Highlights

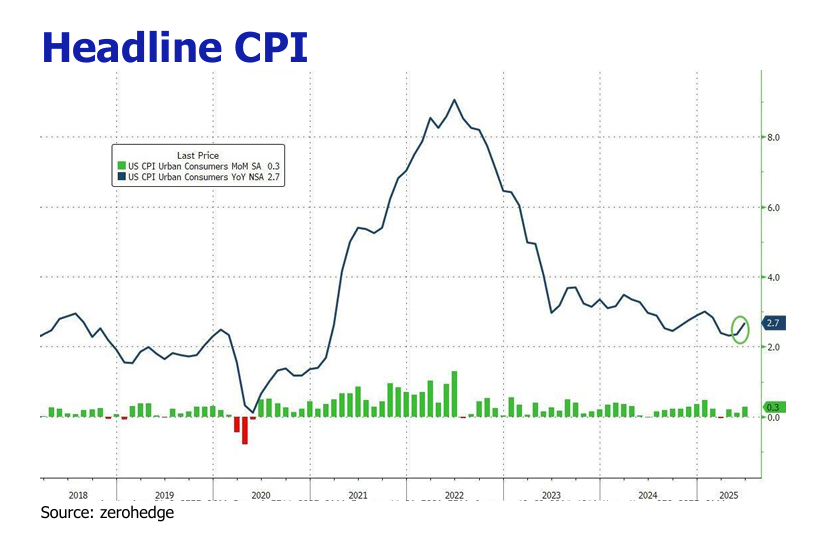

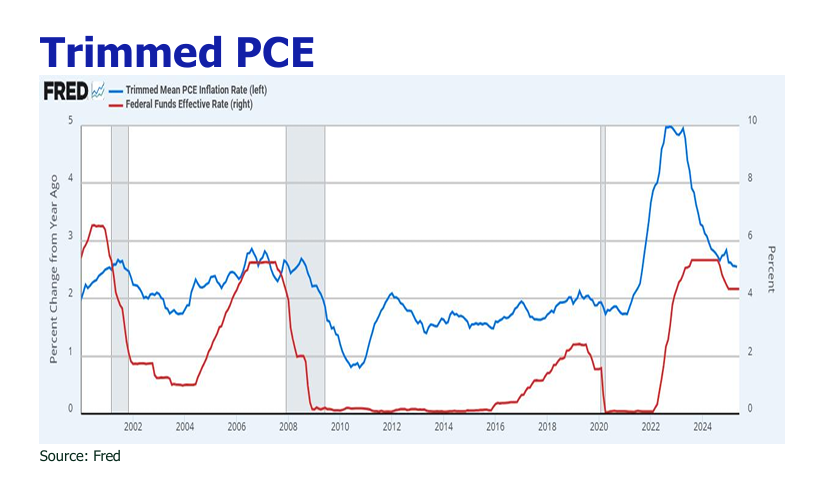

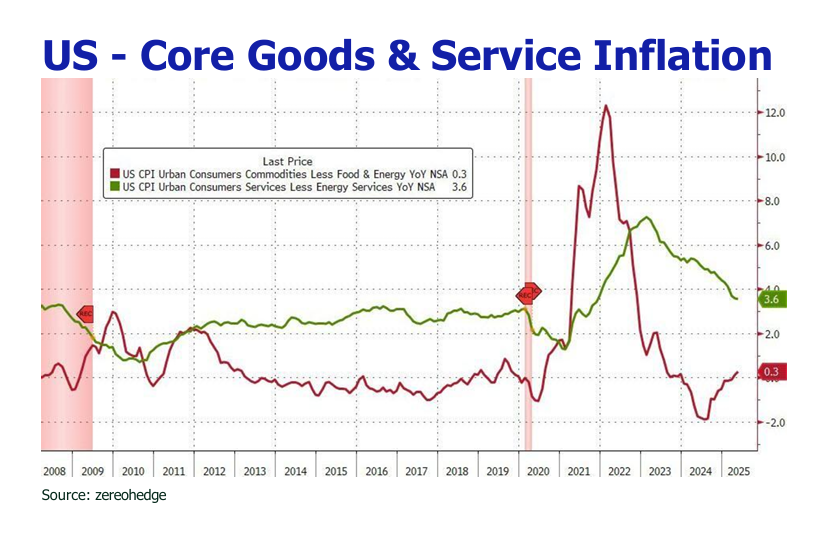

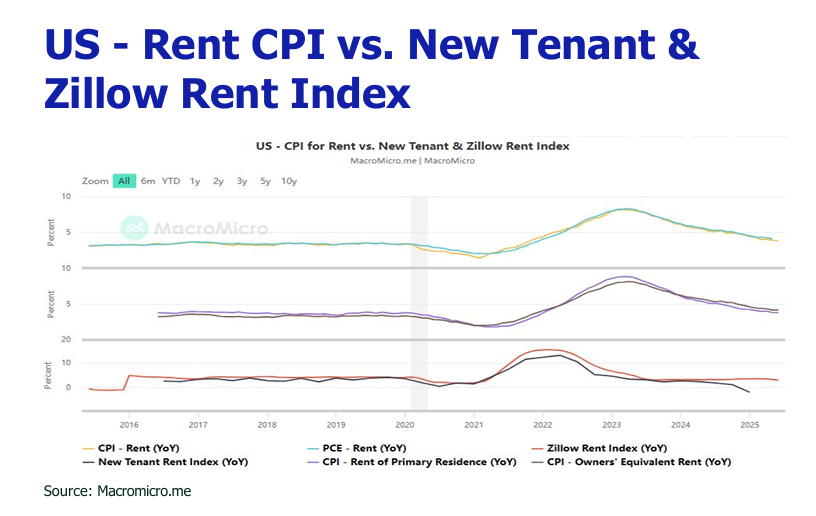

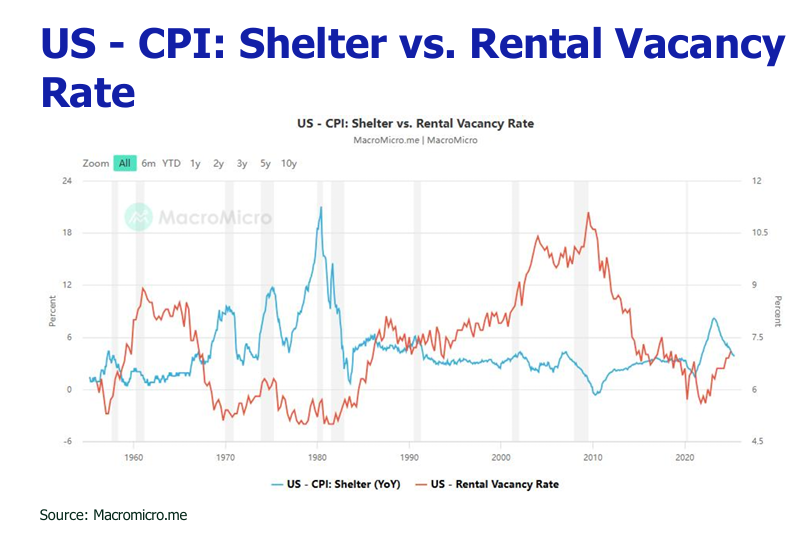

![]() June CPI rose 0.3% MoM and 2.7% YoY, with tariff-sensitive sectors driving inflation, moderated bystrategic imports from Mexico and Vietnam.

June CPI rose 0.3% MoM and 2.7% YoY, with tariff-sensitive sectors driving inflation, moderated bystrategic imports from Mexico and Vietnam.

