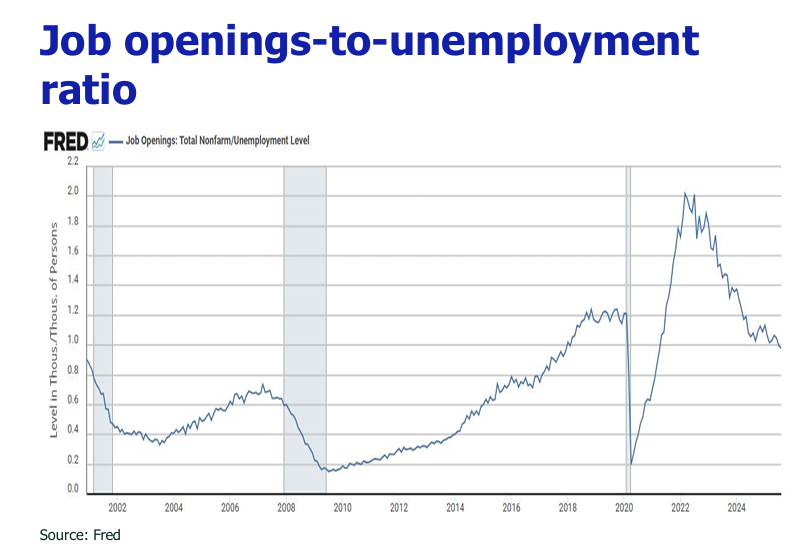

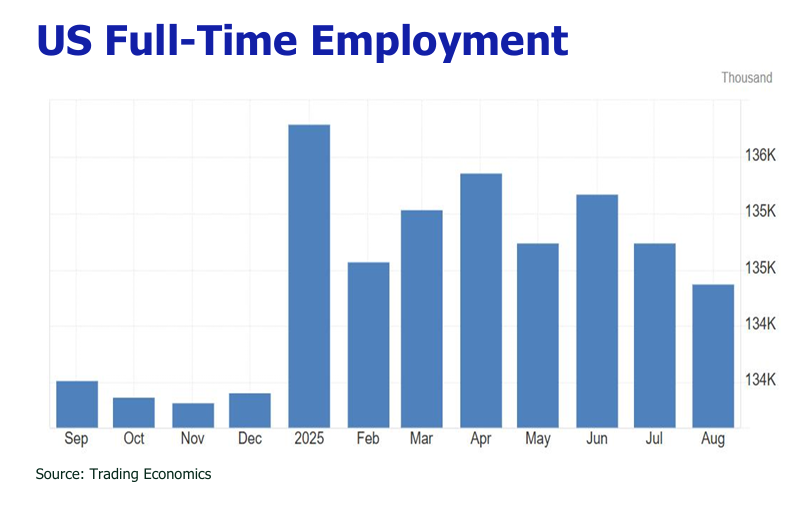

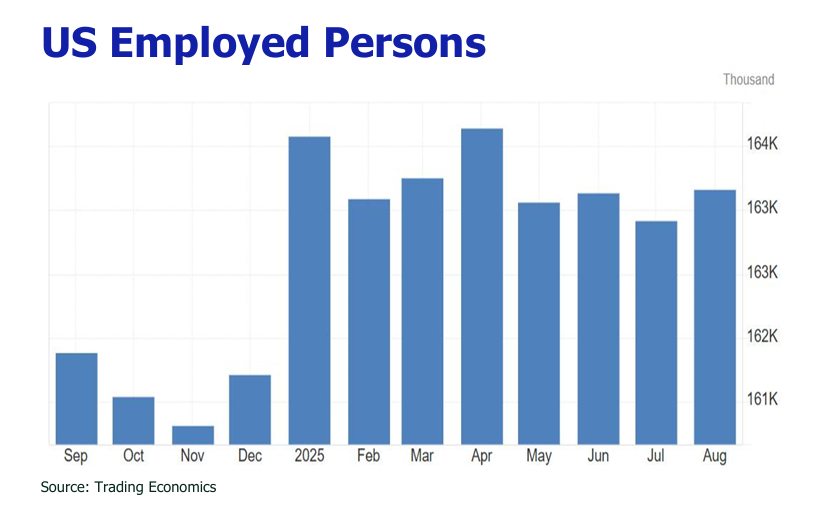

![]() The September ADP unveiled a shrinking labor market, shedding 32,000 jobs—worst since March 2023—hitting small businesses hard in services and hospitality.

The September ADP unveiled a shrinking labor market, shedding 32,000 jobs—worst since March 2023—hitting small businesses hard in services and hospitality.

![]() The CNBC/NRF Retail Monitor revealed a chic 0.66% dip in September 2025 sales (ex-autos/gas), yet a nice 5.42% yearly surge, outshining August, buoyed by wealth-fueled households.

The CNBC/NRF Retail Monitor revealed a chic 0.66% dip in September 2025 sales (ex-autos/gas), yet a nice 5.42% yearly surge, outshining August, buoyed by wealth-fueled households.

