Highlights

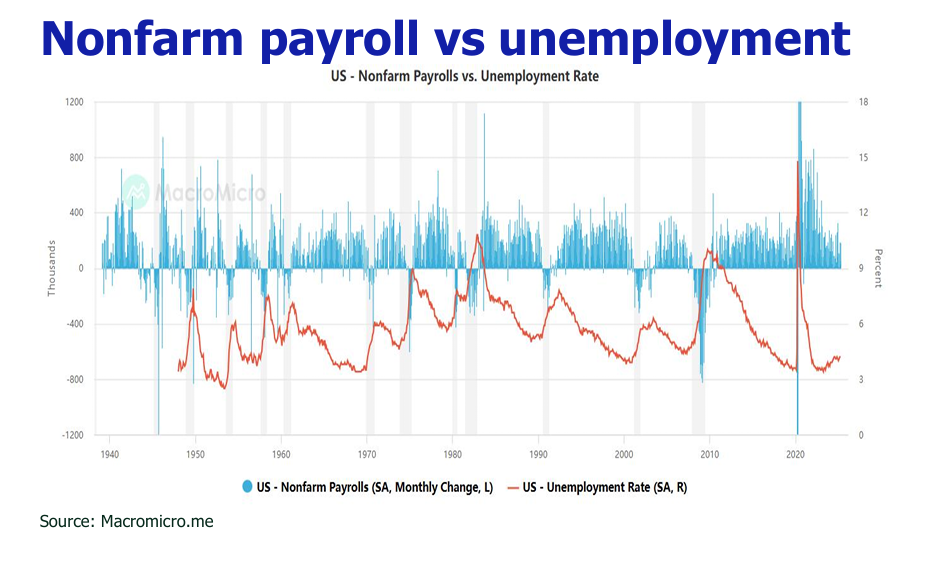

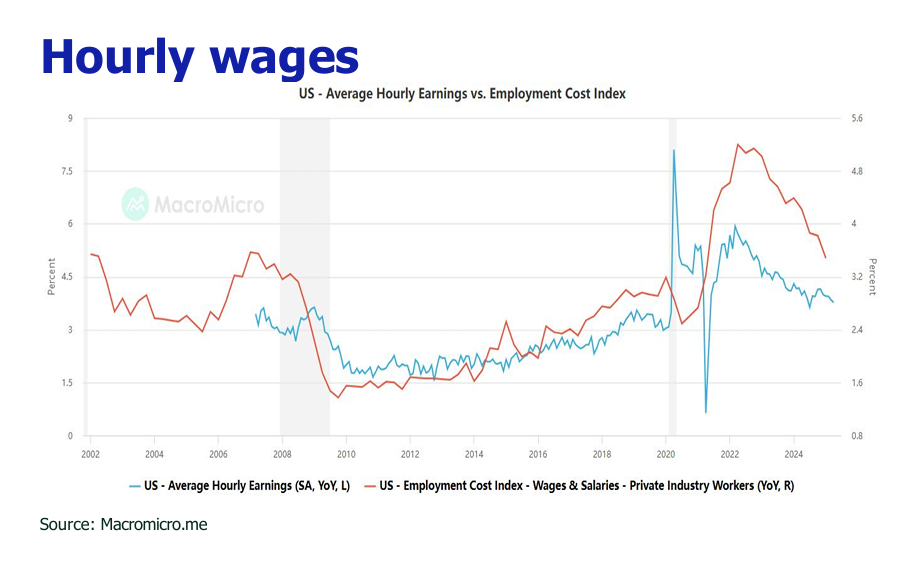

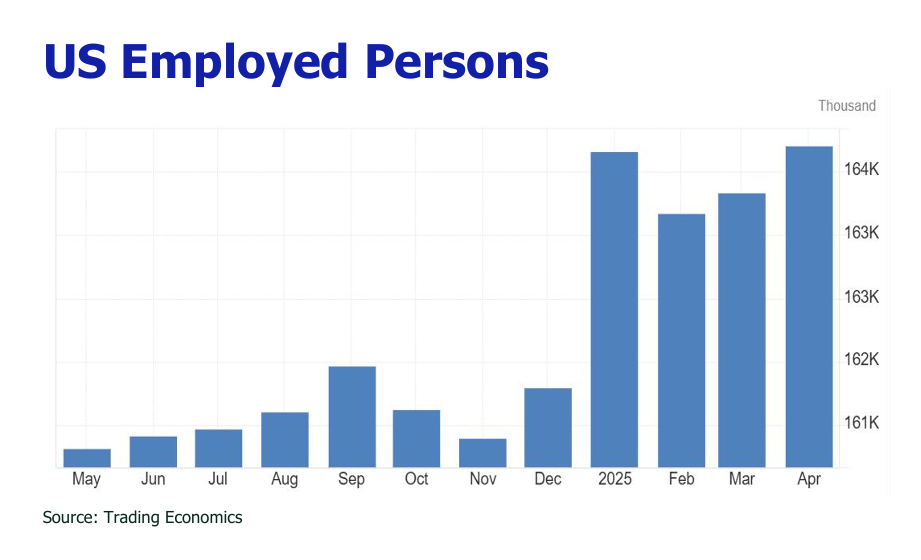

![]() April 2025 saw 177K new jobs, with steady unemployment (4.2%) albeit slowing wage growth (0.2% monthly), underscoring labor market resilience.

April 2025 saw 177K new jobs, with steady unemployment (4.2%) albeit slowing wage growth (0.2% monthly), underscoring labor market resilience.