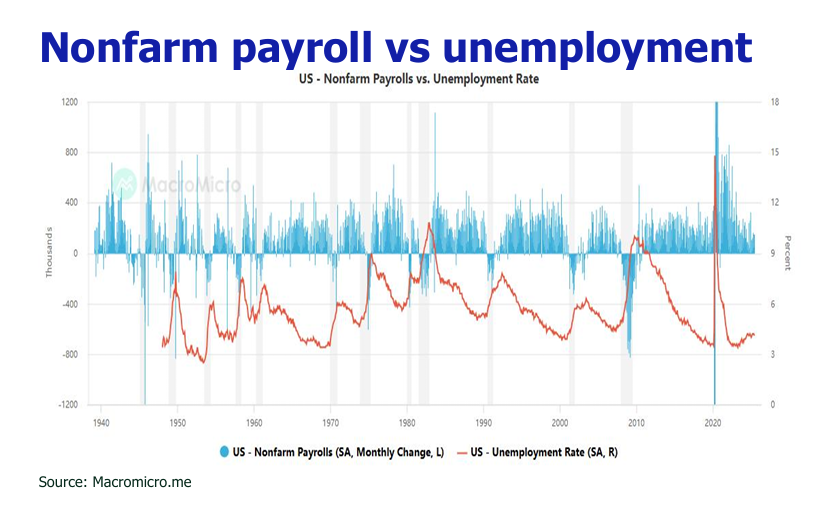

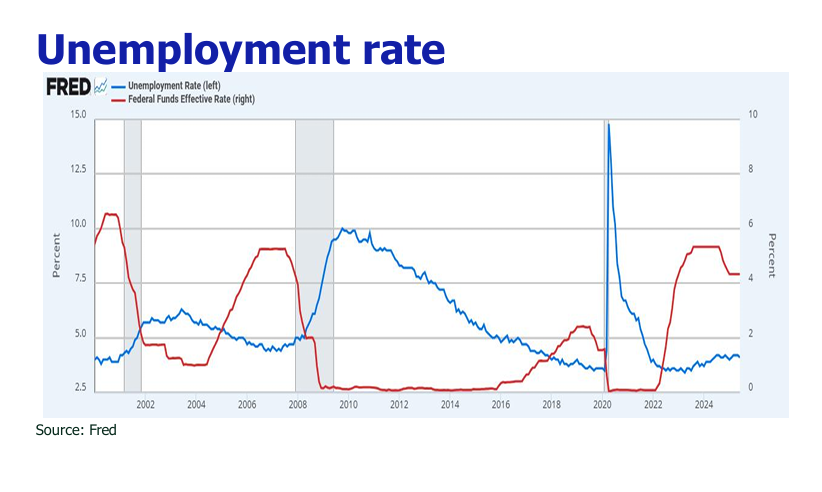

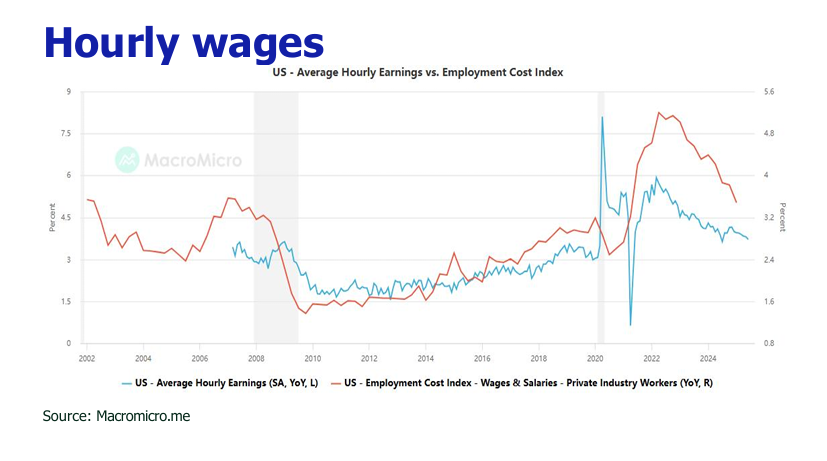

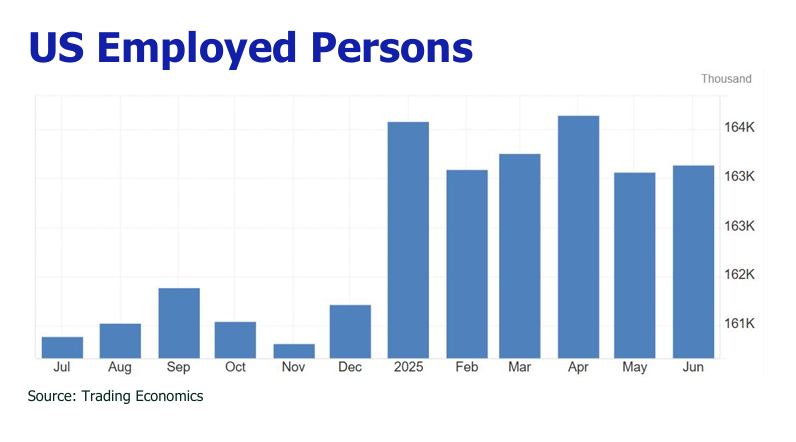

![]() June nonfarm job growth of 147,000 was led by public sector hiring, with private sector weakness and a labor force contraction masking unemployment decline to 4.1%.

June nonfarm job growth of 147,000 was led by public sector hiring, with private sector weakness and a labor force contraction masking unemployment decline to 4.1%.