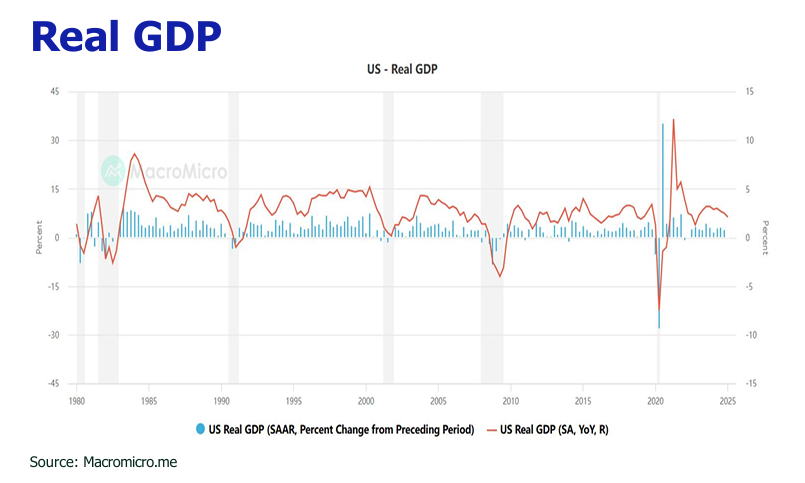

![]() October ignited a fiery US-China trade clash: China’s rare earth grip sparked Trump’s stratospheric 155% tariff threat, risking US tech shortages and GDP dips.

October ignited a fiery US-China trade clash: China’s rare earth grip sparked Trump’s stratospheric 155% tariff threat, risking US tech shortages and GDP dips.

![]() Tariff escalations of wood, steel, aluminum, kitchen cabinets, bathroom vanities, and medium and heavy-duty trucks exert new inflation pressure.

Tariff escalations of wood, steel, aluminum, kitchen cabinets, bathroom vanities, and medium and heavy-duty trucks exert new inflation pressure.

![]() A Supreme Court ruling against Trump’s tariffs could trigger massive refunds, triggering 232/301 fallback amid delays.

A Supreme Court ruling against Trump’s tariffs could trigger massive refunds, triggering 232/301 fallback amid delays.

![]() APEC summit hints at rolling back 100% China tariffs and extending tariff truce on China, spurred by China rare earth dominance and US economic pressures.

APEC summit hints at rolling back 100% China tariffs and extending tariff truce on China, spurred by China rare earth dominance and US economic pressures.

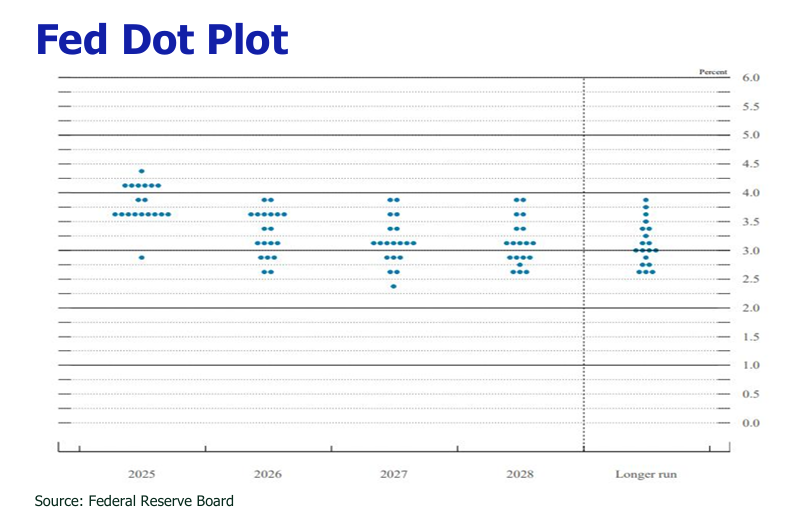

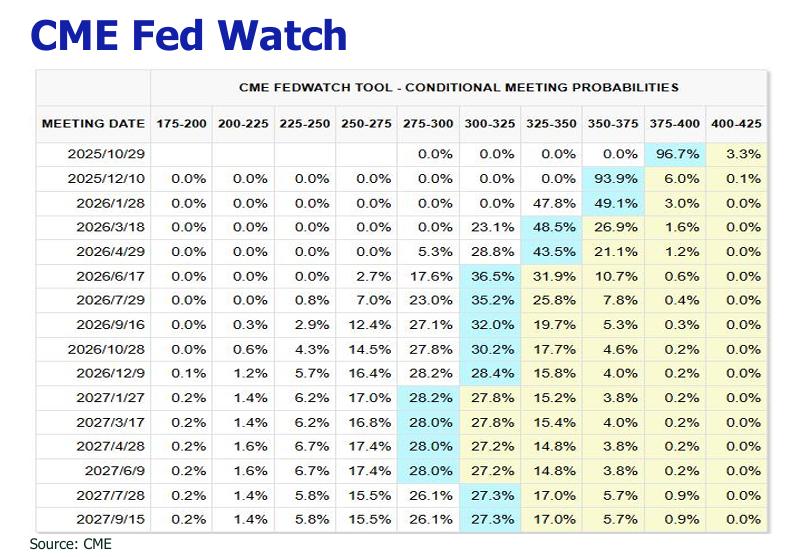

![]() Slumping jobs and tariff relief pave the way for a 97%-likely 25bp Fed rate cut on October FOMC.

Slumping jobs and tariff relief pave the way for a 97%-likely 25bp Fed rate cut on October FOMC.

![]() Golddazzles with a 40% leap past $4,000/oz in 2025, fueled by global chaos, inflation, and Fed cuts, eyeing $4,960–$6,000 by 2026.

Golddazzles with a 40% leap past $4,000/oz in 2025, fueled by global chaos, inflation, and Fed cuts, eyeing $4,960–$6,000 by 2026.

![]() October marked a turbulent descent for the HSI, plummeting over 4% month-to-date to around 26000 with shrinking daily volume to $200B-$250B in lower half month amid escalating US-China trade tensions and domestic policy uncertainties, reversing early-month gains and signaling renewed investor caution in Hong Kong’s markets.

October marked a turbulent descent for the HSI, plummeting over 4% month-to-date to around 26000 with shrinking daily volume to $200B-$250B in lower half month amid escalating US-China trade tensions and domestic policy uncertainties, reversing early-month gains and signaling renewed investor caution in Hong Kong’s markets.