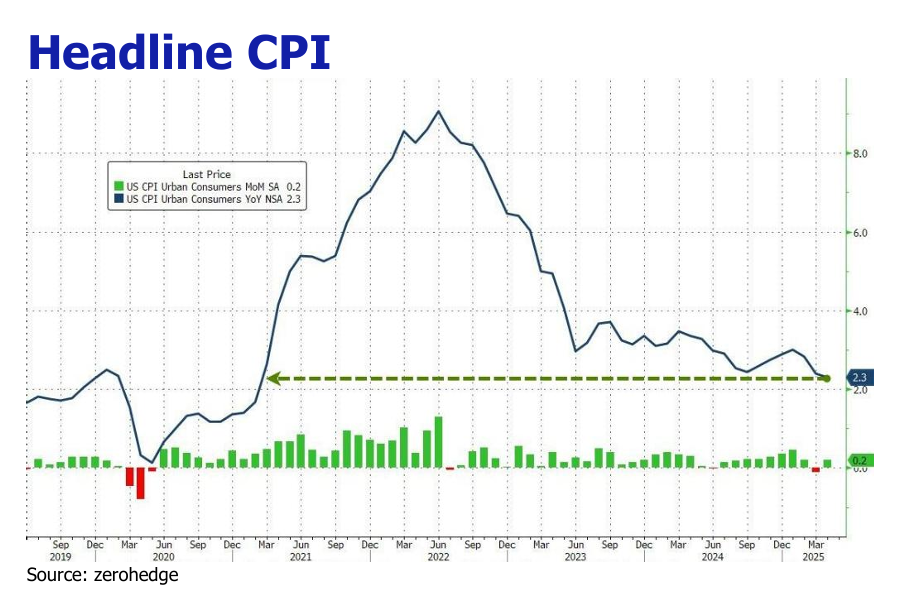

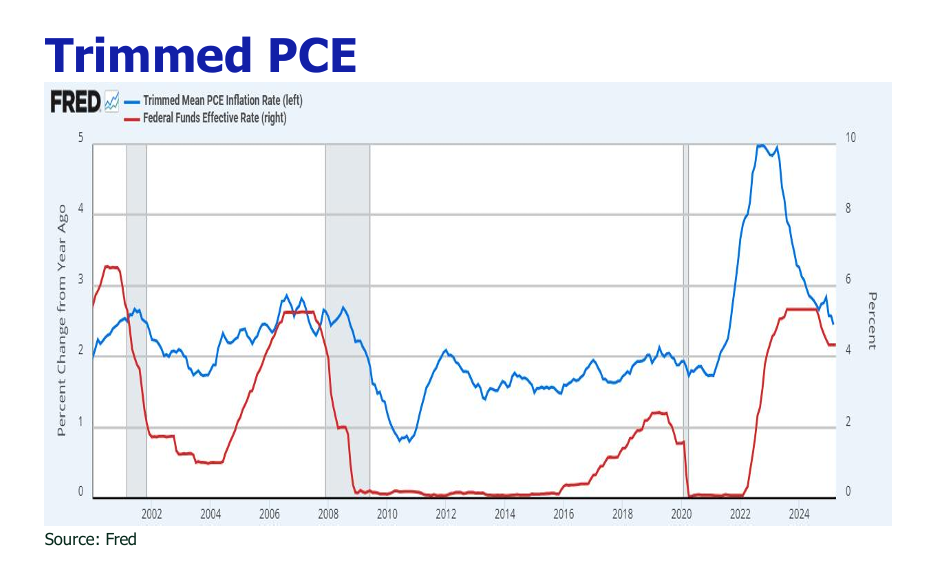

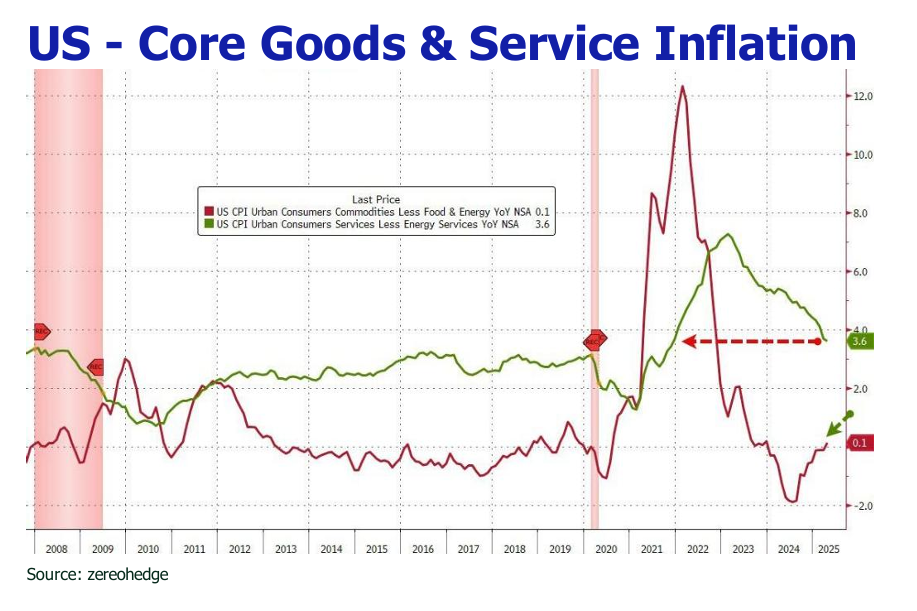

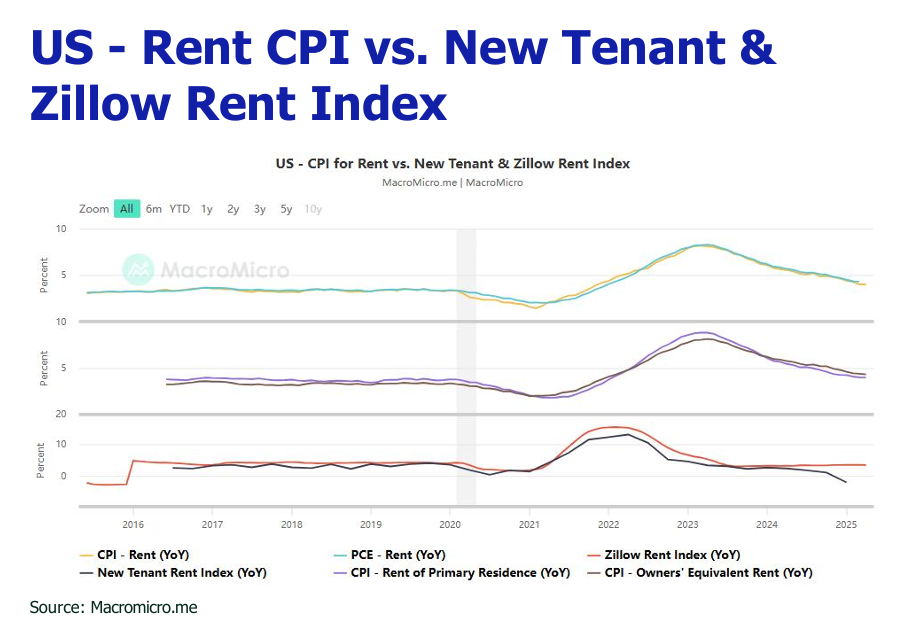

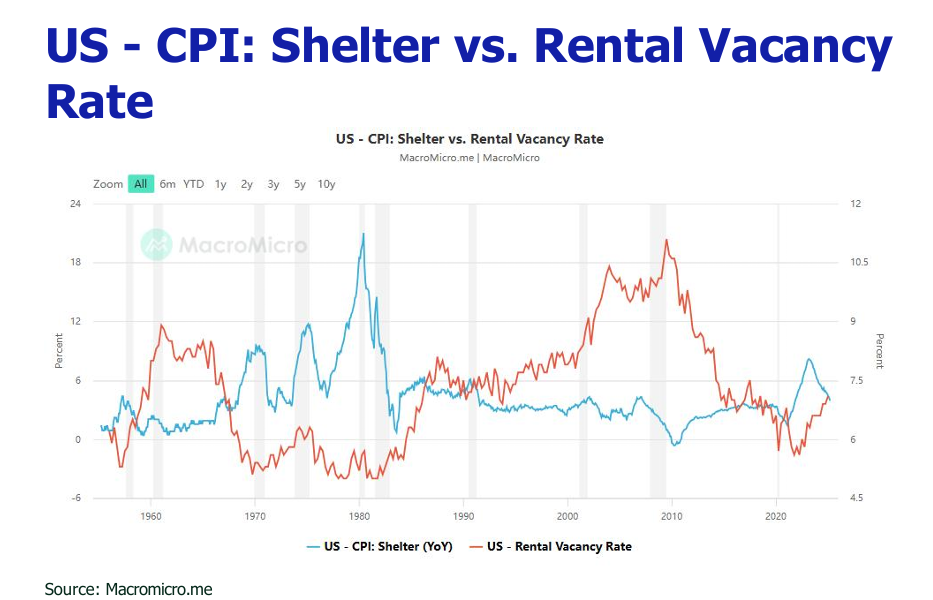

![]() Inflation eased slightly with April CPI rising 2.3% YoY (core CPI 2.8%), the lowest since 2021. Shelter costs drove increases, but “super-core” inflation (services ex-shelter) fell to 3.01%.

Inflation eased slightly with April CPI rising 2.3% YoY (core CPI 2.8%), the lowest since 2021. Shelter costs drove increases, but “super-core” inflation (services ex-shelter) fell to 3.01%.

![]() April retail sales grew just 0.1%, down from March’s 1.7%, as tariff uncertainty dampened consumer spending, especially in autos.

April retail sales grew just 0.1%, down from March’s 1.7%, as tariff uncertainty dampened consumer spending, especially in autos.

![]() U.S.-China tariffs eased (30% from 145%), but new EU (50%) and Japan (10-25%) tariffs were imposed. A court blocked broad tariffs, complicating the tariff outlook.

U.S.-China tariffs eased (30% from 145%), but new EU (50%) and Japan (10-25%) tariffs were imposed. A court blocked broad tariffs, complicating the tariff outlook.