![]() Retail sales grew 0.6% in June, driven by tariff-induced price increases, with real growth at 0.3% after CPI adjustment.

Retail sales grew 0.6% in June, driven by tariff-induced price increases, with real growth at 0.3% after CPI adjustment.

![]() Tariff agreements with Japan and the EU (both 15%) diminish tariff uncertainty, with exemptions and negotiations ongoing (e.g. China, India, South Korea) before August 1 deadline.

Tariff agreements with Japan and the EU (both 15%) diminish tariff uncertainty, with exemptions and negotiations ongoing (e.g. China, India, South Korea) before August 1 deadline.

![]() One Big Beautiful Bill Act (OBBBA) ’s tax cuts, increased funding for key sectors, and $5 trillion debt ceiling hike aim to boost GDP (est. 1.5–2.3% annually) and support US Treasury financing.

One Big Beautiful Bill Act (OBBBA) ’s tax cuts, increased funding for key sectors, and $5 trillion debt ceiling hike aim to boost GDP (est. 1.5–2.3% annually) and support US Treasury financing.

![]() The AI Action Plan promotes U.S. AI leadership through loosening exports, encourage infrastructure investment, tightening export controls on advanced technologies, and establishing American technology as the global benchmark.

The AI Action Plan promotes U.S. AI leadership through loosening exports, encourage infrastructure investment, tightening export controls on advanced technologies, and establishing American technology as the global benchmark.

![]() GENIUS and CLARITY Acts regulate stablecoins and digital assets, enhancing financial system integration and investor protections.

GENIUS and CLARITY Acts regulate stablecoins and digital assets, enhancing financial system integration and investor protections.

![]() Escalating tariffs and the Beautiful Act are poised to heat up inflation and strain labor market.

Escalating tariffs and the Beautiful Act are poised to heat up inflation and strain labor market.

![]() OBBBA’s $2.4–$5.0 trillion deficit increase and $554 billion Q3 Treasury issuance weaken USD amid downgrade risks.

OBBBA’s $2.4–$5.0 trillion deficit increase and $554 billion Q3 Treasury issuance weaken USD amid downgrade risks.

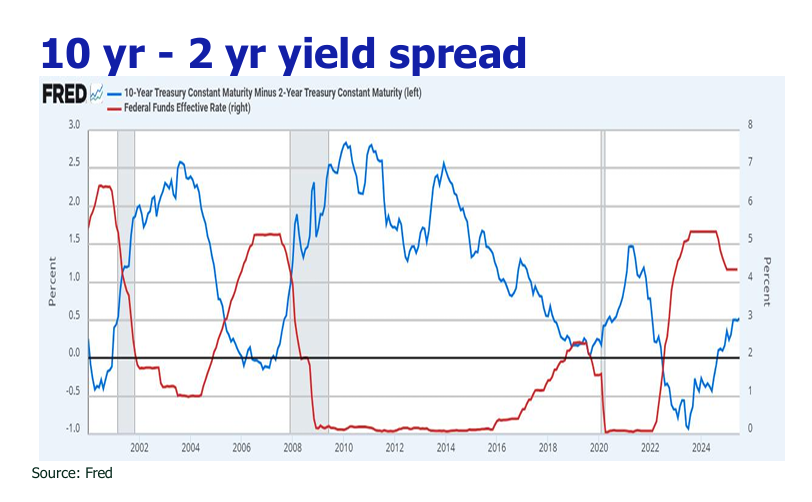

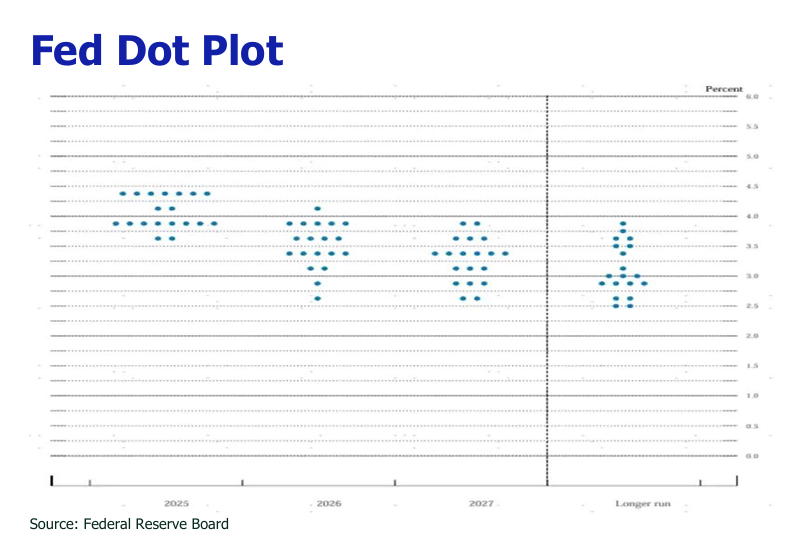

![]() Persistent inflation and labor market resilience delay rate cuts, with Powell’s tenure under scrutiny potentially altering rate cut path.