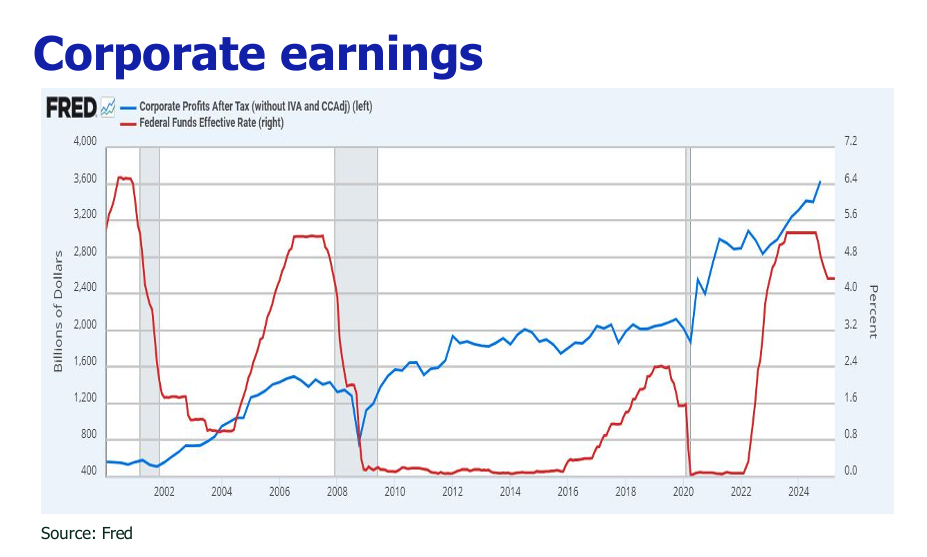

![]() The House approved a $5T tax cut, extending TCJA benefits (higher deductions, child credit, SALT cap) but worsening deficits, despite partial offset by $2.1T tariff.

The House approved a $5T tax cut, extending TCJA benefits (higher deductions, child credit, SALT cap) but worsening deficits, despite partial offset by $2.1T tariff.

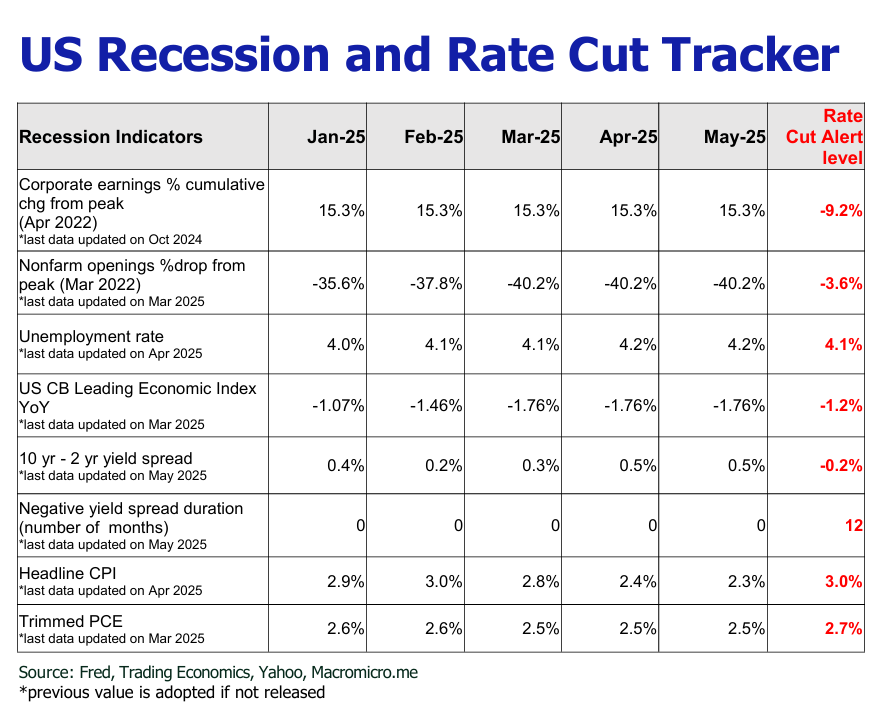

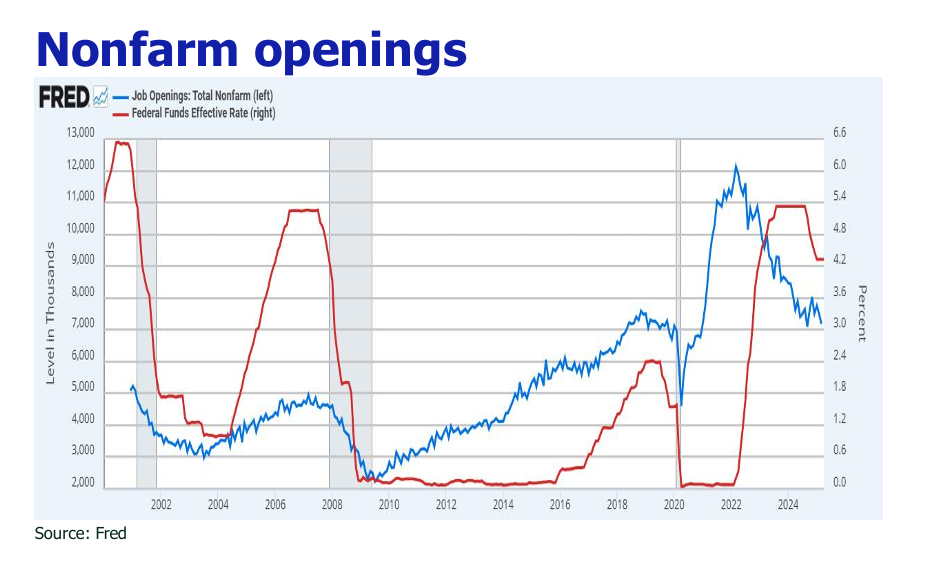

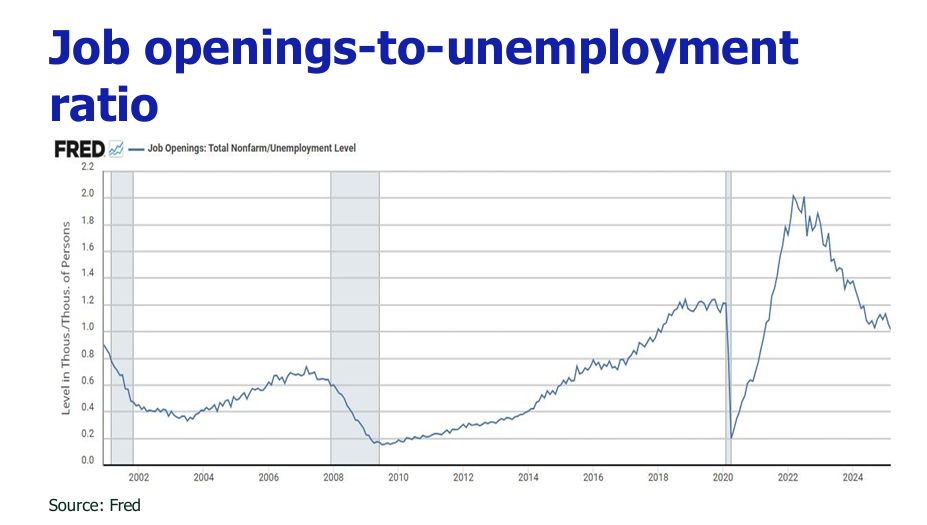

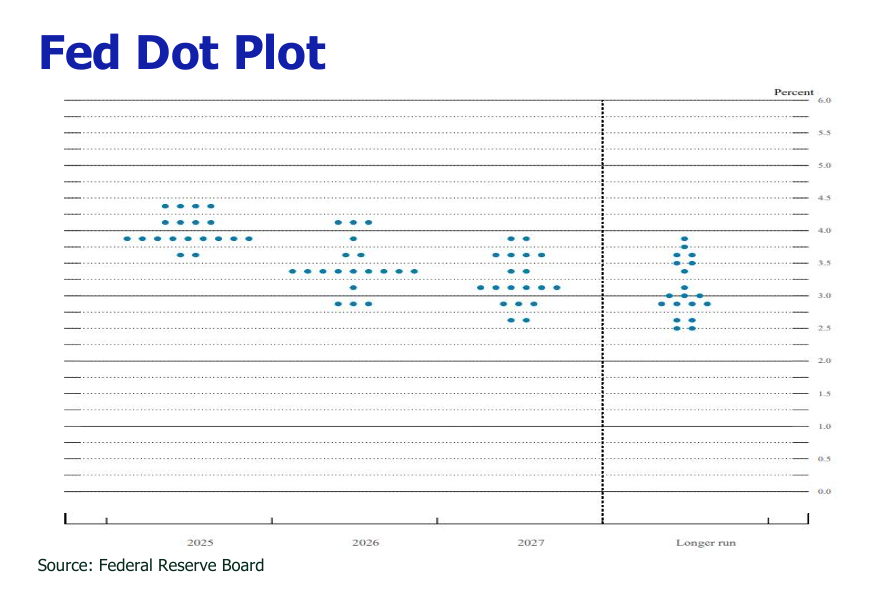

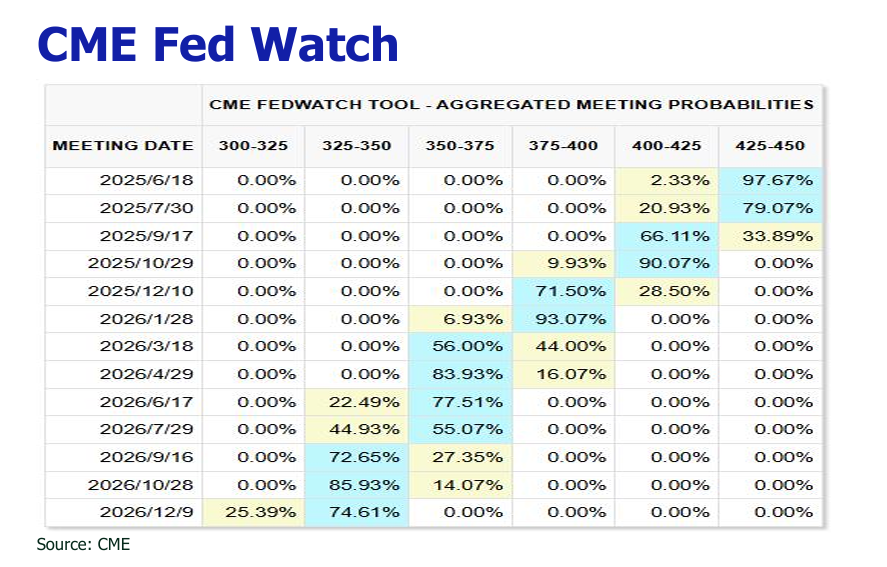

![]() Ratecuts are expected to delay against prevailing call in June as tariffs may push core PCE inflation up 0.5-1%, plus strong labor market (4.2% jobless rate) reduces recession risk.

Ratecuts are expected to delay against prevailing call in June as tariffs may push core PCE inflation up 0.5-1%, plus strong labor market (4.2% jobless rate) reduces recession risk.

![]() US dollar is circling the drain (index down 6% from year peak) sowed by tariff volatility, rising deficits, and a Moody’s downgrade, pointing to to 12-19% total drop under rate cut scenario.