Persistent inflation and labor market resilience delay rate cuts, with Powell’s tenure under scrutiny potentially altering rate cut path.

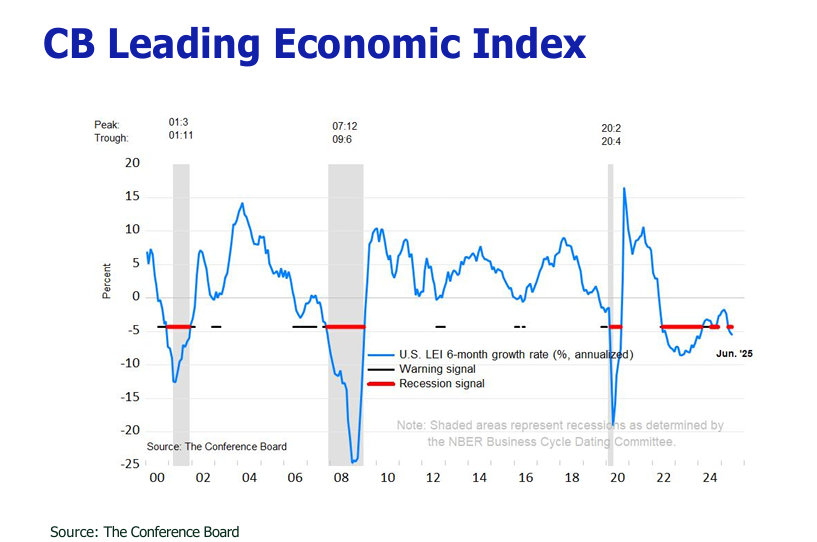

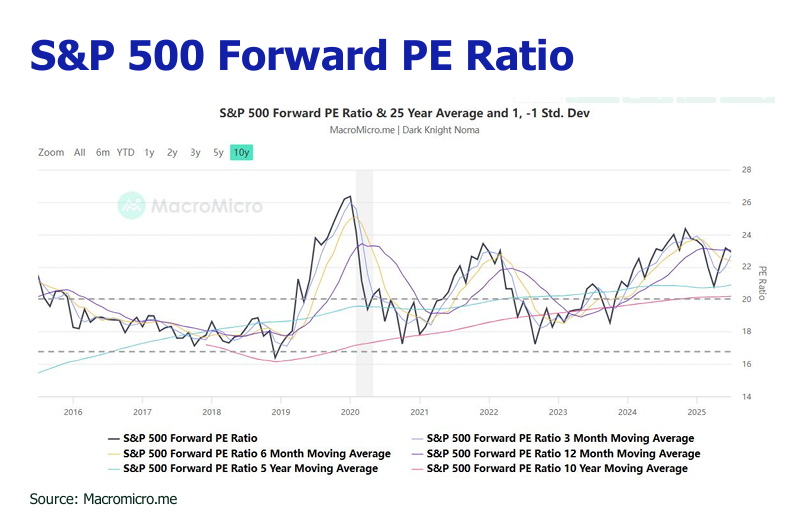

![]() OBBBA and AI Action Plan bolster tech and AI sectors, but tariffs and liquidity drain from Treasury issuance threaten Q3 market stability.

OBBBA and AI Action Plan bolster tech and AI sectors, but tariffs and liquidity drain from Treasury issuance threaten Q3 market stability.

![]() In July 2025, the HSI exhibited robust growth, reaching a 3.5-year high above 25,000 points, driven by foreign fund inflows, positive trade developments, and optimism in Tech and Healthcare sectors, with daily volume of HK$190-340B.

In July 2025, the HSI exhibited robust growth, reaching a 3.5-year high above 25,000 points, driven by foreign fund inflows, positive trade developments, and optimism in Tech and Healthcare sectors, with daily volume of HK$190-340B.