US dollar is circling the drain (index down 6% from year peak) sowed by tariff volatility, rising deficits, and a Moody’s downgrade, pointing to to 12-19% total drop under rate cut scenario.

![]() The U.S. debt, standing at $36 trillion or 123% of GDP, combined with rising refinancing costs (3.75% to 5.25%) and expanding deficits due to tax cuts, continues to exert significant pressure on the U.S. Treasury.

The U.S. debt, standing at $36 trillion or 123% of GDP, combined with rising refinancing costs (3.75% to 5.25%) and expanding deficits due to tax cuts, continues to exert significant pressure on the U.S. Treasury.

![]() Following a strong rally in May, the S&P 500 is expected to enter into a volatile period due to the interplay of improved sentiment from easing tariff tensions, reinforcement of the AI narrative, weaker household consumption, higher inflation, delayed rate cuts, elevated treasury yields and latest tariff uncertainty surrounding the US court ruling to halt most of Trump’s IEEPA-based tariffs.

Following a strong rally in May, the S&P 500 is expected to enter into a volatile period due to the interplay of improved sentiment from easing tariff tensions, reinforcement of the AI narrative, weaker household consumption, higher inflation, delayed rate cuts, elevated treasury yields and latest tariff uncertainty surrounding the US court ruling to halt most of Trump’s IEEPA-based tariffs.

![]() The HangSeng Index gained 6% to around 23400 with HK$200-300B daily turnover, under the confluence of China’s Monetary Stimulus (50 bp RRR and 10 bp 7-day repo rate cuts) and abated US-China trade tensions.

The HangSeng Index gained 6% to around 23400 with HK$200-300B daily turnover, under the confluence of China’s Monetary Stimulus (50 bp RRR and 10 bp 7-day repo rate cuts) and abated US-China trade tensions.